PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027643

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027643

Silicon Monoxide Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

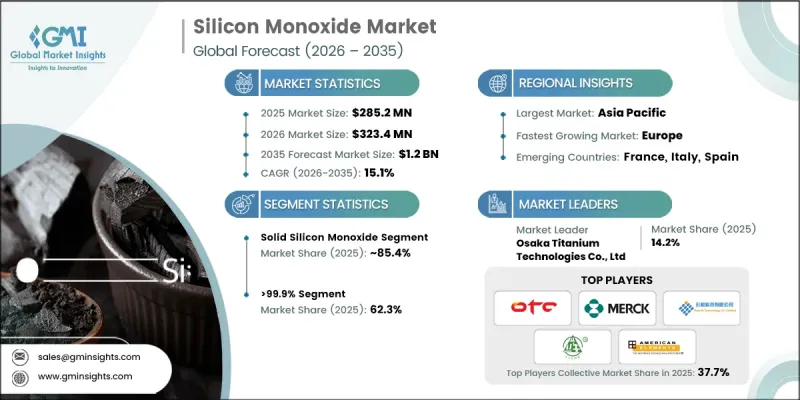

The Global Silicon Monoxide Market was valued at USD 285.2 million in 2025 and is estimated to grow at a CAGR of 15.1% to reach USD 1.2 billion by 2035.

Silicon monoxide is a chemical compound composed of equal parts silicon and oxygen atoms, primarily serving as a precursor for silicon dioxide, commonly known as silica. Its versatile properties, including energy density, thermal stability, and electrical conductivity, make it a critical material across diverse industries such as electronics, ceramics, and solar energy. The market is experiencing significant growth due to rising demand from electric vehicle batteries, energy storage systems, and consumer electronics. Rapid industrialization in the Asia-Pacific region is creating opportunities for technological innovation and business expansion. However, high production costs and supply chain complexities pose challenges, as manufacturing requires precise control over reaction parameters and careful material selection, which can limit capacity and influence pricing dynamics in a competitive environment.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $285.2 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 15.1% |

The solid silicon monoxide held an 85.4% share in 2025. The material is the backbone of the silicon monoxide industry due to its stability, high electrical conductivity, and adaptability for multiple industrial applications. Solid silicon monoxide is critical in battery production, semiconductor fabrication, and ceramic manufacturing because it maintains consistent performance over extended operational cycles. Its robustness makes it ideal for applications demanding high durability and reliability. Companies prefer solid silicon monoxide as a core input because its versatile characteristics allow tailored solutions for specific technological and industrial needs, enhancing product efficiency and lifecycle performance.

The purities exceeding 99.9% accounted for 62.3% share in 2025. These ultra-high-purity grades are essential for advanced electronics, semiconductor manufacturing, and high-performance battery technologies. The exceptional purity ensures maximum electrical conductivity, thermal stability, and overall material reliability, making it indispensable in applications that demand precision and longevity. High-purity silicon monoxide underpins innovations in cutting-edge devices and energy storage systems, positioning it as a critical driver of market growth across high-tech sectors.

North America Silicon Monoxide Market was valued at USD 89.6 million in 2025 and is expected to grow at a CAGR of 14.8% between 2026 and 2035. Led by the U.S. and Canada, this region represents a major hub due to the presence of advanced electronics, aerospace, and healthcare industries. The demand for ultra-pure materials is particularly high in North America because of research-intensive semiconductor fabrication, energy storage development, and technology-driven manufacturing. These applications require consistent quality and high-performance standards, driving the adoption of silicon monoxide across various industrial sectors.

Key players operating in the Global Silicon Monoxide Market include ACS Material, American Elements, FUJIFILM Wako Pure Chemical Corporation, BTR New Material Group Co., Ltd, LICHE OPTO GROUP CO., LTD, Lorad Chemical Corporation, Merck, Nanochemazone, Osaka Titanium Technologies Co., Ltd., and Shenzhen Rearth Technology Co., Ltd. Market participants are strengthening their presence through strategic initiatives such as investing in high-capacity, precision-controlled production facilities to ensure consistent product quality. Companies are enhancing R&D efforts to improve material purity, optimize reaction processes, and develop application-specific formulations. Strategic partnerships, mergers, and acquisitions are being leveraged to expand regional footprints, particularly in emerging markets. Additionally, businesses are focusing on supply chain optimization, vertical integration, and technology-driven manufacturing solutions to reduce costs and improve efficiency. Offering technical support, custom material solutions, and long-term contracts with electronics, battery, and ceramic manufacturers further helps firms secure client loyalty and enhance market share in a highly competitive global environment.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Purity

- 2.2.4 End use industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid growth in lithium-ion battery demand for EVs

- 3.2.1.2 Superior anode performance vs. traditional graphite

- 3.2.1.3 Expansion of consumer electronics market

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volume expansion issues in battery cycling

- 3.2.2.2 Higher cost vs. conventional graphite anodes

- 3.2.3 Market opportunities

- 3.2.3.1 Development of next-generation EV batteries

- 3.2.3.2 Solid-state battery commercialization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Gaseous silicon monoxide

- 5.3 Solid silicon monoxide

- 5.3.1 Powder

- 5.3.2 Granules

Chapter 6 Market Estimates and Forecast, By Purity, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 >99.9%

- 6.3 99-99.9%

Chapter 7 Market Estimates and Forecast, By End-User Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive & transportation

- 7.2.1 Electric vehicles (EV battery anodes)

- 7.2.2 Hybrid electric vehicles (HEV)

- 7.2.3 Automotive electronics & displays

- 7.2.4 Others

- 7.3 Consumer electronics

- 7.3.1 Smartphones & tablets

- 7.3.2 Laptops & personal computers

- 7.3.3 Wearable devices

- 7.3.4 Others

- 7.4 Energy & power

- 7.4.1 Grid-scale energy storage systems

- 7.4.2 Residential & commercial battery storage

- 7.4.3 Renewable energy integration systems

- 7.4.4 Others

- 7.5 Industrial & manufacturing

- 7.5.1 Material processing equipment

- 7.5.2 Industrial coatings & surface treatment

- 7.5.3 Semiconductor manufacturing equipment

- 7.5.4 Optical equipment manufacturing

- 7.5.5 Others

- 7.6 Aerospace & defense

- 7.6.1 Aircraft systems & components

- 7.6.2 Satellite & space applications

- 7.6.3 Defense electronics

- 7.6.4 Others

- 7.7 Healthcare & medical devices

- 7.7.1 Medical equipment batteries

- 7.7.2 Diagnostic device components

- 7.7.3 Implantable device applications

- 7.7.4 Others

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 ACS Material

- 9.2 American Elements

- 9.3 BTR New Material Group Co., Ltd

- 9.4 FUJIFILM Wako Pure Chemical Corporation

- 9.5 LICHE OPTO GROUP CO., LTD

- 9.6 Lorad Chemical Corporation

- 9.7 Merck

- 9.8 Nanochemazone

- 9.9 Osaka Titanium Technologies Co., Ltd.

- 9.10 Shenzhen rearth technology Co Ltd