PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027648

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027648

Uncooked Pasta and Noodles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

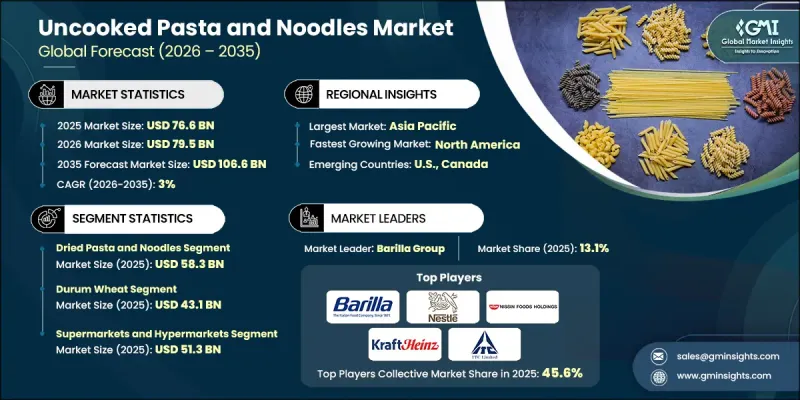

The Global Uncooked Pasta and Noodles Market was valued at USD 76.6 billion in 2025 and is estimated to grow at a CAGR of 3% to reach USD 106.6 billion by 2035.

Uncooked pasta and noodles are dough-based food products prepared from wheat flour or other grain flours blended with water, and in some cases eggs or salt, which are then shaped and preserved through drying or packaged in fresh form for later cooking. These products are widely consumed across global cuisines, with pasta strongly linked to European dietary traditions and noodles deeply rooted in Asian food cultures. The dry form retains a firm structure that softens only after boiling, making it suitable for long-term storage and easy preparation. Durum wheat semolina is widely used in pasta production due to its high protein content, which helps maintain firmness and elasticity after cooking. Noodles are produced using a broader range of raw materials, including rice-based and buckwheat-based flours, depending on regional preferences and culinary practices. The drying process plays a vital role in reducing moisture content, extending shelf life, and preventing microbial growth, while also supporting efficient transportation and global distribution. Ongoing advancements in production technologies are further improving quality consistency, processing efficiency, and product variety across the industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $76.6 Billion |

| Forecast Value | $106.6 Billion |

| CAGR | 3% |

The dried pasta and noodles segment reached USD 58.3 billion in 2025. This category continues to dominate the market due to its long shelf stability, cost-effectiveness, and ease of storage compared to alternative forms. Its convenience and versatility have made it a staple in household cooking as well as foodservice operations, supporting consistent demand across both residential and commercial consumption channels.

The durum wheat segment reached USD 43.1 billion in 2025. This raw material is widely used in pasta manufacturing due to its high protein content and strong gluten-forming properties, which contribute to desirable texture and cooking performance. The coarse milling of durum wheat semolina enables the production of pasta with a firm structure that holds its shape during cooking, ensuring the characteristic bite and texture associated with traditional pasta products.

The key companies operating in the Uncooked Pasta and Noodles Market include Nissin Foods Holdings, Kraft Heinz Company, Barilla Group, Toyo Suisan Kaisha, Nestle, ITC, Unilever, Campbell Soup Company, Ebro Foods, TreeHouse Foods, De Cecco, and Jovial Foods. Key strategies adopted by companies in the Uncooked Pasta and Noodles Market focus on expanding product portfolios through innovation in ingredient composition, including high-protein, gluten-free, and enriched formulations to meet evolving dietary preferences. Manufacturers are increasingly investing in advanced production technologies to enhance texture consistency, shelf life, and cooking performance. Strategic expansion of distribution networks across retail and online channels is strengthening global reach and improving product accessibility. Companies are also emphasizing branding and premiumization strategies to differentiate offerings in a competitive market. Partnerships with foodservice providers and retail chains are helping to increase volume sales and market penetration. Additionally, firms are focusing on sustainable sourcing of grains and improving packaging solutions to extend shelf stability while aligning with environmental expectations. Continuous investment in R&D is further enabling the development of region-specific product variations to cater to diverse culinary traditions and consumer preferences worldwide.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Form

- 2.2.2 Raw Material

- 2.2.3 Distribution Channel

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for affordable staple foods drives market expansion

- 3.2.1.2 Growth in food service and quick-service restaurants boosts bulk consumption

- 3.2.1.3 Rising urban populations support higher packaged food sales

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 Volatile wheat prices pressure manufacturer margins

- 3.2.2.2 Supply chain disruptions affect raw material stability

- 3.2.3 Opportunities

- 3.2.3.1 Long shelf life supports large-scale distribution and exports

- 3.2.3.2 Regional flavor customization can expand consumer base

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By form

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Dried pasta and noodles

- 5.3 Ambient/canned pasta and noodles

- 5.4 Chilled/frozen pasta and noodles

Chapter 6 Market Estimates and Forecast, By Raw Material, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Semolina

- 6.3 Flour

- 6.4 Durum wheat

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Supermarkets and hypermarkets

- 7.3 Convenience stores

- 7.4 Online retail

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Barilla Group

- 9.2 Nestle

- 9.3 ITC

- 9.4 Kraft Heinz Company

- 9.5 Unilever

- 9.6 Toyo Suisan Kaisha

- 9.7 Nissin Foods Holdings

- 9.8 Campbell Soup Company

- 9.9 TreeHouse Foods

- 9.10 Ebro Foods

- 9.11 De Cecco

- 9.12 Jovial Foods