PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027605

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027605

Bumper Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

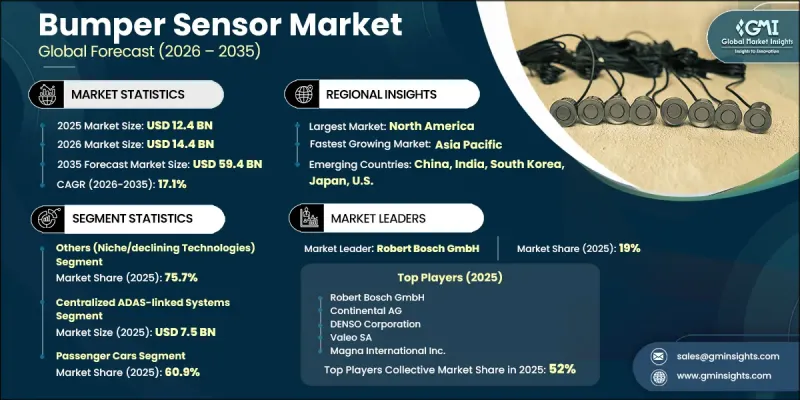

The Global Bumper Sensor Market was valued at USD 12.4 billion in 2025, and it is estimated to grow at a CAGR of 17.1% to reach USD 59.4 billion by 2035.

The market growth is linked to the rapid strengthening of vehicle safety regulations across major economies, alongside the rising integration of connected and wireless sensing systems in modern vehicles. Increasing urban congestion and limited parking space availability are also pushing the adoption of advanced parking assistance technologies, which directly support bumper sensor demand. At the same time, the accelerated deployment of Advanced Driver Assistance Systems (ADAS) is reinforcing the role of bumper-based sensing in collision prevention and real-time object detection. The market is also witnessing a structural shift toward sensor fusion, where ultrasonic, radar, and camera-based inputs are combined to improve detection accuracy and reduce errors in judgment. Growing consumer preference for safer driving experiences, combined with OEM focus on automation-ready vehicle platforms, is further strengthening product adoption. Expanding passenger vehicle production, increasing penetration in both OEM and aftermarket channels, and continuous advancements in electronic control systems are collectively shaping a strong long-term growth trajectory for the industry across global automotive ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.4 Billion |

| Forecast Value | $59.4 Billion |

| CAGR | 17.1% |

The centralized ADAS-linked systems segment reached USD 7.5 billion in 2025. These systems consolidate inputs from bumper sensors, radar units, and camera modules into a unified processing architecture that enables coordinated safety responses. They are widely implemented across passenger and commercial vehicles to support collision avoidance, emergency braking functions, and automated parking assistance. Their integration into electronic control units improves system reliability and ensures compliance with evolving safety standards, which continues to drive their widespread adoption across modern automotive platforms.

The sensor fusion (architecture-driven integration) segment is projected to grow at a CAGR of 16.8% during 2026-2035. Growth in this segment is driven by increasing deployment of integrated ADAS ecosystems that combine multiple sensing technologies into a single decision-making framework. This approach enhances object detection accuracy, strengthens response time, and supports semi-automated driving capabilities in vehicles. It also helps reduce false detection signals and improves overall system reliability, which is encouraging automotive manufacturers to standardize fused sensor architectures across both mid-range and premium vehicle categories.

North America Bumper Sensor Market accounted for 36.3% share in 2025, supported by strict vehicle safety enforcement and a strong emphasis on reducing road accidents through advanced automotive technologies. Regulatory frameworks in the United States continue to evolve toward enhanced oversight of driver assistance technologies, encouraging wider deployment of safety monitoring systems in vehicles. Continuous investment from government bodies and industry participants in research programs focused on crash prevention and intelligent mobility solutions is also strengthening the regional adoption of bumper sensor technologies.

The Bumper Sensor Industry includes several key players such as ZF Friedrichshafen AG, Robert Bosch GmbH, NXP Semiconductors, Sensata Technologies, Valeo SA, Analog Devices, Inc., Continental AG, DENSO Corporation, Hyundai Mobis, Aptiv PLC, Magna International Inc., Murata Manufacturing Co., Ltd., Hitachi Automotive Systems, Infineon Technologies AG, and LeddarTech Inc. Companies operating in the Bumper Sensor Market are focusing on strengthening their position through aggressive investment in ADAS integration and next-generation sensor fusion platforms. They are expanding product portfolios to include highly integrated ultrasonic, radar, and camera-based sensing solutions that improve detection accuracy and reduce system complexity. Strategic partnerships with automotive OEMs are being prioritized to secure early design integration in upcoming vehicle platforms. Firms are also investing in software-driven sensing intelligence, enabling real-time data processing and predictive safety functions. Cost optimization through semiconductor advancements and miniaturized sensor designs is another key focus area, helping manufacturers scale production efficiently.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Technology trends

- 2.2.2 System architecture trends

- 2.2.3 Application trends

- 2.2.4 Vehicle type trends

- 2.2.5 Sales channel trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global NCAP safety compliance requirements

- 3.2.1.2 Increasing ADAS penetration in mid-range vehicles

- 3.2.1.3 Growing urban parking constraints boosting sensor adoption

- 3.2.1.4 OEM integration of ultrasonic sensors as standard features

- 3.2.1.5 Expansion of autonomous driving feature pipelines

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Sensor performance degradation in extreme weather conditions

- 3.2.2.2 Integration complexity with multi-sensor ADAS architectures

- 3.2.3 Market opportunities

- 3.2.3.1 Transition toward software-defined vehicle sensor ecosystems

- 3.2.3.2 Increasing aftermarket retrofitting demand in developing regions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Ultrasonic sensors

- 5.3 Radar sensors (short-range)

- 5.4 Sensor fusion (architecture-driven integration)

- 5.5 Others (niche/declining technologies)

Chapter 6 Market Estimates and Forecast, By System Architecture, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Standalone sensors

- 6.3 Integrated bumper sensor systems

- 6.4 Centralized ADAS-linked systems

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Parking assistance systems (PAS)

- 7.3 Blind spot detection (BSD)

- 7.4 Rear cross traffic alert (RCTA)

- 7.5 Low-speed collision avoidance

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.3 Commercial vehicles

Chapter 9 Market Estimates and Forecast, By Sales Channel, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 OEM (original equipment manufacturer)

- 9.3 Aftermarket

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Robert Bosch GmbH

- 11.1.2 Continental AG

- 11.1.3 DENSO Corporation

- 11.1.4 Valeo SA

- 11.1.5 Magna International Inc.

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Aptiv PLC

- 11.2.1.2 LeddarTech Inc.

- 11.2.1.3 Sensata Technologies

- 11.2.2 Asia Pacific

- 11.2.2.1 Hyundai Mobis

- 11.2.2.2 Hitachi Automotive Systems

- 11.2.2.3 Murata Manufacturing Co., Ltd.

- 11.2.2.4 NXP Semiconductors

- 11.2.3 Europe

- 11.2.3.1 ZF Friedrichshafen AG

- 11.2.3.2 Infineon Technologies AG

- 11.2.1 North America

- 11.3 Niche Players/Disruptors

- 11.3.1 Analog Devices, Inc.