PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038277

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038277

Aircraft Survival Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

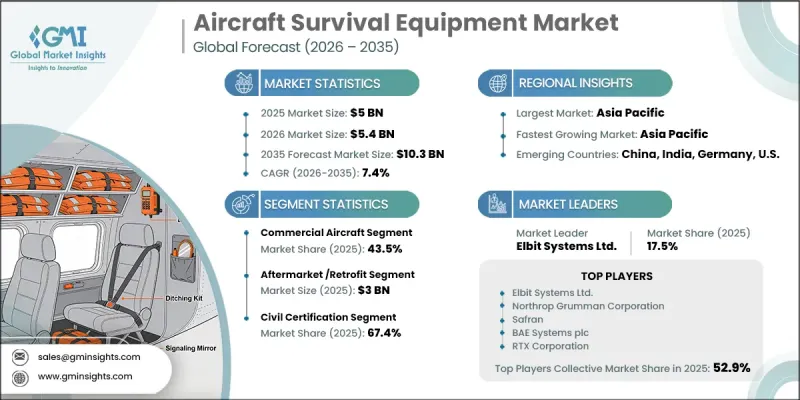

The Global Aircraft Survival Equipment Market was valued at USD 5 billion in 2025 and is estimated to grow at a CAGR of 7.4% to USD 10.3 billion by 2035.

Market growth is driven by the steady increase in aircraft deliveries across both commercial and defense aviation sectors, alongside strict regulatory requirements mandating the installation and maintenance of certified onboard safety systems. Rising global defense spending and continuous fleet modernization programs are further strengthening demand for advanced survival equipment. In addition, the development of lightweight, compact, and technologically advanced survival systems is encouraging both new installations and retrofit activities. The expansion of long-distance, overwater, and remote flight operations is also increasing the need for enhanced onboard safety solutions. Airlines and defense operators are placing greater emphasis on improving passenger and crew safety, which is contributing to sustained investment in survival equipment. As aviation authorities continue to enforce stringent compliance standards, the market is expected to witness growth supported by technological innovation, regulatory alignment, and increasing operational complexity across global aviation networks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5 Billion |

| Forecast Value | $10.3 Billion |

| CAGR | 7.4% |

The aircraft survival equipment market is further supported by the rising volume of aircraft entering service, driven by continued expansion in global aviation fleets. Increasing passenger traffic and fleet utilization are reinforcing the need for reliable emergency preparedness systems onboard aircraft. Regulatory bodies require strict adherence to safety certifications and periodic replacement of survival equipment to ensure operational readiness. Compliance with established technical standards governing onboard safety systems remains a critical factor shaping market demand. These regulations ensure that aircraft are equipped with certified systems designed to enhance survivability in emergency scenarios, thereby sustaining consistent demand for high-quality survival equipment across aviation sectors.

The civil aviation segment is expected to grow at a CAGR of 7.8% through 2035, supported by increasing demand for air travel and the expansion of regional connectivity. Growing use of smaller aircraft and business aviation platforms is further contributing to segment growth. Operators are increasingly investing in advanced survival equipment that offers improved performance, reduced weight, and enhanced reliability. The integration of modern technologies into safety systems is enabling greater operational flexibility and efficiency, encouraging faster adoption within this segment. These factors collectively position civil aviation as a key growth area within the overall market.

The aftermarket and retrofit segment reached USD 3 billion in 2025, driven by mandatory replacement cycles and the presence of a large installed base of aging aircraft across commercial and defense fleets. Regular maintenance, inspection, and recertification requirements are sustaining steady demand for replacement equipment. High utilization rates of aircraft further increase wear and tear on safety systems, necessitating timely upgrades and replacements. This ongoing need for compliance and operational readiness continues to reinforce the importance of the aftermarket segment in the overall industry landscape.

North America Aircraft Survival Equipment Market accounted for 34.2% share in 2025, supported by a well-established aviation ecosystem and a large fleet of active commercial and military aircraft. The region benefits from the presence of leading aircraft manufacturers, airlines, and defense organizations, all of which contribute to continuous demand for certified survival equipment. Strong regulatory oversight and ongoing defense aviation initiatives further strengthen market growth. Additionally, consistent investments in fleet modernization and safety enhancements support sustained demand for both new installations and replacement equipment across the region.

Key companies operating in the Aircraft Survival Equipment Market include THALES, Safran, RTX Corporation, Northrop Grumman Corporation, BAE Systems plc, Elbit Systems Ltd., Saab AB, RUAG Ltd., Airborne Systems Ltd., Survitec Group Limited, FCAH Aerospace, Legend Aerospace, and TULMAR Safety Systems. These players are actively engaged in developing advanced safety solutions and expanding their global presence through innovation and strategic initiatives. Companies in the Aircraft Survival Equipment Market are focusing on a range of strategic initiatives to strengthen their market position and enhance competitiveness. A major priority is the development of lightweight, durable, and technologically advanced survival systems that improve efficiency without compromising safety. Firms are investing in research and development to integrate smart features such as real-time monitoring and enhanced deployment mechanisms. Strategic partnerships with aircraft manufacturers, defense agencies, and airlines are helping companies secure long-term contracts and expand their customer base. Additionally, businesses are strengthening their aftermarket services by offering maintenance, repair, and overhaul solutions to ensure regulatory compliance and customer retention.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Equipment type (primary) trends

- 2.2.2 Aircraft type trends

- 2.2.3 Fit type trends

- 2.2.4 Certification standards trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global aircraft deliveries and fleet expansion

- 3.2.1.2 Stringent aviation safety regulations and compliance mandates

- 3.2.1.3 Increasing defense & military aviation spending

- 3.2.1.4 Technological advancements in smart and lightweight survival equipment

- 3.2.1.5 Expansion of overwater, remote, and long-haul flight operations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of certified survival equipment and maintenance

- 3.2.2.2 Lengthy certification and approval timelines

- 3.2.3 Market opportunities

- 3.2.3.1 Rising modernization and replacement programs for aging aircraft fleets

- 3.2.3.2 Increasing demand for integrated and service-based survival equipment solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Equipment Type (Primary), 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Flotation & water survival equipment

- 5.3 Oxygen systems

- 5.4 Evacuation equipment

- 5.5 Fire suppression equipment

- 5.6 Survival kits & emergency supplies

- 5.7 Emergency communication & locator systems

- 5.8 Protective breathing equipment

Chapter 6 Market Estimates and Forecast, By Aircraft Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Commercial aircraft

- 6.3 Military aircraft

- 6.4 Civil aviation

Chapter 7 Market Estimates and Forecast, By Fit Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 OEM / line fit

- 7.3 Aftermarket / retrofit

Chapter 8 Market Estimates and Forecast, By Certification Standards, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Civil certification

- 8.3 Military certification

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Elbit Systems Ltd.

- 10.1.2 Northrop Grumman Corporation

- 10.1.3 Safran

- 10.1.4 BAE Systems plc

- 10.1.5 RTX Corporation

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Airborne Systems Ltd.

- 10.2.1.2 FCAH Aerospace

- 10.2.1.3 TULMAR Safety Systems

- 10.2.2 Asia Pacific

- 10.2.2.1 Legend Aerospace

- 10.2.3 Europe

- 10.2.3.1 RUAG Ltd.

- 10.2.3.2 THALES

- 10.2.3.3 Saab AB

- 10.2.3.4 Survitec Group Limited

- 10.2.1 North America