PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027492

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027492

Molasses Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

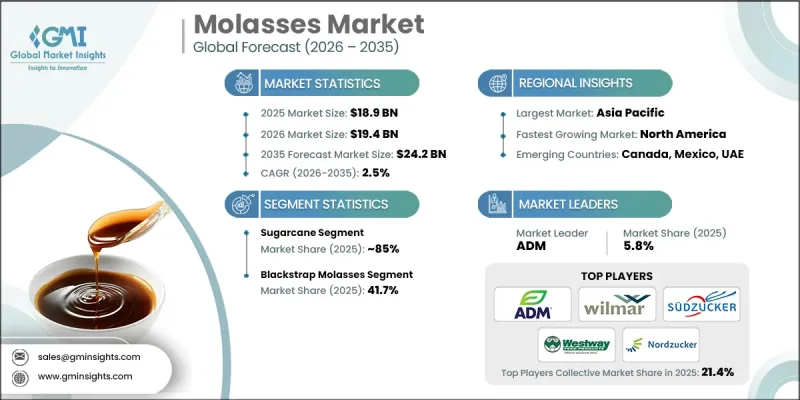

The Global Molasses Market was valued at USD 18.9 billion in 2025 and is estimated to grow at a CAGR of 2.5% to reach USD 24.2 billion by 2035.

The market is witnessing expansion owing to increasing utilization across the food and beverage, animal feed, and biofuel industries. In the food sector, molasses is widely used as a natural sweetener and flavor enhancer in baked products, confectionery items, and beverage formulations, supporting its consistent demand in processed food manufacturing. Growing consumer preference for plant-based diets is further strengthening its role as a substitute for refined sugar-based ingredients. In the animal feed industry, molasses is valued for its energy-rich composition and palatability, helping improve feed efficiency and livestock productivity. The biofuel sector also represents a key growth avenue, where molasses is used as a cost-effective raw material for ethanol production. Sustainability trends are increasingly shaping the market, with manufacturers focusing on environmentally responsible production practices. Although fluctuations in sugar prices and weather-related disruptions in sugarcane cultivation create supply-side challenges, demand remains resilient due to expanding industrial applications. Technological advancements and improved processing efficiency are further enhancing production output, reducing costs, and ensuring consistent product quality across end-use industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $18.9 Billion |

| Forecast Value | $24.2 Billion |

| CAGR | 2.5% |

The sugarcane segment accounted for 85% share in 2025 and is expected to maintain steady growth at a CAGR of 2.5% through 2035. Its dominance is primarily attributed to large-scale cultivation in tropical and subtropical regions, where favorable climatic conditions support high-yielding production. The widespread availability and cost-effectiveness of sugarcane make it the most important raw material source for molasses across global industries. Its consistent supply base ensures stable production for food, feed, and industrial applications, reinforcing its leading position in the market structure.

The blackstrap molasses segment held a 41.7% share in 2025, supported by its strong nutritional profile and deep flavor characteristics. This type of molasses is widely utilized in food processing and animal nutrition applications due to its high mineral content, including iron and calcium. Its functional and nutritional advantages also contribute to its growing acceptance among health-oriented consumers seeking more natural ingredient alternatives in daily diets.

North America Molasses Market is projected to grow at a CAGR of 2.3% from 2026 to 2035. Regional growth is driven by increasing demand for natural sweeteners and functional food ingredients across the food and beverage industry. Rising consumer awareness regarding clean-label and plant-based products is further supporting market expansion. In addition, advancements in processing technologies, including enzymatic extraction and fermentation-based methods, are enhancing product quality and improving production efficiency across manufacturing facilities in the region.

Key companies operating in the Global Molasses Market include Sudzucker, ADM, Wilmar International Limited, Nordzucker, American Crystal Sugar Company, Michigan Sugar Company, Amalgamated Sugar, Westway Feed Products, B & G Foods, Cosun Beet Company, International Molasses Corporation, and Crosby Molasses Co., Ltd. Companies in the Molasses Market are strengthening their market position by focusing on production efficiency, supply chain optimization, and diversification of application areas. Many players are investing in advanced processing technologies to improve yield quality, reduce production costs, and ensure consistent product standards. Strategic expansion of distribution networks is helping companies enhance global reach and improve accessibility across end-use industries. Firms are also emphasizing sustainable sourcing practices and environmentally friendly production methods to align with evolving regulatory expectations and consumer preferences. Partnerships with food, feed, and biofuel manufacturers are supporting long-term demand stability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Source

- 2.2.3 Type

- 2.2.4 Category

- 2.2.5 Form

- 2.2.6 Application

- 2.2.7 Packaging

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand in food and beverage industries

- 3.2.1.2 Growth in animal feed production

- 3.2.1.3 Expansion of the biofuel sector, particularly ethanol production

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fluctuating sugar prices and weather-related disruptions to production

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for natural sweeteners and health benefits

- 3.2.3.2 Expanding use in animal feed and biofuel industries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Source, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Sugarcane

- 5.3 Sugar beets

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Sugarcane

- 6.3 Sugar beets

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Category, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Organic

- 7.3 Conventional

Chapter 8 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Liquid

- 8.3 Powder

Chapter 9 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Food & beverage

- 9.2.1 Bakery & confectionery

- 9.2.2 Sauces, soups & marinades

- 9.2.3 Beverages

- 9.2.4 Dairy products

- 9.2.5 Others (breakfast cereals, porridges, ready-to-eat foods)

- 9.3 Animal feed

- 9.3.1 Livestock feed

- 9.3.2 Poultry feed

- 9.3.3 Pet food

- 9.4 Pharmaceuticals & personal care

- 9.4.1 Nutritional supplements

- 9.4.2 Medicinal products

- 9.4.3 Cosmetics & personal care

- 9.5 Industrial applications

- 9.5.1 Biofuels/ethanol production

- 9.5.2 Fermentation industry

- 9.5.3 Chemical industry

- 9.5.4 Others (ink, paint, Microbial Culture Media)

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By Packaging, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Bottles

- 10.3 Pouches

- 10.4 Bulk/industrial packaging

Chapter 11 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 ADM

- 12.2 Amalgamated Sugar

- 12.3 American Crystal Sugar Company

- 12.4 B & G Foods

- 12.5 Cosun Beet Company

- 12.6 Crosby Molasses Co., Ltd

- 12.7 International Molasses Corporation

- 12.8 Michigan Sugar Company

- 12.9 Nordzucker

- 12.10 Sudzucker

- 12.11 Westway Feed Products

- 12.12 Wilmar International Limited