PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038269

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038269

Asia Pacific Small Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

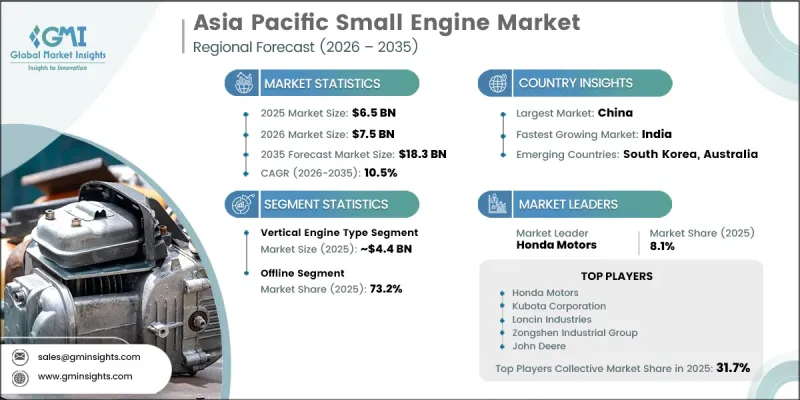

Asia Pacific Small Engine Market was valued at USD 6.5 billion in 2025 and is projected to grow at a CAGR of 10.5% to reach USD 18.3 billion by 2035.

Growth in the Asia Pacific small engine industry is being driven by rising construction activity supported by rapid urbanization across Southeast Asia and India. Expanding residential and commercial infrastructure is increasing demand for equipment used in landscaping, maintenance, and outdoor applications. At the same time, the transition toward mechanized agriculture is replacing manual labor with engine-powered solutions, improving productivity and operational efficiency. Government investments in large-scale infrastructure projects, including transport networks and smart city developments, are further boosting demand for compact machinery powered by small engines. In addition, rising disposable incomes across the middle class are encouraging greater spending on home improvement and outdoor equipment, further strengthening long-term market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.5 Billion |

| Forecast Value | $18.3 Billion |

| CAGR | 10.5% |

The Asia Pacific small engine market is also benefiting from the growing adoption of mechanized farming practices across developing economies. Farmers are increasingly relying on compact, engine-powered tools to enhance yield efficiency and reduce labor dependency. Rising infrastructure development activities are also supporting demand for portable machinery used in construction and maintenance projects, reinforcing consistent market expansion across multiple end-use sectors.

The vertical engine segment generated USD 4.4 billion in 2025 and is projected to reach USD 12.7 billion by 2035. This segment remains dominant due to its widespread use in walk-behind mowing equipment. Its compact design, efficient performance, and simpler lubrication systems make it highly suitable for high-density urban environments where space efficiency and reliability are essential.

The offline distribution channel accounted for 73.2% share in 2025. This dominance is driven by customer preference for physical evaluation of equipment before purchase. Buyers often rely on in-person assessment to evaluate build quality, performance, and durability. The availability of after-sales support, including maintenance, technical assistance, and servicing, further strengthens the preference for offline channels in this market.

China Small Engine Market held a 57.9% share in 2025. Growth in China is supported by its strong manufacturing base for agricultural machinery, generators, motorcycles, and outdoor equipment. High domestic consumption, along with strong export-oriented production, continues to drive demand. The country's efficient supply chain structure, rapid industrialization, and increasing adoption of mechanized farming and infrastructure development projects are further supporting sustained market expansion.

Key companies operating in the Asia Pacific Small Engine Market include Honda Motors, Kubota Corporation, Yamaha Motors, Briggs & Stratton, Yanmar Holdings, Kawasaki Heavy Industries, John Deere, Loncin Industries, Zongshen Industrial Group, Changchai Company, Greaves Cotton Limited, Rato Technology, Rehlko, Launtop, and Ducar / Dajiang Power. Companies in the Asia Pacific Small Engine Market are focusing on product innovation, manufacturing efficiency, and regional expansion to strengthen their market position. They are investing in advanced engine technologies that improve fuel efficiency, durability, and performance across various applications. Strategic partnerships with OEMs and distributors are helping expand market reach and improve supply chain integration. Many players are also enhancing localized production capabilities to reduce costs and meet regional demand more effectively.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.3.1 Source consistency protocol

- 1.4 Research Trail & Confidence Scoring

- 1.4.1 Research Trail Components

- 1.4.2 Scoring Components

- 1.5 Data Collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.7 Paid sources

- 1.7.1 Sources, by region

- 1.8 Base estimates and calculations

- 1.8.1 Base year calculation for any one approach

- 1.9 Forecast model

- 1.9.1 Quantified market impact analysis

- 1.9.1.1 Mathematical impact of growth parameters on forecast

- 1.9.1 Quantified market impact analysis

- 1.10 Research transparency addendum

- 1.10.1 Source attribution framework

- 1.10.2 Quality assurance metrics

- 1.10.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Engine

- 2.2.2 Energy Resources

- 2.2.3 Engine Displacement

- 2.2.4 Application

- 2.2.5 End Use

- 2.2.6 Distribution Channel

- 2.2.7 Country

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Outdoor power equipment demand

- 3.2.1.2 Growth in construction and infrastructure development

- 3.2.1.3 Growth in agriculture and gardening

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Inefficient supply chain

- 3.2.2.2 Lack of marketing and branding of small engine

- 3.2.3 Opportunities

- 3.2.3.1 Electrification and hybrid engine adoption

- 3.2.3.2 Expansion in rural infrastructure and emerging economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory framework

- 3.5 Major market trends and disruptions

- 3.6 Pricing Analysis (driven by primary research)

- 3.6.1 Historical price trend analysis (driven by primary research)

- 3.6.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.7 Future market trends

- 3.8 Trade data analysis (driven by paid database) (HS Code: 8407, 8408)

- 3.8.1 Import/export volume & value trends (driven by primary research)

- 3.8.2 Key trade corridors & tariff impact (driven by primary research)

- 3.9 Impact of AI & Generative AI on the Market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 Gen-AI use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Capacity & production landscape (driven by primary research)

- 3.12.1 Installed capacity by region & key producer (driven by primary research)

- 3.12.2 Capacity utilization rates & expansion pipelines (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By country

- 4.2.1.1 China

- 4.2.1.2 India

- 4.2.1.3 Japan

- 4.2.1.4 Australia

- 4.2.1.5 South Korea

- 4.2.1 By country

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Engine Type 2022 - 2035, (USD Billion; Million Units)

- 5.1 Vertical

- 5.2 Horizontal

Chapter 6 Market Size and Forecast, By Energy Resource 2022 - 2035, (USD Billion; Million Units)

- 6.1 Gasoline

- 6.2 Diesel

- 6.3 Gas

- 6.4 Electric

Chapter 7 Market Size and Forecast, By Engine Displacement 2022 - 2035, (USD Billion; Million Units)

- 7.1 Upto 100CC

- 7.2 100 CC to 250CC

- 7.3 250 CC to 550 CC

Chapter 8 Market Size and Forecast, By Application 2022 - 2035, (USD Billion; Million Units)

- 8.1 Lawn Mower

- 8.2 Snow Blower

- 8.3 Garden Tiller

- 8.4 Chain Saw

- 8.5 Go Kart

- 8.6 Pressure Washer

- 8.7 Water Pump

- 8.8 Others (Weed Trimmer etc.)

Chapter 9 Market Size and Forecast, By Distribution Channel 2022 - 2035, (USD Billion; Million Units)

- 9.1 Residential

- 9.2 Industrial

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion; Million Units)

- 10.1 Key trends

- 10.2 Online

- 10.3 Offline

- 10.3.1 Direct Sales

- 10.3.2 Indirect Sales

Chapter 11 Market Estimates & Forecast, By Country, 2022 - 2035, (USD Billion; Million Units)

- 11.1 Key trends

- 11.2 China

- 11.3 India

- 11.4 Japan

- 11.5 South Korea

- 11.6 Australia

- 11.7 Rest of Asia Pacific

Chapter 12 Company Profiles

- 12.1 Briggs & Stratton

- 12.2 Changchai Company

- 12.3 Ducar / Dajiang Power

- 12.4 Greaves Cotton Limited

- 12.5 Honda Motors

- 12.6 John Deere

- 12.7 Kawasaki Heavy Industries

- 12.8 Kubota Corporation

- 12.9 Launtop

- 12.10 Loncin Industries

- 12.11 Rato Technology

- 12.12 Rehlko

- 12.13 Yamaha Motors

- 12.14 Yanmar Holdings

- 12.15 Zongshen Industrial Group