PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027556

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027556

Celtic Salt Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

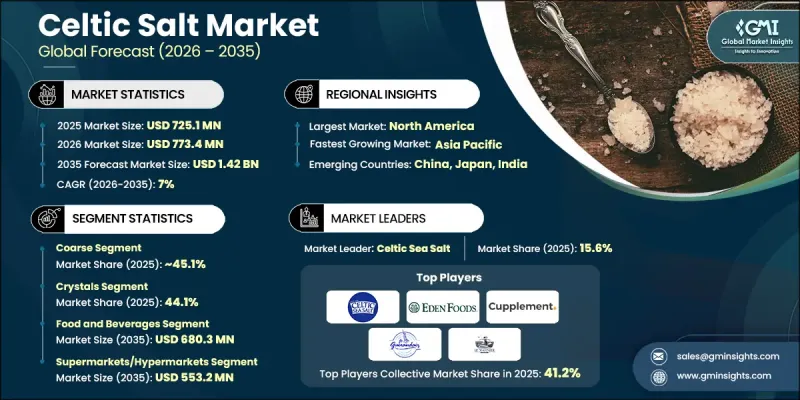

The Global Celtic salt market was valued at USD 725.1 million in 2025 and is estimated to grow at a CAGR of 7% to reach USD 1.42 billion by 2035.

The market expansion is driven by increasing consumer preference for natural and minimally processed ingredients over refined alternatives. Celtic sea salt is favored for its rich mineral content, including calcium, magnesium, and potassium, which appeals to health-conscious buyers seeking products with clean labels. The rising interest in organic and whole-food diets has further propelled the adoption of Celtic salt. Beyond culinary use, mineral-rich salts are also in demand in the beauty and personal care sectors, where consumers increasingly incorporate natural ingredients into home spa treatments, skincare routines, and holistic wellness practices. This growing focus on health, wellness, and natural ingredients is creating continuous opportunities for market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $725.1 Million |

| Forecast Value | $1.42 Billion |

| CAGR | 7% |

The coarse Celtic salt accounted for 45.1% share in 2025 and is expected to grow at a CAGR of 5.2% through 2035. Its traditional harvesting process and widespread use in cooking make it the preferred form for many households. Coarse grains retain natural moisture and minerals, enhancing both flavor and texture during food preparation.

The dietary supplement segment is projected to grow at a CAGR of 7.3% over the forecast period. Ancient Celtic salts are marketed as natural mineral supplements to support electrolyte balance, hydration, and overall cellular health, further increasing their relevance in wellness-oriented applications.

North American Celtic Salt Market is anticipated to grow at a CAGR of 6.4% during 2026 to 2035. Increasing awareness of natural, mineral-rich food ingredients has made North America a key market for Celtic salt. Health-conscious consumers in the US and Canada are increasingly substituting traditional table salt with unrefined, mineral-rich alternatives. Growth is supported by the rising popularity of organic and clean-label products, as well as a surge in gourmet cooking. In addition, the expansion of the wellness and natural cosmetics sectors is contributing to demand, as Celtic salts are increasingly included in therapeutic bath products, scrubs, and other self-care formulations.

Prominent players in the Global Celtic Salt Market include Eden Foods, Celtic Sea Salt, Le Guerandais, Le Marinier, 82 Minerals, VIVA LA GAIA, Celt Salt, Cupplement B.V., Elite Brand Supply, Dr. Celtic, and Celtic Salt. Companies in the Celtic salt market are leveraging strategies such as expanding production capacities to meet growing consumer demand and investing in sustainable harvesting practices to appeal to eco-conscious buyers. Strategic partnerships and distribution agreements enable firms to increase market reach and penetrate emerging regions. Innovation in packaging and product formats, such as ready-to-use culinary blends and wellness-focused formulations, strengthens brand differentiation. Companies also focus on marketing campaigns highlighting natural purity, mineral content, and clean-label benefits to educate consumers. Additionally, investments in research and development allow for quality enhancement, certification, and premium positioning, helping firms secure a competitive foothold in the global Celtic salt market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Form

- 2.2.4 Application

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer preference for natural and mineral-rich salts

- 3.2.1.2 Growth of health-conscious and clean-label food trends

- 3.2.1.3 Expanding applications in cosmetics and personal care products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production and harvesting costs compared to conventional salt

- 3.2.2.2 Limited consumer awareness in emerging markets

- 3.2.2.3 Competition from Himalayan pink salt and other specialty salts

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of online retail and specialty gourmet food platforms

- 3.2.3.2 Increasing demand for natural dietary supplements

- 3.2.3.3 Rising demand for premium and artisanal food ingredients

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Coarse/Grey (Sel Gris)

- 5.2.1 Traditional Unwashed

- 5.2.2 Dried Coarse

- 5.3 Fine/Ground

- 5.4 Flavored/Infused

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Crystals

- 6.3 Powder

- 6.4 Flakes

- 6.5 Liquid/Brine

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food and Beverages

- 7.2.1 Culinary/Home Cooking

- 7.2.2 Food Service/Professional

- 7.2.3 Food Manufacturing

- 7.3 Cosmetics and Personal Care

- 7.4 Dietary Supplements

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Supermarkets/Hypermarkets

- 8.3 Online Retail

- 8.4 Specialty Stores

- 8.5 Direct Sales

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Eden Foods

- 10.2 Cupplement B.V.

- 10.3 82 Minerals

- 10.4 Le Marinier

- 10.5 Le Guerandais

- 10.6 Celtic Sea Salt

- 10.7 Elite Brand Supply

- 10.8 Celt Salt

- 10.9 Celtic Salt

- 10.10 VIVA LA GAIA

- 10.11 Dr. Celtic