PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027670

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027670

Liquid Membrane Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

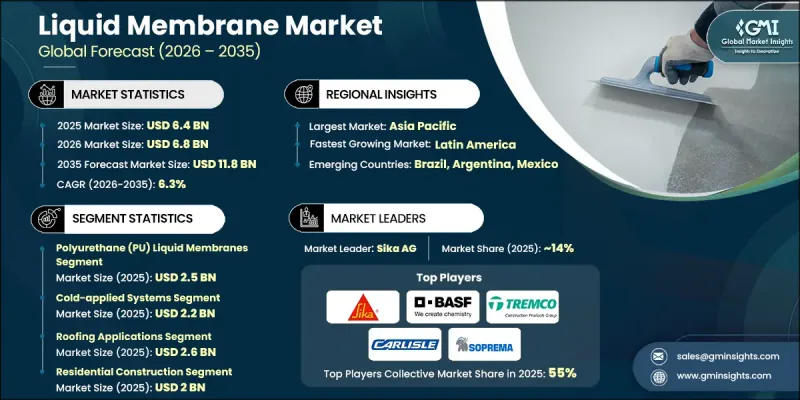

The Global Liquid Membrane Market was valued at USD 6.4 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 11.8 billion by 2035.

Growth in the market is driven by rising investments in infrastructure, increasing collaboration between public and private sectors, and evolving construction requirements across new developments and renovation projects. Demand is further supported by stricter building regulations focused on energy efficiency, moisture protection, and structural performance across residential, commercial, and industrial sectors. Liquid membranes are gaining traction in emerging economies due to their quick curing time, ease of application, and longer lifecycle compared to conventional alternatives. Rapid urbanization and the construction of modern structures are encouraging the use of advanced formulations such as polyurethane, acrylic, and cementitious materials. Acrylic-based membranes, known for their cost efficiency and lower environmental impact, are witnessing growing adoption in developed regions where sustainability certifications emphasize environmentally responsible materials. Additionally, water-based solutions are becoming increasingly relevant in renovation activities due to their compatibility with existing structures and compliance with updated standards.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.4 Billion |

| Forecast Value | $11.8 Billion |

| CAGR | 6.3% |

The polyurethane liquid membranes segment accounted for USD 2.5 billion in 2025. Product segmentation indicates a growing preference for high-performance materials, with polyurethane leading due to its flexibility, durability, and ability to withstand demanding environmental conditions. These characteristics make it a preferred choice for applications requiring long-term reliability and structural protection.

The residential construction segment was valued at USD 2 billion in 2025, maintaining its position as the leading end-use category in terms of volume. Continued growth in housing demand, urban development, and renovation activities is driving the adoption of liquid membranes. Their cost-effectiveness and ease of installation further enhance their appeal in residential applications.

North America Liquid Membrane Market generated USD 1.6 billion in 2025. The United States remains the dominant market in the region, supported by robust activity in residential upgrades, commercial construction, and large-scale infrastructure development. Regulatory initiatives and modernization programs continue to drive demand for advanced liquid membrane systems. Meanwhile, Canada is contributing to regional expansion through its increasing focus on sustainable construction practices and the adoption of environmentally efficient waterproofing materials.

Key companies operating in the Global Liquid Membrane Market include Sika AG, BASF SE, Tremco Incorporated, Carlisle Companies Inc., Soprema Group, GAF Materials Corporation, Johns Manville Corporation, Firestone Building Products, Dow Chemical Company, Huntsman Corporation, Pidilite Industries Limited, Fosroc International Limited, and MAPEI S.p.A. Companies in the Liquid Membrane Market are reinforcing their competitive position by prioritizing innovation, expanding product portfolios, and enhancing distribution networks. Many are investing in advanced formulations that improve durability, environmental performance, and ease of application to meet evolving construction standards. Strategic collaborations and partnerships are being used to strengthen market reach and improve access to large-scale infrastructure projects. Firms are also focusing on digital transformation to streamline supply chains and improve customer engagement.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 End user industry

- 2.2.5 Technology

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing construction industry demand

- 3.2.1.2 Infrastructure development and urbanization

- 3.2.1.3 Increasing focus on building durability

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Raw material price volatility

- 3.2.2.2 Technical application challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Sustainable and bio-based solutions

- 3.2.3.2 Smart membrane technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Patent Landscape

- 3.10 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.10.1 Major importing countries

- 3.10.2 Major exporting countries

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.12 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyurethane (PU) liquid membranes

- 5.2.1 Aromatic PU

- 5.2.2 Aliphatic PU

- 5.2.3 Bio-Based/Sustainable PU

- 5.3 Acrylic liquid membranes

- 5.3.1 Pure Acrylic

- 5.3.2 Styrene-Acrylic (Modified)

- 5.3.3 Silicone-Acrylic Hybrids

- 5.4 Cementitious liquid membranes

- 5.4.1 Flexible Cementitious

- 5.4.2 Rigid Cementitious

- 5.4.3 Polymer-Modified Cementitious

- 5.4.4 Crystalline Waterproofing Systems

- 5.5 Hybrid and specialty membranes

- 5.5.1 Polyurea systems

- 5.5.2 Silicone-based membranes

- 5.5.3 Bitumen-modified systems

- 5.5.4 Other specialty formulations

Chapter 6 Market Estimates and Forecast, By Application Method, 2022 - 2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cold-applied systems

- 6.3 Hot-applied systems

- 6.4 Spray-applied systems

- 6.4.1 Airless spray

- 6.4.2 Plural component spray

- 6.5 Brush/roller-applied systems

- 6.6 Other methods

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Roofing applications

- 7.2.1 Flat roof waterproofing

- 7.2.2 Pitched roof applications

- 7.2.3 Green roof systems

- 7.2.4 Roof renovation and repair

- 7.3 Below-grade waterproofing

- 7.3.1 Basement waterproofing

- 7.3.2 Foundation waterproofing

- 7.3.3 Underground structures

- 7.3.4 Tunnel waterproofing

- 7.4 Above-grade applications

- 7.4.1 Balcony and terrace waterproofing

- 7.4.2 Bathroom and wet area waterproofing

- 7.4.3 Facade and wall protection

- 7.4.4 Swimming pool waterproofing

- 7.5 Infrastructure applications

- 7.5.1 Bridge deck waterproofing

- 7.5.2 Parking deck applications

- 7.5.3 Water treatment facilities

- 7.5.4 Industrial floor coatings

- 7.6 Specialty applications

- 7.6.1 Marine and offshore structures

- 7.6.2 Transportation infrastructure

- 7.6.3 Agricultural applications

- 7.6.4 Mining and heavy industry

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Residential construction

- 8.2.1 New residential construction

- 8.2.2 Residential renovation and repair

- 8.2.3 Multi-family housing

- 8.2.4 Single-family housing

- 8.3 Commercial Construction

- 8.3.1 Office buildings

- 8.3.2 Retail and shopping centers

- 8.3.3 Hospitality and entertainment

- 8.3.4 Healthcare facilities

- 8.4 Industrial Construction

- 8.4.1 Manufacturing facilities

- 8.4.2 Warehouses and distribution centers

- 8.4.3 Chemical and process industries

- 8.4.4 Food and beverage facilities

- 8.5 Infrastructure and Public Works

- 8.5.1 Transportation infrastructure

- 8.5.2 Water and wastewater treatment

- 8.5.3 Energy and power generation

- 8.5.4 Government and public buildings

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Sika AG

- 10.2 BASF SE

- 10.3 Tremco Incorporated

- 10.4 Carlisle Companies Inc.

- 10.5 Soprema Group

- 10.6 GAF Materials Corporation

- 10.7 Johns Manville Corporation

- 10.8 Firestone Building Products

- 10.9 Dow Chemical Company

- 10.10 Huntsman Corporation

- 10.11 Pidilite Industries Limited

- 10.12 Fosroc International Limited

- 10.13 MAPEI S.p.A.