PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027524

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027524

Laptop Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

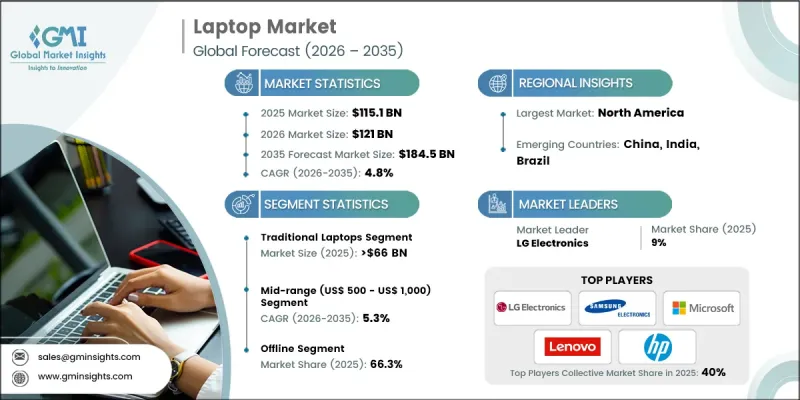

The Global Laptop Market was valued at USD 115.1 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 184.5 billion by 2035.

Market expansion is driven by the increasing adoption of remote work models, hybrid learning environments, and the growing reliance on portable computing devices with enhanced performance and connectivity. Consumers and enterprises alike are seeking advanced laptops that deliver seamless multitasking, high-speed processing, and efficient power management. The competitive landscape is evolving through strategic mergers and acquisitions among leading manufacturers, enabling them to broaden product portfolios and strengthen technological capabilities. This consolidation is accelerating innovation across multiple categories, including standard laptops, convertible devices, gaming systems, and ultraportable models. Continuous advancements in processor technologies, battery efficiency, and integrated software ecosystems are further supporting demand. As digital transformation accelerates across industries, laptops are becoming essential tools for productivity, communication, and entertainment, reinforcing their importance across diverse user groups and driving long-term market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $115.1 Billion |

| Forecast Value | $184.5 Billion |

| CAGR | 4.8% |

The shift toward intelligent and high-performance computing solutions is redefining product expectations in the market. Conventional laptops with limited capabilities are gradually being replaced by advanced systems featuring AI-enabled processors, cloud integration, and enhanced battery life. These innovations allow users to benefit from personalized computing experiences, improved connectivity across multiple devices, and optimized performance for various tasks. Increasing demand from professionals, students, and gaming enthusiasts continues to support adoption, as laptops offer portability, efficiency, and the ability to handle complex workloads with ease.

The traditional laptops segment generated USD 66 billion in 2025 and is projected to reach USD 100.3 billion by 2035. This segment remains dominant due to consistent demand from enterprise users, educational institutions, and cost-conscious consumers seeking reliable computing solutions. The familiar design, durability, and wide availability across different price points contribute to sustained growth. Traditional laptops continue to serve as a practical choice for everyday computing needs, ensuring their relevance despite the emergence of newer form factors.

The offline distribution segment accounted for 66.3% share in 2025 and is expected to grow at a CAGR of 4.5% through 2035. Physical retail outlets continue to play a crucial role in the purchasing process by offering hands-on product experiences, personalized assistance, and immediate product availability. These advantages help consumers make informed decisions, particularly when evaluating features such as build quality, keyboard comfort, and display performance. Offline channels remain especially important for enterprise buyers and first-time users, contributing to sustained foot traffic and strong sales performance.

United States Laptop Market reached USD 31.90 billion in 2025, maintaining its position as one of the most stable and high-growth markets in the region. Strong consumer spending, widespread digital adoption, and frequent technology upgrades support continued expansion. Demand for premium devices, gaming laptops, professional systems, and convertible models remains high. The presence of established retail networks and a robust e-commerce ecosystem further strengthens market growth, while increasing interest in advanced computing solutions continues to drive innovation and adoption.

Key players operating in the Global Laptop Market include Apple Inc. Dell Inc., HP Inc., Lenovo, Acer, ASUSTeK Computer Inc., Microsoft, Samsung, LG Electronics, Huawei Device Co., Ltd., Razer Inc., Micro-Star INT'L CO., LTD., Toshiba Corporation, Sony Electronics Inc., and Haier Inc. Companies in the Laptop Market are focusing on innovation, strategic partnerships, and product diversification to strengthen their competitive position. Significant investments in research and development are driving advancements in processor performance, battery efficiency, and AI-enabled features. Firms are expanding their product portfolios to cater to various consumer segments, including premium, gaming, and ultraportable categories. Strategic collaborations and mergers are helping companies enhance technological capabilities and global reach. Additionally, brands are leveraging digital marketing, e-commerce platforms, and strong retail networks to improve customer engagement and accessibility. Continuous focus on design, sustainability, and user experience further supports long-term growth and market differentiation.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Screen Size

- 2.2.4 Price Range

- 2.2.5 End User

- 2.2.6 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for remote work & hybrid learning solutions

- 3.2.1.2 Rapid technology advancements

- 3.2.1.3 Expansion of cloud computing & digital ecosystems

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High competitive pressure & price sensitivity

- 3.2.2.2 Fast product obsolescence

- 3.2.3 Opportunities

- 3.2.3.1 Rising demand for device-as-a-service

- 3.2.3.2 Shift toward AI-first and connected ecosystems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis

- 3.10.1 Import & Export Volume & Value Trends

- 3.10.2 Key Trade Corridors & Tariff Impact

- 3.10.3 Regional Trade Policy Impact (US-China Trade Dynamics)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 Predictive Analytics for Product Development

- 3.12 Infrastructure & Deployment Landscape (Driven by Primary Research)

- 3.12.1 Deployment Penetration by Region & Buyer Segment (Driven by Primary Research)

- 3.12.2 Scalability Constraints & Infrastructure Investment Trends (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Laptop Market Estimates & Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Traditional Laptops

- 5.3 2-in-1 Laptops

Chapter 6 Laptop Market Estimates & Forecast, By Screen Size, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Up to 10.9 inch

- 6.3 11 to 14.9 inch

- 6.4 15 to 16.9 inch

- 6.5 Above 17 inches

Chapter 7 Laptop Market Estimates & Forecast, By Price Range, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Economy (Up to US$ 500)

- 7.3 Mid-range (US$ 500 - US$ 1,000)

- 7.4 High (Above US$ 1,000)

Chapter 8 Laptop Market Estimates & Forecast, By End Use, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Personal

- 8.3 Commercial

- 8.3.1 Corporate

- 8.3.2 Gaming

- 8.3.3 Educational Institutes

- 8.3.4 BFSI

- 8.3.5 Others (Retail stores, creative studios, etc.)

- 8.4 Industrial

Chapter 9 Laptop Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-Commerce Sites

- 9.2.2 Company Website

- 9.3 Offline

- 9.3.1 Multi-brand Stores

- 9.3.2 Departmental Stores

- 9.3.3 Specialty Stores

- 9.3.4 Other Retail Stores

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Acer

- 11.2 Apple Inc.

- 11.3 ASUSTeK Computer Inc.

- 11.4 Dell Inc.

- 11.5 Haier Inc.

- 11.6 HP Inc.

- 11.7 Huawei Device Co., Ltd.

- 11.8 Lenovo

- 11.9 LG Electronics

- 11.10 Microsoft

- 11.11 Micro-Star INT'L CO., LTD.

- 11.12 Razer Inc.

- 11.13 SAMSUNG

- 11.14 SONY ELECTRONICS INC.

- 11.15 Toshiba Corporation