PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027541

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027541

Nano Fertilizers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

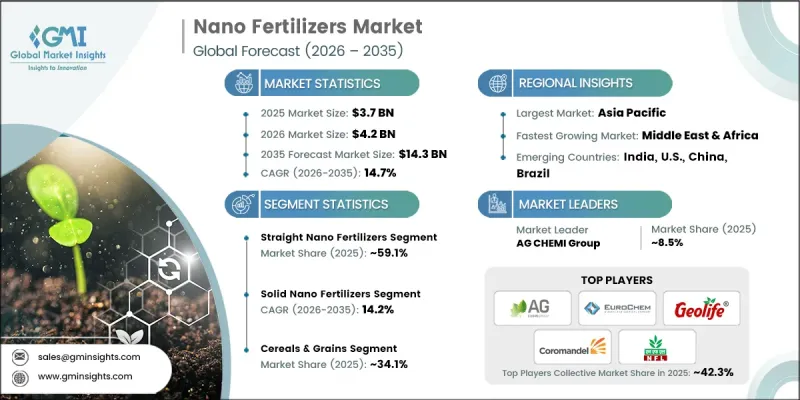

The Global Nano Fertilizers Market was valued at USD 3.7 billion in 2025 and is estimated to grow at a CAGR of 14.7% to reach USD 14.3 billion by 2035.

Nano fertilizers are cutting-edge nutrient delivery systems with particle sizes ranging from 1 to 100 nanometers, created using advanced nanotechnology techniques such as sol-gel synthesis, chemical vapor deposition, mechanical grinding, and eco-friendly green synthesis. These fertilizers are available in various formats, including single-nutrient straight nano fertilizers, multi-nutrient combinations, and specialty formulations. Their exceptionally high surface area-to-volume ratios allow superior nutrient absorption, enhancing crop yield while reducing environmental impact through up to 25% lower fertilizer use compared to conventional options. Rising adoption of precision agriculture, expanding sustainable farming mandates, and increasing global food demand are driving growth. As manufacturers invest in next-generation production facilities, controlled-release technology, and distribution expansion, demand from both commercial farms and smallholder cooperatives continues to rise across diverse crops and regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.7 Billion |

| Forecast Value | $14.3 Billion |

| CAGR | 14.7% |

The straight nano fertilizers segment held a 59.1% share and is projected to grow at a CAGR of 14.2% through 2035. Their targeted single-nutrient delivery addresses specific soil deficiencies, supports precise NPK customization, and effectively mitigates micronutrient shortages in crops. Farmers benefit from tailored nutrient applications, aligning with crop growth stages and minimizing environmental losses while meeting precision agriculture recommendations.

The solid nano fertilizers segment accounted for 54.1% share in 2025 and is expected to grow at a CAGR of 14.2% through 2035. Their storage stability, long shelf life, and compatibility with conventional distribution channels make them highly adoptable. Solid formulations release nutrients gradually, maintain integrity in transport, and reduce packaging and logistics costs. Granular and powder variants integrate easily with mechanical spreaders and fertigation systems, securing dominance in bulk commodity crop applications and government distribution programs.

U.S. Nano Fertilizers Market generated USD 748.3 million in 2025. Growth is fueled by precision agriculture adoption, sustainable farming initiatives, government-backed field trials, and advanced agricultural research validating nano fertilizer performance. Regional environmental regulations and high-value specialty crop production further strengthen market demand and adoption rates.

Key players operating in the Nano Fertilizers Industry include Coromandel International Limited, Paradeep Phosphates Limited (PPL), Indian Farmers Fertiliser Cooperative (IFFCO), National Fertilizers Limited (NFL), Hindustan Urvarak & Rasayan Limited (HURL), AG CHEMI Group, GeoLife Agritech India, JU Agri Sciences, Lazuriton Nano Biotechnology, Ray Nano Science & Research Centre, Indogulf BioAg, Tropical Agrosystem India, Prathista Industries Limited, and Nano Solutions. Companies in the Nano Fertilizers Market are adopting strategies to strengthen their global presence and market position by focusing on research and development to enhance nutrient efficiency, controlled-release technologies, and environmentally friendly formulations. Firms are expanding production facilities to meet rising demand and forming partnerships with distributors and agricultural cooperatives to widen market reach. Strategic investments in precision agriculture solutions, farmer education programs, and government collaborations improve adoption rates. Diversifying product portfolios to include both solid and liquid formulations, single and multi-nutrient options, enables companies to target various crop types and geographies while building brand credibility and competitive advantage.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Form

- 2.2.3 Packaging

- 2.2.4 Application

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Straight

- 5.3 Mixed

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solid

- 6.3 Liquid

Chapter 7 Market Estimates and Forecast, By Packaging, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Plastic bottles

- 7.3 Bags

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Cereals & Grains

- 8.3 Fruits, Nuts & Vegetables

- 8.4 Oilseeds & Pulses

- 8.5 Turf & Ornamentals

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Indian Farmers Fertiliser Cooperative (IFFCO)

- 10.2 Coromandel International Limited

- 10.3 AG CHEMI Group • EuroChem

- 10.4 Geolife Agritech India

- 10.5 Paradeep Phosphates Limited (PPL)

- 10.6 Tropical Agrosystem India

- 10.7 National Fertilizers Limited (NFL)

- 10.8 Hindustan Urvarak & Rasayan Limited (HURL)

- 10.9 JU Agri Sciences

- 10.10 Lazuriton Nano Biotechnology

- 10.11 Nano Solutions

- 10.12 Ray Nano Science & Research Centre

- 10.13 Indogulf BioAg

- 10.14 Prathista Industries Limited