PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038285

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038285

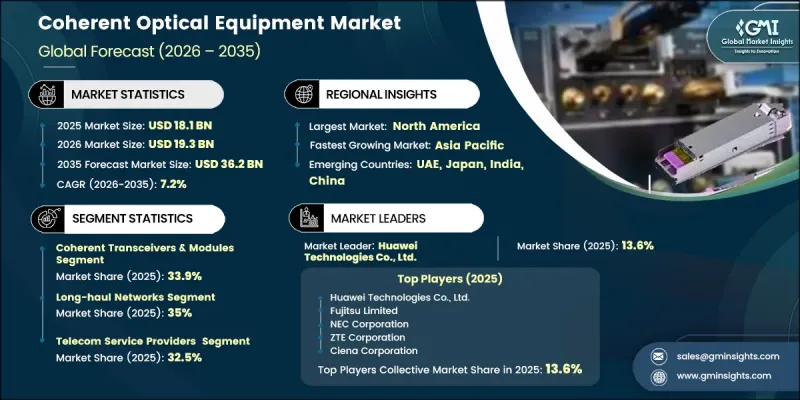

Coherent Optical Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Coherent Optical Equipment Market was valued at USD 18.1 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 36.2 billion by 2035.

The coherent optical equipment industry is expanding steadily as demand intensifies for high-capacity data transmission and efficient network performance. Rapid growth in cloud computing, widespread rollout of next-generation communication networks, and the continuous rise in global data center deployments are key factors driving this expansion. Increasing requirements for low-latency and high-speed connectivity are pushing network operators to adopt advanced optical communication technologies. Strong investments from both telecom operators and government bodies aimed at modernizing backbone infrastructure are further supporting market development. In addition, the shift toward open and flexible optical network architectures is transforming deployment strategies, enabling greater interoperability and reduced dependence on single vendors. The growing adoption of software-defined networking approaches enhances operational efficiency and scalability, positioning coherent optical technologies as a critical component in future-ready communication ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $18.1 Billion |

| Forecast Value | $36.2 Billion |

| CAGR | 7.2% |

The wavelength-division multiplexers segment is anticipated to grow at a CAGR of 7.7% through 2035, supported by rising demand for maximizing fiber capacity while improving overall network efficiency. This technology enables multiple data streams to be transmitted simultaneously through a single optical fiber, optimizing bandwidth utilization. Increased investments in optical infrastructure and the need to support large-scale data transmission across advanced communication networks are further accelerating segment growth.

The telecom service providers segment accounted for a share of 32.5% in 2025, driven by substantial investments in upgrading network infrastructure to handle increasing data traffic and expanding connectivity requirements. These providers rely on coherent optical technologies for long-distance and metro network applications, ensuring reliable and high-capacity communication performance. Continuous network modernization efforts and rising demand for faster connectivity are reinforcing the segment's leadership position.

North America Coherent Optical Equipment Market held a 31.1% share in 2025, supported by strong demand for high-bandwidth connectivity and ongoing upgrades to communication infrastructure. The region continues to witness significant investments in advanced optical technologies to support growing data traffic and evolving digital applications, contributing to sustained market growth.

Key players operating in the Global Coherent Optical Equipment Industry include Accelink Technologies, Adtran, Broadcom Inc., Ciena Corporation, Cisco Systems, Inc., Coherent Corp., Fujitsu Limited, Huawei Technologies Co., Ltd., Juniper Networks, Lumentum, Marvell Technology, Inc., NEC Corporation, NeoPhotonics Corporation, Nokia Corporation, Ribbon Communications Operating Company, Inc., ZHONGJI INNOLIGHT, and ZTE Corporation. Companies in the Coherent Optical Equipment Market are focusing on innovation, strategic alliances, and technology integration to strengthen their competitive position. They are investing in advanced optical technologies to enhance data transmission speed, capacity, and energy efficiency. Collaborations with telecom operators and cloud service providers are enabling faster deployment of next-generation network solutions. Firms are also expanding their product portfolios to support evolving network requirements and improve scalability. Additionally, companies are adopting open architecture approaches to improve interoperability and reduce vendor dependency.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Component trends

- 2.2.2 Technology trends

- 2.2.3 Application trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for high-capacity data center interconnect (DCI) networks

- 3.2.1.2 Rapid expansion of 5G and next-generation telecom infrastructure

- 3.2.1.3 Increasing adoption of cloud computing and hyperscale data centers

- 3.2.1.4 Growing AI/ML workloads driving high-speed optical transmission needs

- 3.2.1.5 Continuous advancements in coherent optical transceiver technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High deployment and system integration costs of coherent optical solutions

- 3.2.2.2 Technical complexity and power consumption limitations in advanced optical networks

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of pluggable coherent optical modules in data center interconnect

- 3.2.3.2 Growth in Open ROADM and disaggregated optical network architectures

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends (Based on paid Database)

- 3.8.1 Historical Price Analysis (2022-2025)

- 3.8.2 Price Trend Drivers

- 3.8.3 Regional Price Variations

- 3.8.4 Price Forecast (2026-2035)

- 3.9 Trade Data Analysis (Driven by Primary Research)

- 3.9.1 Import/Export Volume & Value Trends

- 3.9.2 Key Trade Corridors & Tariff Impact

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI-Driven Disruption of Existing Business Models

- 3.10.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.10.3 Risks, Limitations & Regulatory Considerations

- 3.11 Capacity & Production Landscape (Driven by Primary Research)

- 3.11.1 Installed Capacity by Region & Key Producer

- 3.11.2 Capacity Utilization Rates & Expansion Pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Component, 2022-2035 (USD Million)

- 5.1 Key trends

- 5.2 Coherent transceivers & modules

- 5.3 Wavelength-division Multiplexers (WDM)

- 5.4 Optical Amplifiers

- 5.5 Optical Switches

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2022-2035 (USD Million)

- 6.1 Key trends

- 6.2 100G

- 6.3 200G

- 6.4 400G+

- 6.5 400G ZR

- 6.6 800G

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million)

- 7.1 Key trends

- 7.2 Long-haul networks

- 7.3 Metro networks

- 7.4 Data Center Interconnect (DCI)

- 7.5 Submarine networks

Chapter 8 Market Estimates and Forecast, By End User, 2022-2035 (USD Million)

- 8.1 Key trends

- 8.2 Telecom service providers

- 8.3 Data center operators & cloud service providers

- 8.4 Enterprises

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Ciena Corporation

- 10.1.2 Huawei Technologies Co., Ltd.

- 10.1.3 Nokia Corporation

- 10.1.4 Cisco Systems, Inc.

- 10.1.5 ZTE Corporation

- 10.1.6 Fujitsu Limited

- 10.1.7 NEC Corporation

- 10.1.8 Juniper Networks

- 10.1.9 Broadcom Inc.

- 10.1.10 Marvell Technology, Inc.

- 10.2 Regional Players

- 10.2.1 Ribbon Communications Operating Company, Inc.

- 10.2.2 Adtran

- 10.2.3 Coherent Corp.

- 10.2.4 Lumentum

- 10.2.5 NeoPhotonics Corporation

- 10.3 Local Players

- 10.3.1 ZHONGJI INNOLIGHT

- 10.3.2 Accelink Technologies