PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027603

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027603

Herbal Personal Care Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

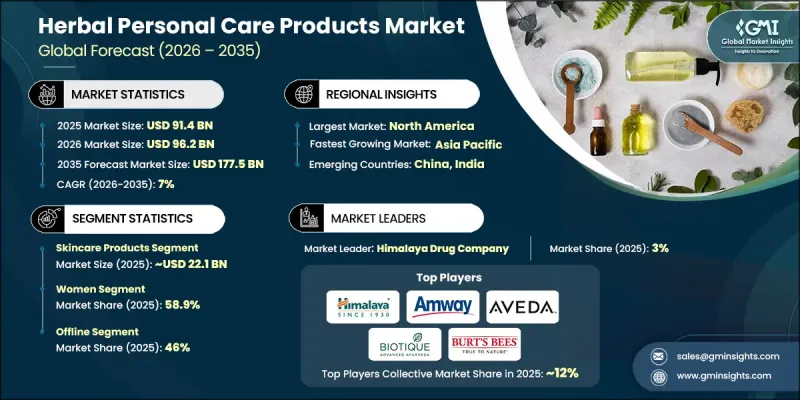

The Global Herbal Personal Care Products Market was valued at USD 91.4 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 177.5 billion by 2035.

Consumers are increasingly conscious of the harmful effects of synthetic chemicals like parabens, sulfates, phthalates, and artificial fragrances, which have reshaped purchasing behavior. Many shoppers now scrutinize labels, research ingredients online, and gravitate toward brands emphasizing transparency and "free-from" formulations. This shift has prompted both established and emerging companies to reformulate products to meet rising demand for cleaner, safer personal care solutions. Digital content, dermatologist recommendations, and influencer-led awareness campaigns are fueling this movement. Social media simplifies complex chemical information, educating consumers on risks and safer alternatives. The market favors products marketed as gentle, toxin-free, and naturally derived, and brands that highlight plant-based formulations are building trust while gaining a competitive edge in the evolving personal care landscape.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $91.4 Billion |

| Forecast Value | $177.5 Billion |

| CAGR | 7% |

The skincare segment generated USD 22.1 billion in 2025 and is expected to grow at a CAGR of 7.2% through 2035. Skincare leads the herbal personal care sector, driven by increasing concerns about acne, sensitivity, aging, and environmental damage. Consumers prefer herbal, chemical-free solutions, which are perceived as safer and more effective. Innovations in botanical extraction and active ingredient research have strengthened the appeal and credibility of herbal skincare products.

The women segment accounted for 58.9% share in 2025 and is anticipated to grow at a CAGR of 7.3% through 2035. Female consumers dominate demand for herbal personal care items, particularly skincare and haircare, influenced by clean-label preferences, wellness-focused lifestyles, and engagement with beauty routines. Social media, influencers, and personalized care regimens have further amplified women's impact on market growth, making them central to revenue generation.

U.S. Herbal Personal Care Products Market reached USD 22.6 billion in 2025 and is expected to grow at a CAGR of 7.5% from 2026 to 2035. Rising awareness of clean beauty and ingredient safety drives U.S. consumer adoption of herbal personal care products. Premium botanical formulations, strong retail networks, and digital presence have reinforced the country's market leadership. Women are particularly active in adopting herbal solutions, which supports sustained demand.

Major players in the Global Herbal Personal Care Products Market include Forest Essentials, Aveda Corporation, Dabur India Ltd., Lotus Herbals, Burt's Bees, Lush Fresh Handmade Cosmetics, Patanjali Ayurved Ltd., Weleda AG, Khadi Natural, Biotique, The Body Shop International Limited, Amway Corporation, Ecobee, Kama Ayurveda, and Oriflame Cosmetics. Companies in the Global Herbal Personal Care Products Market are strengthening their presence by investing heavily in research and development to enhance product efficacy and safety. They are expanding their portfolios to include premium and niche herbal offerings to cater to diverse consumer segments. Strategic collaborations with retailers, wellness brands, and digital platforms improve accessibility and brand visibility. Firms are leveraging influencer marketing and social media campaigns to educate consumers and build trust. Additionally, they are focusing on sustainable sourcing, eco-friendly packaging, and certifications to align with clean-label trends, while expanding into emerging markets to increase their global footprint and market share.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Market estimates & forecasts parameters

- 1.4 Forecast Model

- 1.4.1 Key trends for market estimates

- 1.4.2 Quantified market impact analysis

- 1.4.2.1 Mathematical impact of growth parameters on forecast

- 1.4.3 Scenario analysis framework

- 1.5 Primary research and validation

- 1.5.1 Some of the primary sources (but not limited to)

- 1.6 Data mining sources

- 1.6.1 Paid Sources

- 1.7 Primary research and validation

- 1.7.1 Primary sources

- 1.8 Research Trail & confidence scoring

- 1.8.1 Research trail components

- 1.8.2 Scoring components

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Skin type

- 2.2.4 Ingredient type

- 2.2.5 Form

- 2.2.6 Price

- 2.2.7 Consumer Group

- 2.2.8 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer awareness of harmful synthetic chemicals

- 3.2.1.2 Health & wellness trends driving natural product demand

- 3.2.1.3 Influencer marketing & social media impact

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 Market saturation & proliferation of misleading products

- 3.2.2.2 Consumer skepticism on efficacy claims

- 3.2.3 Opportunities

- 3.2.3.1 Digital-first brand emergence & D2C models

- 3.2.3.2 Ayurveda & traditional medicine integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 North America

- 3.7.1.1 US: Consumer Product Safety Commission (CPSC) 16 Code of Federal Regulations (CFR) part 1512

- 3.7.1.2 Canada: International Organization for Standardization (ISO) 4210

- 3.7.2 Europe

- 3.7.2.1 Germany: Deutsches Institut fur Normung (DIN) European Norm (EN) ISO 4210

- 3.7.2.2 UK: European Norm (EN) ISO 4210 / United Kingdom Conformity Assessed (UKCA)

- 3.7.2.3 France: European Norm (EN) ISO 4210

- 3.7.3 Asia Pacific

- 3.7.3.1 China: Guobiao (GB) 3565

- 3.7.3.2 India: Indian Standard (IS) 10613

- 3.7.3.3 Japan: Japanese Industrial Standard (JIS) D 9110

- 3.7.4 Latin America

- 3.7.4.1 Brazil: Associacao Brasileira de Normas Tecnicas (ABNT) Norma Brasileira (NBR) ISO 4210

- 3.7.4.2 Mexico: International Organization for Standardization (ISO) 4210

- 3.7.5 Middle East & Africa

- 3.7.5.1 South Africa: South African National Standard (SANS) 311

- 3.7.5.2 Saudi Arabia: Saudi Standards, Metrology and Quality Organization (SASO) Gulf Standardization Organization (GSO) ISO 4210

- 3.7.1 North America

- 3.8 Trade data analysis (HS Code - 30049011)

- 3.8.1 Import/export volume & value trends

- 3.8.2 Key trade corridors & tariff impact

- 3.9 Impact of ai & generative ai on the market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 Genai use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Skin care products

- 5.2.1 Face creams & lotions

- 5.2.2 Body creams & lotions

- 5.2.3 Moisturizers

- 5.2.4 Cleansers

- 5.2.5 Sunscreens

- 5.2.6 Anti-aging products

- 5.2.7 Serums

- 5.2.8 Other (exfoliators, eye creams, lip care etc.)

- 5.3 Oral care products

- 5.3.1 Toothpaste

- 5.3.2 Mouthwash

- 5.3.3 Tooth powder

- 5.3.4 Other (breath fresheners etc.)

- 5.4 Makeup and color cosmetics

- 5.4.1 Foundation

- 5.4.2 Lipsticks

- 5.4.3 Eyeliners

- 5.4.4 Powders

- 5.4.5 Others (makeup removers, blushes and highlighters)

- 5.5 Bath & Shower Products

- 5.5.1 Soaps

- 5.5.2 Shower gels

- 5.5.3 Bath oils

- 5.5.4 Bath salts

- 5.5.5 Others (bath bombs, scrubs etc.)

- 5.6 Fragrances

- 5.6.1 Perfumes

- 5.6.2 Deodorants

- 5.6.3 Body mists

- 5.6.4 Others (roll-ons, solid perfumes)

- 5.7 Baby care products

- 5.7.1 Shampoos

- 5.7.2 Lotions

- 5.7.3 Oils

- 5.7.4 Wipes

- 5.7.5 Powder

- 5.7.6 Others (diaper creams, etc.)

- 5.8 Grooming products

- 5.8.1 Beard oils

- 5.8.2 Aftershave lotions

- 5.8.3 Shaving creams

- 5.8.4 Others (waxing strips and kits, razors and trimmers etc.)

- 5.9 Hair care products

- 5.9.1 Shampoos

- 5.9.2 Conditioners

- 5.9.3 Hair oils

- 5.9.4 Hair masks

- 5.9.5 Hair serums

- 5.9.6 Other (hair tonics, hair sprays, hair dyes and colors etc.)

- 5.10 Others (intimate care, nail care etc.)

Chapter 6 Market Estimates & Forecast, By Skin Type 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Normal skin

- 6.3 Dry skin

- 6.4 Oily skin

- 6.5 Combination skin

- 6.6 Sensitive skin

Chapter 7 Market Estimates & Forecast, By Ingredient Type, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Plant-based ingredients

- 7.2.1 Aloe vera

- 7.2.2 Neem

- 7.2.3 Turmeric

- 7.2.4 Tulsi (Holy Basil)

- 7.2.5 Sandalwood

- 7.2.6 Others

- 7.3 Essential oils

- 7.3.1 Tea tree oil

- 7.3.2 Lavender oil

- 7.3.3 Eucalyptus oil

- 7.3.4 Rosemary oil

- 7.3.5 Peppermint oil

- 7.3.6 Others

- 7.4 Natural extracts

- 7.4.1 Fruit extracts

- 7.4.2 Flower extracts

- 7.4.3 Seed extracts

- 7.4.4 Root extracts

- 7.4.5 Other herbal ingredients

- 7.5 Other herbal ingredients (activated charcoal, dead sea minerals)

Chapter 8 Market Estimates & Forecast, By Form, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Creams

- 8.3 Lotions

- 8.4 Liquids

- 8.5 Bars

- 8.6 Gels

- 8.7 Oils

- 8.8 Others (foams, sprays, powders, aerosols)

Chapter 9 Market Estimates & Forecast, By Price Range, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Low

- 9.3 Medium

- 9.4 High

Chapter 10 Market Estimates & Forecast, By Consumer Group, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Men

- 10.3 Women

- 10.4 Children

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 Online

- 11.2.1 E-commerce

- 11.2.2 Company websites

- 11.3 Offline

- 11.3.1 Supermarkets/hypermarkets

- 11.3.2 Specialty stores

- 11.3.3 Pharmacies & drugstores

- 11.3.4 Department stores

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 Saudi Arabia

- 12.6.2 UAE

- 12.6.3 South Africa

Chapter 13 Company Profiles

- 13.1 Amway Corporation

- 13.2 Aveda Corporation

- 13.3 Biotique

- 13.4 Burt's Bees

- 13.5 Dabur India Ltd.

- 13.6 Forest Essentials

- 13.7 Himalaya Drug Company

- 13.8 Kama Ayurveda

- 13.9 Khadi Natural

- 13.10 Lotus Herbals

- 13.11 Lush Fresh Handmade Cosmetics

- 13.12 Oriflame Cosmetics

- 13.13 Patanjali Ayurved Ltd.

- 13.14 The Body Shop International Limited

- 13.15 Weleda AG