PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027498

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027498

Garment Steamers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

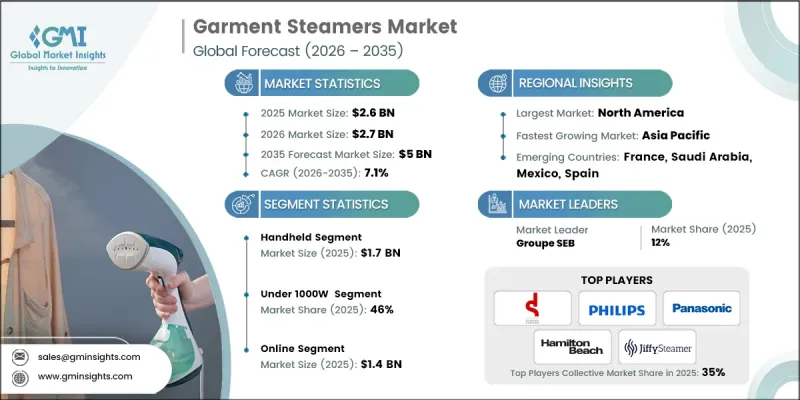

The Global Garment Steamers Market was valued at USD 2.6 billion in 2025 and is estimated to grow at a CAGR of 7.1% to reach USD 5 billion by 2035.

The market is gaining steady traction as consumers increasingly shift toward lightweight, delicate, and performance-oriented fabrics across both mass and premium apparel segments. These materials are widely preferred for their comfort, visual appeal, and adaptability to evolving fashion cycles. However, their sensitivity to heat and pressure has limited the effectiveness of conventional ironing methods, which can damage fabric texture and structure. This shift in fabric preference is directly driving demand for gentler garment care solutions. Steam-based wrinkle removal has emerged as a practical alternative, offering a non-contact, vertical approach that preserves fabric integrity while ensuring efficiency. As consumers prioritize convenience and garment longevity, steamers are becoming an essential household appliance. Additionally, the growing influence of fast-paced lifestyles and compact living spaces is further accelerating adoption, positioning garment steamers as a modern solution aligned with evolving consumer needs and fabric care requirements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.6 Billion |

| Forecast Value | $5 Billion |

| CAGR | 7.1% |

The handheld segment generated USD 1.7 billion in 2025. This category continues to dominate due to its compact design, ease of operation, and cost-effectiveness. These devices are widely adopted for quick garment touch-ups and fabric refreshing, making them highly suitable for users seeking convenience-driven solutions. Their portability and plug-and-use functionality support strong demand among consumers with limited storage space, reinforcing their widespread appeal across urban households.

The under 1000W segment accounted for 46% share in 2025. This segment supports broader market penetration by offering affordable, compact, and energy-efficient solutions that cater to first-time buyers. Its compatibility with standard electrical systems and accessibility through online retail channels contribute to increased product visibility and adoption. Although positioned at a lower price range, this segment plays a critical role in building brand familiarity and encouraging future upgrades to higher-capacity models.

U.S. Garment Steamers Market held a 64.5% share, generating USD 622.8 million in 2025. The strong market position is supported by high consumer awareness, widespread appliance usage, and a well-established retail and e-commerce ecosystem. Demand is further driven by lifestyle preferences that emphasize convenience, along with increasing adoption of delicate and casual clothing. The presence of strong distribution networks, continuous product innovation, and high replacement rates contributes to sustained market expansion in the region.

Key companies operating in the Global Garment Steamers Market include Black+Decker, Electrolux, Groupe SEB, Hamilton Beach, Jiffy Steamer, LG Electronics, Panasonic, Philips, Pure Enrichment, Reliable, SALAV, SharkNinja, Singer, Steamfast, and Sunbeam. Companies in the Global Garment Steamers Market are strengthening their market position through product innovation, strategic partnerships, and expansion of distribution channels. Manufacturers are focusing on developing compact, energy-efficient, and smart steamers with enhanced safety features and faster heat-up times to meet evolving consumer expectations. Many players are investing in digital marketing and direct-to-consumer sales platforms to improve brand visibility and customer engagement. Additionally, firms are expanding their product portfolios across different price segments to capture a wider consumer base. Emphasis on sustainable materials and energy-saving technologies is also becoming a key strategy to align with environmental trends. After-sales services, warranty extensions, and user-friendly designs further help companies build long-term customer loyalty and competitive advantage.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Power

- 2.2.4 Height

- 2.2.5 Price

- 2.2.6 End user

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth of delicate and non-iron-friendly fabrics

- 3.2.1.2 Rising awareness of hygiene and fabric sanitization

- 3.2.1.3 Growth of the fashion and apparel industry

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Performance limitations vs traditional irons

- 3.2.2.2 Water leakage and durability issues

- 3.2.3 Opportunities

- 3.2.3.1 Product innovation & differentiation

- 3.2.3.2 Premiumization and design-led offerings

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Pricing analysis

- 3.10.1 Historical price trend analysis (driven by primary research) (2022-2025)

- 3.10.2 Pricing strategy by player type (premium/value/cost-plus)

- 3.10.3 Regional price variations & purchasing power parity

- 3.10.4 Price elasticity of demand by segment

- 3.10.5 Discount & promotional pricing patterns (seasonal, e-commerce events)

- 3.11 Trade data analysis (driven by primary research)

- 3.11.1 Import/export volume & value trends (2022-2025)

- 3.11.2 Key trade corridors & tariff impact (driven by primary research)

- 3.11.3 Major exporting countries (China, Germany, South Korea)

- 3.11.4 Major importing countries (U.S., UK, Australia)

- 3.11.5 Trade flow analysis by product type (handheld vs. upright vs. steam closets)

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.2.1 Predictive maintenance & IoT sensor integration

- 3.12.2.2 Personalized fabric care recommendations (AI-powered apps)

- 3.12.2.3 Voice-activated controls & smart home ecosystems

- 3.12.2.4 Manufacturing process optimization & quality control

- 3.12.3 Risks, limitations & regulatory considerations

- 3.12.3.1 Data privacy concerns (user behavior tracking)

- 3.12.3.2 Cybersecurity vulnerabilities in connected devices

- 3.12.3.3 Consumer trust & adoption barriers

- 3.13 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.13.1 Channel coverage by region & format (modern vs. Traditional trade)

- 3.13.1.1 Online channel penetration (e-commerce platforms, D2C websites)

- 3.13.1.2 Offline channel density (hypermarkets, specialty stores, electronics retailers)

- 3.13.1.3 Emerging channels (social commerce, live shopping platforms)

- 3.13.2 Last-mile infrastructure gaps & emerging channel shifts

- 3.13.2.1 Urban vs. Rural distribution challenges

- 3.13.2.2 Same-day delivery capabilities in key markets

- 3.13.2.3 Omnichannel integration & click-and-collect model

- 3.13.1 Channel coverage by region & format (modern vs. Traditional trade)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Handheld

- 5.3 Upright

Chapter 6 Market Estimates and Forecast, By Power, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Under 1000W

- 6.3 Between 1000-1500W

- 6.4 Above 1500W

Chapter 7 Market Estimates and Forecast, By Height, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Below 20 cm

- 7.3 Between 20-24 cm

- 7.4 Above 24cm

Chapter 8 Market Estimates and Forecast, By Price, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.4 Industrial

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce

- 10.2.2 Company websites

- 10.3 Offline

- 10.3.1 Specialty stores

- 10.3.2 Hypermarkets

- 10.3.3 Electronics stores, etc.

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Black+Decker

- 12.2 Electrolux

- 12.3 Groupe SEB

- 12.4 Hamilton Beach

- 12.5 Jiffy Steamer

- 12.6 LG Electronics

- 12.7 Panasonic

- 12.8 Philips

- 12.9 Pure Enrichment

- 12.10 Reliable

- 12.11 SALAV

- 12.12 SharkNinja

- 12.13 Singer

- 12.14 Steamfast

- 12.15 Sunbeam