PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027594

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027594

Industrial Inkjet Printers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

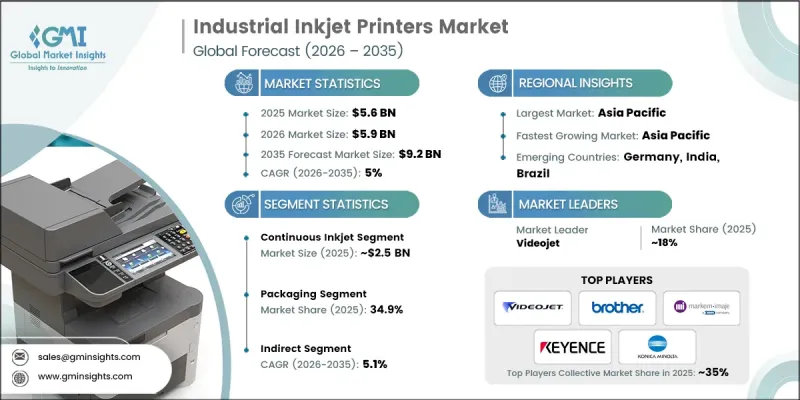

The Global Industrial Inkjet Printers Market was valued at USD 5.6 billion in 2025 and is estimated to grow at a CAGR of 5% to reach USD 9.2 billion by 2035.

Demand is driven by manufacturers across the packaging, textiles, and pharmaceutical industries who are increasingly using variable data printing to meet evolving business requirements. These printers allow for high-resolution printing of batch codes, barcodes, dates, and serial numbers on multiple substrates, offering flexibility for short production runs without extensive retooling. Industrial inkjet systems are gaining traction due to their cost-effectiveness, operational efficiency, and alignment with sustainable manufacturing practices, which reduce waste and energy consumption. Technological advancements in printheads, innovative ink formulations, and the integration of smart manufacturing solutions have significantly improved print quality. High-resolution printing capabilities now enable manufacturers to meet regulatory standards, enhance product traceability, and achieve superior marketing differentiation, making inkjet technology a key enabler of modern industrial production.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.6 Billion |

| Forecast Value | $9.2 Billion |

| CAGR | 5% |

The continuous inkjet (CIJ) segment generated USD 2.5 billion in 2025 and is expected to grow at a CAGR of 5.3% between 2026 and 2035. CIJ technology is widely adopted for its high-speed, non-contact printing ability, supporting dynamic information such as batch numbers, expiration dates, and barcodes. Its reliability in continuous operations with minimal maintenance makes it ideal for industries that demand high productivity and efficiency, including food and beverage, pharmaceuticals, automotive, and general manufacturing.

The packaging segment held an 34.9% share in 2025. Industrial inkjet printers are integral to packaging operations, providing essential functions such as batch coding, date marking, barcoding, and traceability. They can print on a variety of substrates including cardboard, plastic, metal, and film. The combination of precision, adaptability, and reliability has made these printers indispensable for modern packaging processes that demand accuracy and regulatory compliance.

U.S. Industrial Inkjet Printers Market reached USD 0.7 billion in 2025 and is expected to grow at a CAGR of 5.6% through 2035. The country's advanced manufacturing infrastructure and leadership in automation drive the adoption of inkjet systems across electronics, pharmaceuticals, and food processing industries. These printers support coding, marking, and labeling processes while ensuring consistent productivity, minimizing downtime, and integrating seamlessly with existing production lines.

Key players in the Global Industrial Inkjet Printers Market include Epson, HP, Domino Printing Sciences, Fujifilm, Konica Minolta, Videojet, Hitachi Industrial Equipment Systems, Canon, Markem-Imaje, Brother Industries, Durst Phototechnik, Leibinger Group, Mitsubishi Heavy Industries Printing & Packaging Machinery, and Electronics For Imaging. Companies in the Industrial Inkjet Printers Market are strengthening their position through product innovation, developing high-resolution and high-speed printing systems suitable for diverse industrial applications. They are expanding their portfolios with specialized inks and substrates to meet regulatory and environmental standards. Strategic partnerships and collaborations enhance distribution networks and provide localized technical support, while investment in research and development ensures the integration of AI and smart manufacturing capabilities. Firms are also focusing on cost efficiency and sustainability to attract environmentally conscious clients and improve operational productivity, solidifying their market presence globally.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Market estimates & forecasts parameters

- 1.4 Forecast Model

- 1.4.1 Key trends for market estimates

- 1.4.2 Quantified market impact analysis

- 1.4.2.1 Mathematical impact of growth parameters on forecast

- 1.4.3 Scenario analysis framework

- 1.5 Primary research and validation

- 1.5.1 Some of the primary sources (but not limited to)

- 1.6 Data mining sources

- 1.6.1 Paid Sources

- 1.7 Research Trail & confidence scoring

- 1.7.1 Research trail components

- 1.7.2 Scoring components

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 End Use Industry

- 2.2.4 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Component suppliers

- 3.1.3 Industrial inkjet printer manufacturers

- 3.1.4 System integrators & distributors

- 3.1.5 End-user manufacturing facilities

- 3.1.6 After-sales service & maintenance providers

- 3.1.7 Value addition at each stage

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for traceability & anti-counterfeiting solutions

- 3.2.1.2 Stringent regulatory requirements for product marking

- 3.2.1.3 E-commerce growth driving packaging & logistics coding demand

- 3.2.2 Market pitfalls

- 3.2.2.1 High initial capital investment for industrial-grade systems

- 3.2.2.2 Ink adhesion challenges on non-porous substrates

- 3.2.3 Opportunities

- 3.2.3.1 Emerging markets industrialization

- 3.2.3.2 Smart packaging integration

- 3.2.3.3 Pharmaceutical serialization mandates

- 3.2.3.4 Sustainable & eco-friendly ink development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Food Safety Modernization Act (FSMA)

- 3.4.2 FDA 21 CFR Part 11 - pharmaceutical marking standards

- 3.4.3 EU Food Information Regulation (EU) No. 1169/2011

- 3.4.4 GS1 standards for barcoding & serialization

- 3.4.5 Environmental regulations

- 3.5 Major market trends and disruptions

- 3.6 Technological and innovation landscape

- 3.6.1 Printhead technology advancements

- 3.6.2 Ink formulation innovations

- 3.6.3 Variable data printing & serialization capabilities

- 3.6.4 Industry 4.0 integration

- 3.6.5 High-speed printing technology evolution

- 3.7 Pricing analysis, 2025

- 3.7.1 By region

- 3.7.2 Historical price trend analysis (driven by primary research)

- 3.7.3 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.7.4 Regional price variation

- 3.7.5 Impact of raw material costs on pricing

- 3.8 Future market trends

- 3.9 Porter’s analysis

- 3.10 PESTLE analysis

- 3.11 Supply chain analysis

- 3.11.1 Printhead supply concentration

- 3.11.2 Ink supply chain structure

- 3.11.3 Geographic sourcing patterns

- 3.11.4 Supply chain vulnerabilities & mitigation strategies

- 3.12 Trade Data Analysis (Driven by paid database) (HS code- 84433250)

- 3.12.1 Import/Export Volume & Value Trends (Driven by Primary Research) (2019-2024)

- 3.12.2 Key trade corridors & tariff impact (driven by primary research)

- 3.13 Impact of AI & generative AI on the market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.2.1 Predictive maintenance using ai algorithms

- 3.13.2.2 Real-time quality control & defect detection

- 3.13.2.3 AI-optimized ink formulation & substrate matching

- 3.13.2.4 Automated workflow & production line integration

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Capacity & production landscape (driven by primary research)

- 3.14.1 Installed capacity by region & key producer

- 3.14.2 Capacity utilization rates & expansion pipeline

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Continuous inkjet

- 5.3 Drop on demand

- 5.4 UV inkjet

- 5.5 Other

Chapter 6 Market Estimates & Forecast, By End Use Industry, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Food & beverage

- 6.2.1 Beverage bottling & canning

- 6.2.2 Packaged food

- 6.2.3 Fresh produce labeling

- 6.3 Chemical

- 6.3.1 Industrial chemical container marking

- 6.3.2 Agrochemical packaging

- 6.3.3 Specialty chemical labeling

- 6.4 Pharmaceutical

- 6.4.1 Prescription drug packaging

- 6.4.2 OTC medication marking

- 6.4.3 Medical device marking

- 6.5 Packaging

- 6.6 Personal care & cosmetics

- 6.7 Others (automotive, etc.)

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Direct

- 7.3 Indirect

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 Brother Industries

- 9.2 Canon

- 9.3 Domino Printing Sciences

- 9.4 Durst Phototechnik

- 9.5 Electronics For Imaging

- 9.6 Epson

- 9.7 Fujifilm

- 9.8 Hitachi Industrial Equipment Systems

- 9.9 HP

- 9.10 Keyence

- 9.11 Konica Minolta

- 9.12 Leibinger Group

- 9.13 Markem-Imaje

- 9.14 Mitsubishi Heavy Industries Printing & Packaging Machinery

- 9.15 Videojet