PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027501

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027501

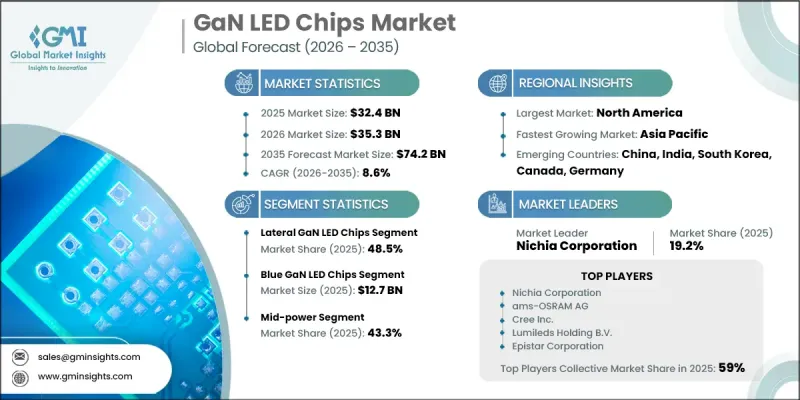

GaN LED Chips Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global GaN LED Chips Market was valued at USD 32.4 billion in 2025 and is estimated to grow at a CAGR of 8.6% to reach USD 74.2 billion by 2035.

The market is witnessing expansion driven by rapid advancements in high-performance lighting and display technologies. Increasing deployment of mini-LED backlighting in premium display systems is significantly boosting demand for GaN-based solutions. Rising integration of these chips in AR/VR devices and wearable electronics is further strengthening market growth. At the same time, growing emphasis on energy-efficient lighting solutions across commercial and industrial sectors is accelerating adoption. The development of smart LED systems for urban infrastructure and outdoor environments is also contributing to sustained demand. Continuous improvements in epitaxial growth techniques and chip architecture are enhancing brightness, efficiency, and operational lifespan. Increasing investment in advanced display manufacturing and the transition toward compact, high-density LED configurations are further supporting market expansion across consumer electronics and automotive applications, positioning GaN LED chips as a core enabling technology in next-generation electronic and lighting ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $32.4 Billion |

| Forecast Value | $74.2 Billion |

| CAGR | 8.6% |

The lateral GaN LED chips segment accounted for 48.5% share in 2025. This segment leads due to its cost-efficient manufacturing process, established production maturity, and strong suitability for low to mid-power applications. Its reliable performance and ease of integration make it widely adopted across consumer electronics, automotive displays, and general lighting systems, supporting large-scale production demand.

The blue GaN LED chips segment reached USD 12.7 billion in 2025. This segment continues to lead due to its extensive use in display backlighting, general illumination, and high-efficiency lighting systems. Its strong energy performance and compatibility with phosphor-based white light conversion make it essential across multiple end-use industries, including consumer electronics and automotive lighting.

North America GaN LED Chips Market held 38.5% share in 2025. Market growth in the region is supported by a strong regulatory focus on energy efficiency and widespread adoption of advanced lighting technologies. Increasing deployment of smart lighting infrastructure integrated with digital control systems is enhancing market penetration. Rising investments in connected lighting platforms across commercial and industrial facilities are further strengthening regional demand. Government and private sector initiatives aimed at improving energy optimization through high-efficiency lighting solutions are also accelerating adoption across multiple applications.

Key companies operating in the GaN LED Chips Market include Nichia Corporation, ams-OSRAM AG, Lumileds Holding B.V., Cree, Inc., Epistar, Infineon Technologies AG, Veeco Instruments Inc., Allegro MicroSystems, Aixtron SE, Sumitomo Electric Industries, Ltd., Fujitsu Ltd., Bridgelux, SemiLEDs Corporation, Epileds Technologies, Inc., GaNPower International Inc., Qorvo, Inc., Aledia, Efficient Power Conversion Corporation, and Navitas Semiconductor. Companies in the GaN LED Chips Market are focusing on strengthening their competitive position through continuous technological innovation and process optimization. Significant investments are being directed toward improving epitaxial growth techniques, chip efficiency, and thermal performance. Strategic partnerships with display manufacturers and lighting solution providers are helping expand application reach across multiple industries. Firms are also increasing production capacity to meet rising demand for mini-LED and smart lighting systems. Expansion into emerging markets and diversification of product portfolios are further supporting growth. Additionally, companies are integrating advanced automation and AI-driven manufacturing processes to enhance yield, reduce costs, and improve product consistency, ensuring stronger long-term market positioning.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Emission type trends

- 2.2.2 Chip architecture trends

- 2.2.3 Power class trends

- 2.2.4 Substrate type trends

- 2.2.5 Application trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising micro-LED adoption in premium displays

- 3.2.1.2 High demand from AR/VR and wearable displays

- 3.2.1.3 Increasing demand for energy-efficient lighting solutions

- 3.2.1.4 Expansion of smart city LED infrastructure projects

- 3.2.1.5 Growth in mini-LED backlighting for LCD panels

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing cost of GaN substrates

- 3.2.2.2 Thermal management complexity in high-power applications

- 3.2.3 Market opportunities

- 3.2.3.1 Integration in next-generation micro-LED televisions

- 3.2.3.2 Expansion in automotive LiDAR and sensing applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Emission Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Blue GaN LED chips

- 5.3 Green GaN LED chips

- 5.4 UV GaN LED chips

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Chip Architecture, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Lateral GaN LED chips

- 6.3 Vertical GaN LED chips

- 6.4 Thin-film GaN LED chips

Chapter 7 Market Estimates and Forecast, By Power Class, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Low power

- 7.3 Mid power

- 7.4 High power

Chapter 8 Market Estimates and Forecast, By Substrate Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Sapphire

- 8.3 Silicon carbide (SiC)

- 8.4 Silicon (Si)

- 8.5 GaN-on-GaN

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 General lighting

- 9.3 Display backlighting

- 9.4 Automotive lighting

- 9.5 Display & signage

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Aixtron SE

- 11.1.2 Infineon Technologies AG

- 11.1.3 Lumileds Holding B.V.

- 11.1.4 Cree, Inc.

- 11.1.5 ams-OSRAM AG

- 11.1.6 Nichia Corporation

- 11.1.7 Epistar

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Bridgelux

- 11.2.1.2 Qorvo, Inc.

- 11.2.1.3 Navitas Semiconductor

- 11.2.1.4 Allegro MicroSystems

- 11.2.2 Asia Pacific

- 11.2.2.1 Fujitsu Ltd.

- 11.2.2.2 Sumitomo Electric Industries, Ltd.

- 11.2.2.3 SemiLEDs Corporation

- 11.2.2.4 Epileds Technologies, Inc.

- 11.2.3 Europe

- 11.2.3.1 Aledia

- 11.2.1 North America

- 11.3 Niche Players/Disruptors

- 11.3.1 Efficient Power Conversion Corporation

- 11.3.2 GaNPower International Inc.

- 11.3.3 Veeco Instruments Inc.