PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027590

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027590

Architectural Flat Glass Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

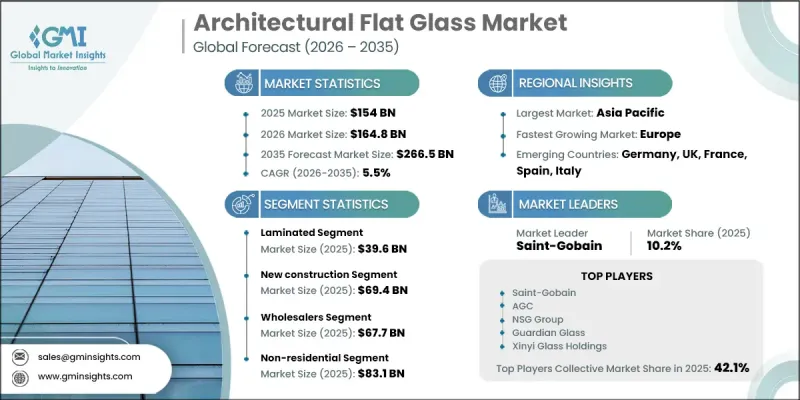

The Global Architectural Flat Glass Market was valued at USD 154 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 266.5 billion by 2035.

The market continues to gain momentum as modern construction increasingly integrates advanced materials that balance performance, design, and energy efficiency. Architectural flat glass, manufactured in uniform sheet form, plays a critical role in contemporary buildings due to its ability to deliver transparency, structural adaptability, and enhanced visual appeal. Its widespread adoption is driven by the growing need for natural light optimization, improved insulation, and aesthetically refined building envelopes. Advancements in coating technologies and fabrication processes have significantly improved thermal performance, solar control, and acoustic insulation, making flat glass a preferred solution in evolving architectural designs. The material is extensively utilized across both residential and commercial infrastructure, supporting the development of energy-efficient and sustainable buildings. In addition, rising urbanization and infrastructure investments are further reinforcing demand, while continuous innovation in glazing systems and design flexibility continues to shape the competitive landscape and long-term growth trajectory of the architectural flat glass market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $154 Billion |

| Forecast Value | $266.5 Billion |

| CAGR | 5.5% |

The new construction segment accounted for USD 69.4 billion in 2025 owing to the increasing volume of global infrastructure development. Builders prioritize high-performance materials that ensure durability, efficiency, and long-term operational value in newly developed structures. Architectural flat glass plays a central role in achieving these objectives by contributing to improved building performance and enhanced occupant experience. Alongside new developments, renovation and upgrade projects are also contributing to demand as property owners seek to enhance energy efficiency and modernize existing structures. The versatility of flat glass enables its application across various structural elements, supporting both functional and visual enhancements in construction projects.

The wholesaler segment generated USD 67.7 billion in 2025. Wholesalers facilitate large-scale distribution by ensuring consistent availability of diverse glass specifications required for complex construction activities. Their ability to manage inventory, logistics, and timely delivery supports contractors and fabricators in meeting project deadlines and quality standards. This distribution network strengthens market accessibility and enables efficient coordination between manufacturers and end users, thereby supporting overall industry growth.

North America Architectural Flat Glass Market was valued at USD 18.4 billion in 2025 and is anticipated to reach USD 31.4 billion by 2035. The region is witnessing rising demand for advanced glazing systems that enhance energy efficiency and building performance. Increasing adoption of innovative facade designs and high-performance coated glass is shaping construction trends across the region. The United States continues to drive regional demand, supported by ongoing residential upgrades and commercial development projects that emphasize improved insulation, daylight optimization, and modern design integration. Growing awareness of sustainable construction practices and regulatory standards is further accelerating the adoption of technologically advanced flat glass solutions.

Key companies operating in the Global Architectural Flat Glass Industry include Saint-Gobain, AGC, Guardian Glass, NSG Group, Xinyi Glass Holdings, Asahi India Glass, Central Glass, China Glass Holdings, CSG Holding, and Cardinal Glass Industries. Companies in the Architectural Flat Glass Market are strengthening their competitive position through continuous investment in advanced manufacturing technologies and product innovation. Many players are focusing on developing energy-efficient and high-performance glass solutions that align with evolving building standards and sustainability requirements. Strategic collaborations with construction firms and real estate developers are enabling companies to expand their project pipelines and enhance market reach. In addition, businesses are optimizing supply chain operations and expanding production capacities to meet rising global demand. Geographic expansion into emerging markets and diversification of product portfolios are also key approaches. Furthermore, companies are prioritizing research in coatings, smart glass technologies, and recyclable materials to maintain long-term competitiveness and reinforce their market presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product

- 2.2.2 Application

- 2.2.3 Sales Channel

- 2.2.4 End Use

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for daylight-focused designs

- 3.2.1.2 Rising use in modern building facades

- 3.2.1.3 Expanding renovation activities using new glazing

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 High energy-loss without proper insulation

- 3.2.2.2 Breakage risk during transport and installation

- 3.2.3 Opportunities

- 3.2.3.1 Growing interest in smart glazing solutions

- 3.2.3.2 Adoption of energy-efficient building materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Laminated

- 5.3 Tempered

- 5.4 Basic Float

- 5.5 Insulating

- 5.6 Decorative

- 5.7 Reflective

- 5.8 Prism & low-emissivity glass

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 New construction

- 6.3 Refurbishment

- 6.4 Interior construction

Chapter 7 Market Estimates and Forecast, By Sales Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Wholesalers

- 7.3 Online

- 7.4 Retailer

Chapter 8 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Non-Residential

- 8.3.1 Offices

- 8.3.2 Retail Spaces

- 8.3.3 Hospitality

- 8.3.3.1 Institutional

- 8.3.3.2 Healthcare facilities

- 8.3.3.3 Educational institutes

- 8.3.3.4 Transport facilities

- 8.3.3.5 Entertainment facilities

- 8.3.3.6 Others

- 8.4 Industrial

- 8.4.1 Manufacturing Facilities

- 8.4.2 Warehouses

- 8.4.3 Flex Space Buildings

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 AGC

- 10.2 Asahi India Glass

- 10.3 Cardinal Glass Industries

- 10.4 Central Glass

- 10.5 China Glass Holdings

- 10.6 CSG Holding

- 10.7 Saint-Gobain

- 10.8 Guardian Glass

- 10.9 NSG Group

- 10.10 Xinyi Glass Holdings