PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027578

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027578

Electronically Scanned Arrays Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

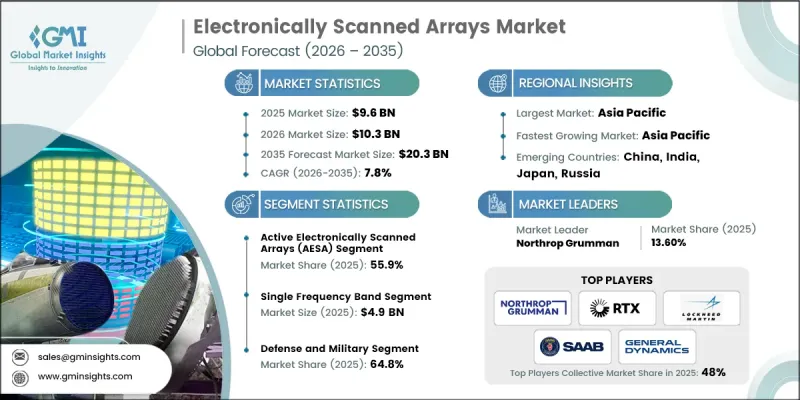

The Global Electronically Scanned Arrays Market was valued at USD 9.6 billion in 2025 and is estimated to grow at a CAGR of 7.8% to reach USD 20.3 billion by 2035.

Expansion is fueled by rising demand for precision detection and multi-target tracking across military, aerospace, and commercial applications. Governments worldwide are prioritizing advanced airborne ISR systems to improve situational awareness and threat monitoring, which is driving adoption in fighter jets, unmanned aerial vehicles, maritime patrol aircraft, and AEW&C platforms. The market is further bolstered by integration with AI-enabled sensing systems, network-centric defense technologies, and space-based applications, while commercial air traffic management and space exploration also present emerging opportunities. Increasing investments in radar modernization and the need for reliable, high-performance sensing systems continue to propel the electronically scanned arrays industry forward.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.6 Billion |

| Forecast Value | $20.3 Billion |

| CAGR | 7.8% |

The active electronically scanned arrays (AESA) segment held a 55.9% share in 2025, primarily due to its high-speed beam steering, multi-target tracking capabilities, and strong resistance to electronic countermeasures. These arrays are highly reliable, require minimal maintenance, and deliver superior performance, making them the preferred choice for modern defense systems, aerospace applications, and surveillance networks. Their extensive use across fighter aircraft, naval defense systems, and air defense applications ensures that AESA maintains market dominance.

The single frequency band segment reached USD 4.9 billion in 2025, owing to its dependable high-power performance and ease of integration. It is widely utilized in established radar systems, naval operations, and early warning networks. Its robust architecture and proven reliability reinforce its continued adoption in ground-based and naval radar deployments.

North America Electronically Scanned Arrays Market accounted for 38.2% share in 2025. The region's growth is driven by substantial defense modernization efforts and advanced aerospace technologies. High demand for military aviation systems, missile defense networks, and naval platforms is encouraging the deployment of AESA and PESA technologies. Additionally, the ongoing upgrade of legacy radar systems, adoption in commercial aviation and space-based platforms, and strong R&D infrastructure supported by leading defense contractors are boosting regional market expansion.

Key players in the Global Electronically Scanned Arrays Market include BAE Systems, Aselsan A.S., Bharat Electronics Limited, Elbit Systems Ltd., General Dynamics Corporation, Hanwha Systems Co., Ltd., Hensoldt AG, Indra Sistemas S.A., Israel Aerospace Industries Ltd., L3Harris Technologies, Inc., Leonardo S.P.A., Lig Nex1 Co., Ltd., Lockheed Martin Corporation, Mitsubishi Electric Corporation, Northrop Grumman, RTX Corporation, Saab AB, Teledyne Technologies Incorporated, Thales Group, and Viasat, Inc. Companies in the Global Electronically Scanned Arrays Market are adopting strategic initiatives to enhance their market presence and maintain competitive advantage. These strategies include continuous investment in R&D to improve beamforming, signal processing, and array density capabilities, while enhancing reliability and efficiency. Firms are forming partnerships and alliances to expand regional and global distribution networks and gain access to new defense and aerospace contracts. Technology integration with AI, network-centric warfare systems, and next-generation sensors helps differentiate products and meet evolving customer requirements. Companies are also focusing on upgrading legacy systems and offering retrofit solutions for existing defense platforms. Strong participation in government programs, export initiatives, and strategic collaborations enables companies to secure long-term contracts and strengthen their foothold in both military and commercial markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Arrays Geometry trends

- 2.2.3 Frequency Band trends

- 2.2.4 Range trends

- 2.2.5 Platform trends

- 2.2.6 Application trends

- 2.2.7 End Use trends

- 2.2.8 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased global defence and homeland security spending

- 3.2.1.2 Rising adoption in space, satellite, and emerging applications

- 3.2.1.3 Advancements in radar and antenna technologies

- 3.2.1.4 Growing demand for airborne intelligence, surveillance, and reconnaissance (ISR)

- 3.2.1.5 Expansion of commercial aviation and advanced air traffic management

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development costs and complex system integration requirements

- 3.2.2.2 Stringent regulatory, export-control, and certification requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of space-based communications and satellite constellation deployments

- 3.2.3.2 Rising adoption of next-generation autonomous and unmanned systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035

- 5.1 Key trends

- 5.2 Active Electronically Scanned Arrays (AESA)

- 5.3 Passive Electronically Scanned Arrays (PESA)

Chapter 6 Market Estimates and Forecast, By Arrays Geometry, 2022 - 2035

- 6.1 Key trends

- 6.2 Planar Arrays

- 6.3 Linear Arrays

- 6.4 Frequency Scanning Arrays

Chapter 7 Market Estimates and Forecast, By Frequency Band, 2022 - 2035

- 7.1 Key trends

- 7.2 Single Frequency

- 7.2.1 X-Band

- 7.2.2 S-Band

- 7.2.3 L-Band

- 7.2.4 C-Band

- 7.2.5 Others

- 7.3 Multifrequency

Chapter 8 Market Estimates and Forecast, By Range, 2022 - 2035

- 8.1 Key trends

- 8.2 Short Range (<50 km)

- 8.3 Medium Range (50-300 km)

- 8.4 Long Range (>300 km)

Chapter 9 Market Estimates and Forecast, By Platform, 2022 - 2035

- 9.1 Key trends

- 9.2 Air

- 9.3 Naval

- 9.4 Ground

- 9.5 Space

Chapter 10 Market Estimates and Forecast, By Application, 2022 - 2035

- 10.1 Key trends

- 10.2 Radar

- 10.3 Communication

- 10.4 Navigation

- 10.5 Electronic Warfare (EW)

- 10.6 Others

Chapter 11 Market Estimates and Forecast, By End-Use, 2022 - 2035

- 11.1 Key trends

- 11.2 Defense & Military

- 11.2.1 Air Surveillance & Early Warning

- 11.2.2 Fire Control & Missile Guidance Systems

- 11.2.3 Electronic Warfare (EW) & Jamming Systems

- 11.2.4 Naval Radar & Maritime Surveillance

- 11.2.5 Ground-Based Air Defense Systems

- 11.2.6 Others

- 11.3 Civilian & Commercial

- 11.3.1 Air Traffic Control & Management

- 11.3.2 Weather Monitoring & Forecasting

- 11.3.3 Satellite Communications

- 11.3.4 Navigation

- 11.3.5 Others

Chapter 12 Market Estimates and Forecast, By Region, 2022 - 2035

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Spain

- 12.3.5 Italy

- 12.3.6 Russia

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 Middle East and Africa

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global Key Players

- 13.1.1 Northrop Grumman

- 13.1.2 RTX Corporation

- 13.1.3 Lockheed Martin Corporation

- 13.1.4 Saab AB

- 13.1.5 General Dynamics Corporation

- 13.2 Regional key players

- 13.2.1 North America

- 13.2.1.1 BAE Systems

- 13.2.1.2 General Dynamics Corporation

- 13.2.1.3 L3Harris Technologies, Inc.

- 13.2.1.4 Lockheed Martin Corporation

- 13.2.1.5 Northrop Grumman

- 13.2.1.6 RTX Corporation

- 13.2.1.7 Teledyne Technologies Incorporated

- 13.2.1.8 Viasat, Inc.

- 13.2.2 Asia Pacific

- 13.2.2.1 Bharat Electronics Limited

- 13.2.2.2 Hanwha Systems Co., Ltd.

- 13.2.2.3 LIG Nex1 Co., Ltd.

- 13.2.2.4 Mitsubishi Electric Corporation

- 13.2.3 Europe

- 13.2.3.1 Hensoldt AG

- 13.2.3.2 Indra Sistemas, S.A.

- 13.2.3.3 Leonardo S.p.A.

- 13.2.3.4 Saab AB

- 13.2.3.5 Thales Group

- 13.2.4 Middle East & Africa

- 13.2.4.1 Aselsan A.S.

- 13.2.4.2 Elbit Systems Ltd.

- 13.2.4.3 Israel Aerospace Industries Ltd.

- 13.2.1 North America

- 13.3 Niche Players/Disruptors

- 13.3.1 Ravpower