PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027644

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027644

Sparkling Wine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

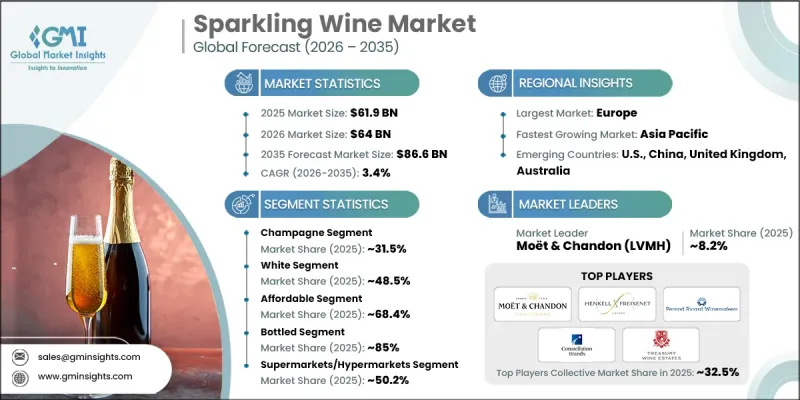

The Global Sparkling Wine Market was valued at USD 61.9 billion in 2025 and is estimated to grow at a CAGR of 3.4% to reach USD 86.6 billion by 2035.

The industry continues to evolve as consumer preferences shift toward premium alcoholic beverages that align with both celebratory occasions and everyday indulgence. Sparkling wine, known for its natural effervescence and refined appeal, is produced using multiple fermentation techniques and is offered across a broad spectrum of styles and sweetness levels. Its versatility across consumption occasions, combined with growing accessibility across price tiers, has strengthened its global demand. The market is further supported by rising interest in premiumization, where consumers increasingly seek high-quality beverages that deliver both experience and value. Expanding digital retail channels and broader distribution networks are also enhancing product visibility and accessibility. Additionally, sustainability has become a central focus, with producers adopting environmentally responsible practices, improving packaging efficiency, and integrating cleaner production processes. Continuous innovation in branding, packaging formats, and production techniques is shaping a competitive and dynamic landscape, reinforcing the long-term growth outlook of the sparkling wine market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $61.9 Billion |

| Forecast Value | $86.6 Billion |

| CAGR | 3.4% |

The champagne segment accounted for 31.5% share in 2025 and is anticipated to grow at a CAGR of 3.6% through 2035. Its leadership position is supported by strong global recognition, premium positioning, and strict production standards that ensure consistent quality. The category benefits from established brand value, controlled origin practices, and a production process that enhances complexity and depth, making it a preferred choice in high-end consumption segments.

The white sparkling wine segment held a 48.5% in 2025 and is forecast to grow at a CAGR of 3.5% during the study period. Its dominance is driven by broad consumer acceptance, adaptability across various consumption occasions, and compatibility with a wide range of culinary pairings. The segment continues to attract demand due to its balanced flavor profile, visual appeal, and consistent performance across both premium and accessible product categories.

U.S. Sparkling Wine Market generated USD 9.8 billion in 2025, contributing significantly to regional growth. Market expansion in North America is supported by evolving consumption habits, increasing preference for premium beverages, and the rising popularity of sparkling wine in casual as well as formal settings. Strong retail presence, expanding distribution channels, and growing consumer awareness continue to support steady market development.

Key players operating in the Global Sparkling Wine Industry include Moet & Chandon (LVMH), Henkell Freixenet, Pernod Ricard Winemakers, Constellation Brands, Treasury Wine Estates, E & J Gallo Winery, Accolade Wines, Casella Family Brands, Vina Concha Y Toro, Bronco Wine Company, Schramsberg Vineyards, Caviro Extra, Giulio Cocchi Spumanti Srl, and Illinois Sparkling Co. Companies in the Sparkling Wine Market are strengthening their competitive position by focusing on premium product development, sustainable production practices, and brand differentiation strategies. Producers are investing in advanced fermentation technologies and improved vineyard management to enhance quality and consistency. Sustainability initiatives, including eco-friendly packaging and reduced carbon emissions, are becoming central to long-term strategies. Businesses are also expanding their presence through digital platforms and direct-to-consumer channels to improve accessibility and engagement. Strategic partnerships, acquisitions, and geographic expansion into emerging markets are helping companies broaden their customer base.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product

- 2.2.2 Type

- 2.2.3 Price

- 2.2.4 Packaging Type

- 2.2.5 Distribution channel

- 2.2.6 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Million Litres)

- 5.1 Key trends

- 5.2 Champagne

- 5.3 Prosecco

- 5.4 Cava

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Million Litres)

- 6.1 Key trends

- 6.2 Red

- 6.3 White

- 6.4 Rose

Chapter 7 Market Estimates and Forecast, By Price, 2022-2035 (USD Billion) (Million Litres)

- 7.1 Key trends

- 7.2 Luxury

- 7.3 Affordable

Chapter 8 Market Estimates and Forecast, By Packaging Type, 2022-2035 (USD Billion) (Million Litres)

- 8.1 Key trends

- 8.2 Bottled

- 8.3 Canned

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Million Litres)

- 9.1 Key trends

- 9.2 Supermarkets/Hypermarkets

- 9.3 Specialty Stores

- 9.4 Online Retail

- 9.5 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Million Litres)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Moet & Chandon (LVMH)

- 11.2 Henkell Freixenet

- 11.3 Pernod Ricard Winemakers

- 11.4 Constellation Brands

- 11.5 Treasury Wine Estates

- 11.6 E & J Gallo Winery

- 11.7 Accolade Wines

- 11.8 Casella Family Brands

- 11.9 Vina Concha Y Toro

- 11.10 Bronco Wine Company

- 11.11 Schramsberg Vineyards

- 11.12 Caviro Extra

- 11.13 Giulio Cocchi Spumanti Srl