PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027580

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027580

Natural Refrigerants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

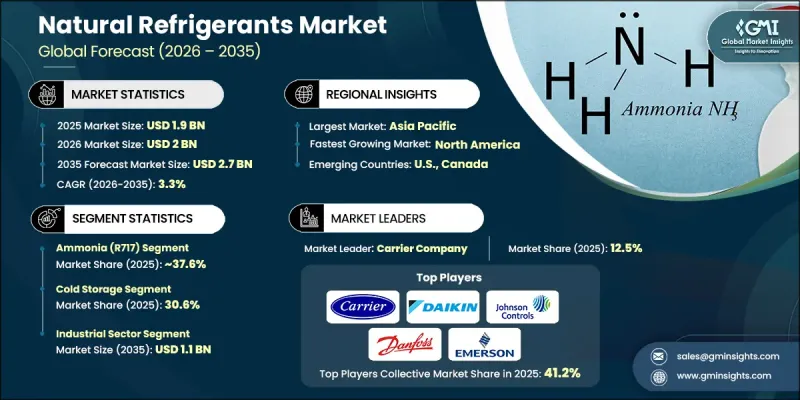

The Global Natural Refrigerants Market was valued at USD 1.9 billion in 2025 and is estimated to grow at a CAGR of 3.3% to reach USD 2.7 billion by 2035.

The global natural refrigerants industry is steadily transitioning from a compliance-driven segment into a core component of modern cooling and refrigeration system design. This shift is being supported by clear regulatory frameworks, rising demand for energy-efficient technologies, and increasing emphasis on sustainability objectives. Natural refrigerants are now being incorporated at the initial design stage of systems as organizations prioritize long-term environmental alignment and operational efficiency. Continuous improvements in system engineering are enhancing reliability, reducing operational risks, and enabling broader adoption across various end-use sectors. Advancements in system configurations and monitoring technologies are contributing to safer, more efficient operations, helping address earlier implementation-related concerns. As industries move toward environmentally responsible practices, natural refrigerants are becoming a preferred choice for next-generation cooling solutions, supporting consistent market expansion across global regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.9 Billion |

| Forecast Value | $2.7 Billion |

| CAGR | 3.3% |

Technological progress has significantly improved the practicality of natural refrigerants in refrigeration and cooling systems. Enhanced system designs, improved safety mechanisms, and advanced monitoring capabilities have strengthened operational performance and reduced perceived risks. These developments have streamlined installation processes, minimized system footprint, and simplified compliance with evolving safety standards, further accelerating adoption across commercial and industrial applications.

The ammonia (R717) segment accounted for 37.6% share in 2025 and is expected to grow at a CAGR of 2.5% through 2035. This segment continues to lead due to its established role in large-scale refrigeration applications and its consistent demand across industries that require reliable and efficient cooling solutions.

The air conditioning segment is projected to reach USD 308.9 million in 2026, although its overall share is expected to decline over time. Market expansion is increasingly being supported by emerging and specialized applications that require tailored system designs and infrastructure investments. Growth in these areas remains gradual and highly dependent on project-specific feasibility and technological adaptability.

North America Natural Refrigerants Market is anticipated to grow at a CAGR of 3.7% during 2026 to 2035. The region reflects a mature yet steadily advancing market environment, driven by regulatory efforts to reduce high global warming potential refrigerants and a growing need for replacement solutions. Demand is supported by widespread adoption across commercial and industrial sectors, along with increasing penetration in smaller-scale applications as efficiency standards and environmental considerations continue to influence purchasing decisions.

Key companies operating in the Global Natural Refrigerants Market include Daikin Industries, Carrier Corporation, Emerson, Danfoss, Johnson Controls, LG, Samsung, Midea, Gree, Honeywell, Linde plc, Air Liquide, and A-Gas International. Companies in the Natural Refrigerants Market are adopting strategic measures to strengthen their market presence and enhance competitive advantage. A strong emphasis is being placed on research and development to improve system efficiency, safety, and compatibility with evolving regulatory standards. Organizations are investing in advanced technologies to optimize product performance and reduce environmental impact. Strategic collaborations and partnerships are being pursued to expand technological capabilities and global reach. Companies are also focusing on expanding production capacities and strengthening distribution networks to meet rising demand across regions. Additionally, efforts are being directed toward product innovation and portfolio diversification to address a wider range of applications. Mergers and acquisitions are further enabling firms to gain market access, improve operational efficiency, and reinforce their long-term growth strategies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Refrigerant Type

- 2.2.3 Application

- 2.2.4 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Global shift to low-GWP refrigeration

- 3.2.1.2 Lifecycle energy-cost reductions

- 3.2.1.3 ESG and brand differentiation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Upfront capex and retrofit complexity

- 3.2.2.2 Safety, codes, and training gaps

- 3.2.2.3 Supply chain and parts availability

- 3.2.3 Market opportunities

- 3.2.3.1 Low-charge and packaged systems

- 3.2.3.2 Digital controls and heat recovery

- 3.2.3.3 Expanding cold-chain and data centers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By refrigerant type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Refrigerant Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Carbon Dioxide (CO2/R744)

- 5.3 Ammonia (R717)

- 5.4 Hydrocarbons

- 5.5 Water (R718)

- 5.6 Air (R729)

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cold storage

- 6.3 Freezers

- 6.4 Food processing

- 6.5 Air conditioners

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Industrial Sector

- 7.3 Commercial Sector

- 7.4 Residential Sector

- 7.5 Utility and Infrastructure Sector

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Carrier Corporation

- 9.2 Daikin Industries

- 9.3 Johnson Controls

- 9.4 Danfoss

- 9.5 Emerson

- 9.6 Gree

- 9.7 Midea

- 9.8 LG

- 9.9 Samsung

- 9.10 A-Gas International

- 9.11 Linde plc

- 9.12 Air Liquide

- 9.13 Honeywell