PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027599

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027599

Ink Additive Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

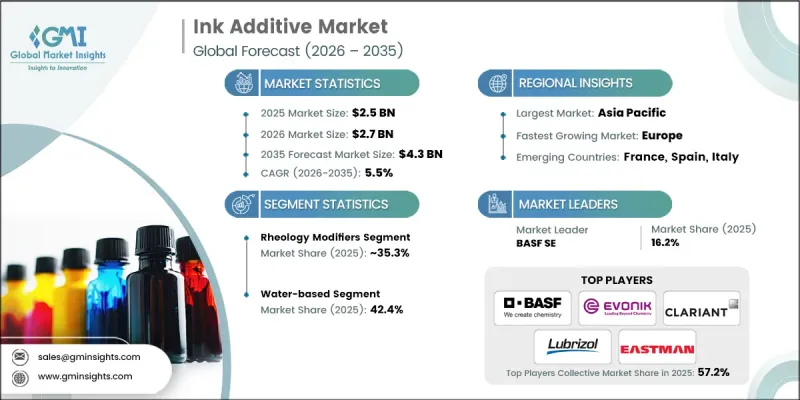

The Global Ink Additive Market was valued at USD 2.5 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 4.3 billion by 2035.

Ink additives consist of specialized chemical compounds designed to enhance the performance and characteristics of printing inks. These additives serve a wide range of functions, including viscosity adjustment, adhesion improvement, color enhancement, foam suppression, and drying control. The industry is driven by the printing sector's demand for higher-quality outcomes in publishing, packaging, and textile printing. Rapid technological advancements in printing processes have heightened the need for additives that improve ink performance while meeting evolving customer requirements. Environmental regulations and sustainability initiatives are encouraging the adoption of eco-friendly ink solutions, which reduce waste and VOC emissions, creating new market opportunities. As manufacturers seek to balance cost efficiency with regulatory compliance, the ink additive market is expected to expand steadily across all regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Billion |

| Forecast Value | $4.3 Billion |

| CAGR | 5.5% |

The rheology modifiers segment accounted for 35.3% share in 2025 and is expected to grow at a CAGR of 5.7% by 2035. Their growth is driven by the printing industry's requirement for precise viscosity control, which ensures uniform ink application and high-quality printing results. These modifiers enhance ink stability and flow characteristics, enabling optimal performance in modern printing technologies. Additionally, the push for environmentally sustainable printing practices is increasing demand for rheology modifiers derived from green sources, further supporting market expansion.

The water-based ink additives held 42.4% share in 2025. This segment's growth is fueled by rising consumer awareness and stringent environmental regulations that favor low-VOC and eco-friendly formulations. Water-based systems are increasingly preferred across multiple printing applications due to their minimal environmental impact, lower emissions, and improved health and safety profile, establishing them as a primary choice for sustainable printing operations.

North America Ink Additive Market is projected to grow at a CAGR of 5.6% from 2026 to 2035, driven by the region's packaging, publishing, and industrial printing sectors, which are increasingly adopting environmentally responsible solutions. Regulatory pressures, coupled with growing consumer expectations for biodegradable and recyclable ink products, are prompting manufacturers to innovate with additives that reduce VOC emissions and enhance ink recyclability while maintaining high performance.

Key players in the Ink Additive Industry include Evonik Industries AG, Clariant AG, BASF SE, Arkema S.A., Lubrizol Corporation, Eastman Chemical Company, Patcham FZC, Ashland, Munzing Corporation, Shamrock Technologies, and Elementis. Companies in the Ink Additive Market are strengthening their market foothold by investing in research and development to create environmentally sustainable and high-performance formulations. Strategic partnerships and joint ventures allow them to expand their regional presence and access new end-use sectors. Firms are focusing on customization, offering additives tailored to specific printing processes, substrates, and customer requirements. They are also implementing advanced production technologies to improve efficiency and consistency while reducing costs. Intellectual property development, technical support services, and compliance with evolving environmental standards help companies maintain long-term client relationships and reinforce their competitive positioning in the global ink additive market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Technology

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Demand for high-quality prints

- 3.2.1.2 Innovations in printing technologies

- 3.2.1.3 Trend towards customized and personalized printing solutions

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Customer expectations and changing market trends

- 3.2.2.2 Market fragmentation and competition

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for eco-friendly and biodegradable ink additives

- 3.2.3.2 Expansion of digital printing reducing reliance on traditional ink formulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Rheology modifiers

- 5.2.1 Synthetic water-based

- 5.2.2 Inorganic

- 5.2.3 Cellulosic

- 5.2.4 Solvent-based synthetic

- 5.3 Defoamers

- 5.4 Wetting agents

- 5.4.1 Mineral oil-based

- 5.4.2 Surfactant-based

- 5.4.3 Polymer-based

- 5.4.4 Silicone-based

- 5.4.5 Acrylic polymer-based

- 5.4.6 Fluorosurfactants

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Water-based

- 6.3 Solvent-based

- 6.4 UV and LED curing

- 6.5 Other

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Packaging

- 7.2.1 Flexible packaging

- 7.2.2 Rigid packaging

- 7.2.3 Labels & tags

- 7.2.4 Corrugated packaging

- 7.3 Publishing & commercial printing

- 7.4 Textile & garments

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 Arkema S.A.

- 9.3 Ashland

- 9.4 Clariant AG

- 9.5 Eastman Chemical Company

- 9.6 Elementis

- 9.7 Evonik Industries AG

- 9.8 Lubrizol Corporation

- 9.9 Munzing Corporation

- 9.10 Patcham FZC

- 9.11 Shamrock Technologies