PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027668

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027668

Yogurt Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

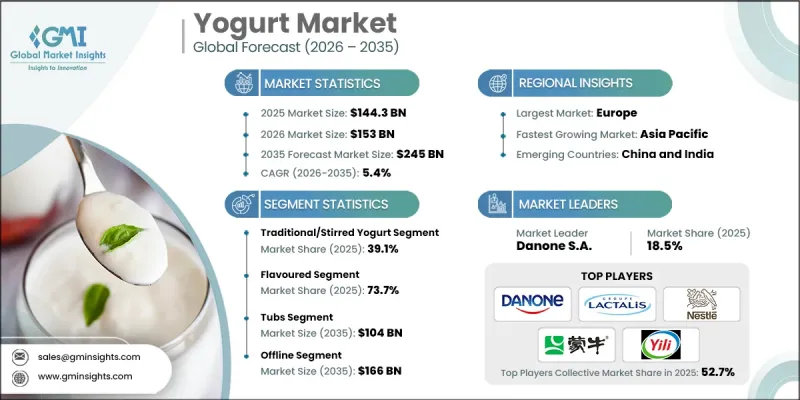

The Global Yogurt Market was valued at USD 144.3 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 245 billion by 2035.

The global yogurt industry is experiencing sustained growth driven by rising consumer awareness surrounding digestive health and immune support. Demand for nutrient-enriched and probiotic-based yogurt continues to accelerate as individuals seek functional food options that align with wellness-focused lifestyles. Producers are actively enhancing product formulations by incorporating additional nutritional components to meet evolving dietary expectations. At the same time, rapid urban expansion and fast-paced routines are fueling demand for convenient consumption formats that fit into busy schedules. Retail channels remain dominant due to strong physical store networks, while digital platforms are expanding rapidly as consumers increasingly shift toward online purchasing. From a regional perspective, Asia Pacific is emerging as a high-growth market supported by economic development and changing consumption habits, while North America and Europe demonstrate maturity with strong demand for premium offerings. Other regions are gradually gaining traction despite structural challenges, creating new avenues for long-term expansion within the yogurt market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $144.3 Billion |

| Forecast Value | $245 Billion |

| CAGR | 5.4% |

The flavoured yogurt segment accounted for 73.7% share in 2025 and is projected to grow at a CAGR of 5.6% from 2026 to 2035. This segment continues to perform strongly due to its wide appeal and continuous innovation in taste profiles. In contrast, unflavored yogurt maintains steady demand among consumers seeking simple and versatile options that align with health-conscious consumption and broader culinary usage.

The tubs segment generated USD 69.5 billion in 2025 and is forecast to reach USD 104 billion by 2035, registering a CAGR of 4.1%. This format remains the most widely adopted due to its practicality for larger consumption needs and cost-effective purchasing. Alternative packaging formats are also gaining traction as convenience and portability become increasingly important factors influencing buying decisions.

North America Yogurt Market is expected to grow at a CAGR of 3.6% during 2026 to 2035. The region reflects a well-established yet evolving landscape where consumer preferences emphasize nutritional value, product transparency, and premium quality. Demand continues to shift toward high-protein and functionally enhanced products, while innovation remains a central competitive factor. Expanding retail availability and a steady introduction of new product variations are reinforcing market growth, with increasing attention also being given to plant-based alternatives.

Key players in the Yogurt Market include Nestle S.A., Danone S.A., General Mills, Lactalis, China Mengniu, FrieslandCampina, Inner Mongolia Yili, Chobani, LLC, Meiji Holdings, and FAGE International. Companies operating in the Yogurt Market are implementing a range of strategies to strengthen their competitive position and expand their market share. A major focus is placed on continuous product innovation, particularly in developing functional and nutrient-enriched offerings that align with evolving consumer preferences. Businesses are investing in advanced manufacturing technologies to improve efficiency and maintain consistent product quality. Strategic partnerships and supply chain optimization are being prioritized to ensure reliable sourcing and cost control. Expansion into high-growth regions is another key approach, supported by localized product development to suit regional tastes. In addition, companies are enhancing their branding and digital presence to engage consumers more effectively, while mergers and acquisitions are being used to access new markets, technologies, and distribution networks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Flavor Type

- 2.2.4 Packaging Type

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer demand for probiotic-rich and gut health functional yogurt products

- 3.2.1.2 Increasing preference for convenient, ready-to-eat and drinkable yogurt formats globally

- 3.2.1.3 Expanding retail infrastructure and cold chain logistics improving product accessibility

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High perishability requiring continuous cold chain management increases operational costs

- 3.2.2.2 Growing competition from plant-based alternatives impacting traditional yogurt consumption trends

- 3.2.2.3 Volatility in raw milk prices affecting production costs and pricing stability

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for high-protein, low-fat, and functional yogurt innovations globally

- 3.2.3.2 Rapid expansion of online grocery platforms enabling broader consumer market reach

- 3.2.3.3 Increasing disposable incomes in emerging markets boosting dairy consumption demand

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Greek Yogurt

- 5.2.1 Full-Fat Greek Yogurt

- 5.2.2 Low-Fat Greek Yogurt

- 5.2.3 Fat-Free Greek Yogurt

- 5.3 Traditional/Stirred Yogurt

- 5.3.1 Full-Fat Traditional Yogurt

- 5.3.2 Low-Fat Traditional Yogurt

- 5.3.3 Fat-Free Traditional Yogurt

- 5.4 Set Yogurt

- 5.4.1 Fruit-on-Bottom Set Yogurt

- 5.4.2 Plain Set Yogurt

- 5.5 Yogurt Drinks

- 5.5.1 Dairy-Based Yogurt Drinks

- 5.5.2 Plant-Based Yogurt Drinks

- 5.6 Frozen Yogurt

- 5.6.1 Soft-Serve Frozen Yogurt

- 5.6.2 Packaged Frozen Yogurt

Chapter 6 Market Estimates and Forecast, By Flavor Type, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Unflavoured

- 6.2.1 Plain Traditional Yogurt

- 6.2.2 Plain Greek Yogurt

- 6.2.3 Plain Plant-Based Yogurt

- 6.3 Flavoured

- 6.3.1 Fruit Flavoured

- 6.3.2 Vanilla Flavoured

- 6.3.3 Chocolate Flavoured

- 6.3.4 Other Flavours

Chapter 7 Market Estimates and Forecast, By Packaging Type, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Tubs

- 7.2.1 Single-Serve Tubs

- 7.2.2 Family-Size Tubs

- 7.3 Pouches

- 7.3.1 Squeezable Pouches

- 7.3.2 Stand-Up Pouches

- 7.4 Cartons

- 7.4.1 Tetra Pack Cartons

- 7.4.2 Gable Top Cartons

- 7.5 Others

- 7.5.1 Bottles

- 7.5.2 Cups

- 7.5.3 Multi-Pack Formats

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Offline

- 8.2.1 Hypermarkets & Supermarkets

- 8.2.2 Specialty Stores

- 8.2.3 Convenience Stores

- 8.2.4 Others

- 8.3 Online

- 8.3.1 Brand Website

- 8.3.2 E-commerce Platform

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Danone S.A.

- 10.2 Lactalis

- 10.3 Nestle S.A.

- 10.4 China Mengniu

- 10.5 Inner Mongolia Yili

- 10.6 FrieslandCampina

- 10.7 Chobani, LLC

- 10.8 FAGE International

- 10.9 Meiji Holdings

- 10.10 General Mills