PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027654

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027654

Satellite Launch Vehicle (SLV) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

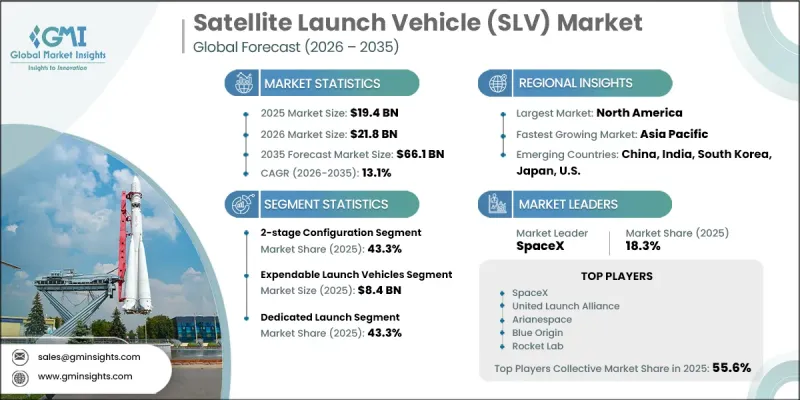

The Global Satellite Launch Vehicle (SLV) Market was valued at USD 19.4 billion in 2025 and is estimated to grow at a CAGR of 13.1% to reach USD 66.1 billion by 2035.

The market is advancing rapidly as the space industry undergoes a structural transformation driven by increasing satellite deployments and evolving mission requirements. Rising demand for low Earth orbit infrastructure, combined with the growing number of satellite-based services, is significantly boosting launch activity worldwide. Governments and private organizations are actively investing in space programs to strengthen communication, navigation, and surveillance capabilities, which is further accelerating demand for reliable launch systems. Technological progress in reusable launch vehicles and propulsion systems is improving cost efficiency and operational frequency, making space access more commercially viable. In addition, increasing interest in deep space exploration and next-generation missions is creating new growth avenues. The expansion of small satellite ecosystems and the need for rapid deployment capabilities are also influencing the design and scalability of launch systems, reinforcing long-term growth prospects for the satellite launch vehicle market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $19.4 Billion |

| Forecast Value | $66.1 Billion |

| CAGR | 13.1% |

The 2-stage configuration segment accounted for a 43.3% share in 2025, owing to its balanced performance characteristics and operational efficiency. These launch systems are widely adopted because they offer dependable mission execution while optimizing payload capacity and cost. Their streamlined architecture supports frequent launch cycles and enables operators to meet growing demand for satellite deployment. Continued improvements in propulsion efficiency and structural design further enhance their reliability, making them a preferred choice across a wide range of orbital missions.

The dedicated launch segment held a 43.3% share in 2025, generating the highest revenue contribution within the market. This segment is gaining strong traction due to its ability to provide customized launch services tailored to specific mission requirements. Dedicated launches allow operators to achieve precise orbital placement and mission flexibility, which is critical for high-value payloads. Increasing demand for assured launch schedules and mission-specific configurations continues to strengthen the segment's position, particularly among government and commercial stakeholders.

North America Satellite Launch Vehicle (SLV) Market accounted for 36.3% share in 2025, supported by a well-established space ecosystem and continuous investment in advanced technologies. The region benefits from strong collaboration between public institutions and private enterprises, which is driving innovation and accelerating commercialization. Policy support, funding initiatives, and streamlined regulatory frameworks are enabling faster development and deployment of launch systems. Ongoing focus on national security, space exploration, and technological leadership continues to reinforce regional market expansion.

Key companies operating in the Global Satellite Launch Vehicle (SLV) Industry include SpaceX, Arianespace, United Launch Alliance, Blue Origin, Northrop Grumman, Rocket Lab, Relativity Space, Firefly Aerospace, Astra Space, Mitsubishi Heavy Industries, Avio S.p.A., China Aerospace Science and Technology Corporation (CASC), ISRO (via NSIL/Antrix), LandSpace, and Roscosmos. Companies in the Global Satellite Launch Vehicle (SLV) Market are strengthening their position by investing heavily in reusable launch technologies and advanced propulsion systems to reduce costs and improve launch frequency. Strategic partnerships with satellite operators and government agencies are helping secure long-term launch contracts and ensure stable revenue streams. Firms are also expanding their launch infrastructure and global presence to support increasing mission demand. Continuous innovation in vehicle design, including modular and scalable platforms, is enabling companies to cater to diverse payload requirements. Additionally, organizations are focusing on vertical integration, in-house manufacturing, and rapid production capabilities to enhance efficiency and maintain a competitive edge in the evolving space economy.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Vehicle type trends

- 2.2.2 Launch platform trends

- 2.2.3 Orbit type trends

- 2.2.4 Vehicle configuration trends

- 2.2.5 Propellant type trends

- 2.2.6 Launch type trends

- 2.2.7 Application trends

- 2.2.8 End-user trends

- 2.2.9 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 LEO mega-constellation deployments accelerating launch demand

- 3.2.1.2 Defense budgets increasing sovereign launch capabilities globally

- 3.2.1.3 Small satellite proliferation driving high-frequency launches

- 3.2.1.4 Deep space and lunar missions increasing heavy-lift demand

- 3.2.1.5 Commercial Earth observation expanding multi-orbit deployment needs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Launch failure risks impacting insurance premiums and contracts

- 3.2.2.2 Supply chain constraints in propulsion and avionics components

- 3.2.3 Market opportunities

- 3.2.3.1 Dedicated small satellite launch services replacing rideshare dependency

- 3.2.3.2 Green propulsion systems gaining traction amid sustainability mandates

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Small-lift launch vehicles (<2,000 kg to LEO)

- 5.3 Medium-lift launch vehicles (2,000-20,000 kg to LEO)

- 5.4 Heavy-lift launch vehicles (20,000-50,000 kg to LEO)

- 5.5 Ultra-heavy lift launch vehicles (>50,000 kg to LEO)

Chapter 6 Market Estimates and Forecast, By Launch Platform, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Expendable launch vehicles

- 6.3 Partially reusable launch vehicles

- 6.4 Fully reusable launch vehicles

Chapter 7 Market Estimates and Forecast, By Orbit Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Low earth orbit (LEO)

- 7.3 Medium earth orbit (MEO)

- 7.4 Geostationary orbit (GEO)

- 7.5 Beyond earth orbit

Chapter 8 Market Estimates and Forecast, By Vehicle Configuration, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 2-stage configuration

- 8.3 3-stage configuration

- 8.4 4+ stage configuration

Chapter 9 Market Estimates and Forecast, By Propellant Type, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Liquid propellant

- 9.3 Cryogenic propellant

- 9.4 Solid propellant

- 9.5 Hybrid propellant

Chapter 10 Market Estimates and Forecast, By Launch Type, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 Dedicated launch

- 10.3 Rideshare launch

- 10.4 Responsive/on-demand launch

Chapter 11 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 Commercial communication

- 11.3 Earth observation & remote sensing

- 11.4 Navigation

- 11.5 Scientific research & government missions

- 11.6 Defense & national security

- 11.7 Technology demonstration & rideshare missions

Chapter 12 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 12.1 Key trends

- 12.2 Government space agencies

- 12.3 Commercial satellite operators

- 12.4 Defense & military organizations

- 12.5 Academic & research institutions

Chapter 13 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 U.S.

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Spain

- 13.3.5 Italy

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 Australia

- 13.4.5 South Korea

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.6 Middle East and Africa

- 13.6.1 South Africa

- 13.6.2 Saudi Arabia

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Global Key Players

- 14.1.1 SpaceX

- 14.1.2 Arianespace

- 14.1.3 United Launch Alliance

- 14.1.4 China Aerospace Science and Technology Corporation (CASC)

- 14.1.5 Roscosmos

- 14.2 Regional key players

- 14.2.1 North America

- 14.2.1.1 Blue Origin

- 14.2.1.2 Northrop Grumman

- 14.2.2 Asia Pacific

- 14.2.2.1 ISRO (via NSIL/Antrix)

- 14.2.2.2 Mitsubishi Heavy Industries

- 14.2.3 Europe

- 14.2.3.1 Avio S.p.A.

- 14.2.1 North America

- 14.3 Niche Players/Disruptors

- 14.3.1 Rocket Lab

- 14.3.2 Firefly Aerospace

- 14.3.3 Relativity Space

- 14.3.4 Astra Space

- 14.3.5 LandSpace