PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038287

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038287

North America Wireless Earphone Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

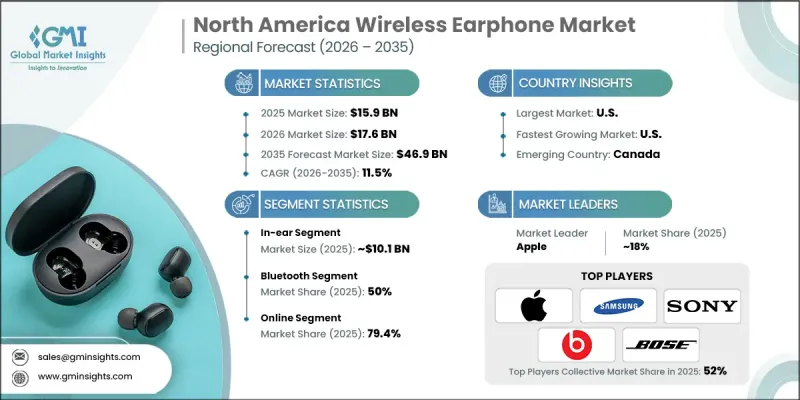

North America Wireless Earphone Market was valued at USD 15.9 billion in 2025 and is estimated to grow at a CAGR of 11.5% to reach USD 46.9 billion by 2035.

The market is gaining traction as consumers shift toward convenient, high-performance audio solutions that align with dynamic and mobile lifestyles. Increasing demand for cable-free devices has accelerated adoption, as users seek seamless audio experiences without the limitations associated with wired alternatives. Advancements in wireless technology have significantly enhanced sound quality, connectivity stability, and battery efficiency, making these devices more appealing across diverse user groups. Additionally, rising awareness on health and active living is influencing purchasing behavior, with consumers favoring lightweight and portable audio solutions that support daily routines. The growing reliance on smart devices and digital ecosystems is contributing to market expansion, positioning wireless earphones as an essential accessory for modern consumers seeking flexibility, comfort, and performance in their audio experiences.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $15.9 Billion |

| Forecast Value | $46.9 Billion |

| CAGR | 11.5% |

In-ear wireless earphones continue to gain widespread adoption due to their ergonomic design and adaptability across multiple usage scenarios. These devices are increasingly preferred for their ability to deliver comfort during extended usage while maintaining consistent audio quality. Demand is rising among professionals who require reliable audio solutions for communication, as well as among consumers seeking immersive sound experiences during daily activities. The evolution of compact audio technology has further improved usability, enabling seamless integration into everyday routines while supporting both productivity and entertainment needs. Shifting consumer preferences and evolving lifestyle patterns across North America are contributing to sustained demand for wireless earphones. Retail and digital sales channels are expanding their product offerings to cater to a broad spectrum of user requirements. Consumers are increasingly prioritizing devices that enable uninterrupted connectivity and enhance their overall digital experience.

The in-ear segment generated USD 10.1 billion in 2025 and is expected to grow at a CAGR of 11.5% from 2026 to 2035. This segment holds a dominant position due to its compact form factor and suitability for everyday use. Its versatility supports a wide range of applications, making it a preferred choice among consumers seeking convenience and portability. Continuous improvements in design and functionality are enhancing user experience, while maintaining high standards of comfort and sound performance. The segment continues to evolve in line with technological advancements, ensuring consistent market leadership.

The Bluetooth segment accounted for 50% share in 2025 and is projected to grow at a CAGR of 11.6% over the forecast period. This segment leads the market due to its broad compatibility with a wide range of digital devices. Wireless connectivity enables users to access audio content effortlessly without additional hardware or complex configurations. Technological advancements have improved connection stability, reduced latency, and enhanced energy efficiency. The ability to support multiple device connections and deliver a seamless user experience continues to drive adoption. Ease of use and universal acceptance across consumer electronics further reinforce the segment's strong position within the market.

United States Wireless Earphone Market reached USD 12.2 billion in 2025 and is anticipated to grow at a CAGR of 11.6% from 2026 to 2035. Market growth in the country is supported by a large and technologically engaged consumer base, along with widespread adoption of advanced digital devices. Consumers are increasingly investing in high-quality audio solutions that offer both convenience and superior performance. The availability of a diverse product range across multiple distribution channels ensures accessibility for a wide audience. Continuous innovation and strong consumer interest in advanced features are further supporting market expansion, positioning the country as a key contributor to regional growth.

Key players operating in the North America Wireless Earphone Market include Apple, Samsung, Sony, Bose, JBL, Anker, Xiaomi, OnePlus, OPPO, Realme, Nothing, Huawei, boAt (Imagine Marketing), Noise, and Beats. Companies in the North America Wireless Earphone Market are focusing on innovation, product differentiation, and strategic expansion to strengthen their competitive position. Market participants are investing in advanced audio technologies to enhance sound quality, battery performance, and connectivity features. Emphasis on design innovation and user comfort is helping brands attract a wider consumer base. Partnerships with distribution platforms and expansion into digital sales channels are improving product accessibility and market reach. Companies are also leveraging branding and targeted marketing strategies to build strong consumer engagement. Continuous investment in research and development, along with competitive pricing and feature integration, enables firms to maintain a strong foothold in an increasingly competitive and rapidly evolving market landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 By type

- 2.2.2 By connectivity

- 2.2.3 By battery life

- 2.2.4 By price

- 2.2.5 By application

- 2.2.6 By end user

- 2.2.7 By distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for wireless and portable audio solutions

- 3.2.1.2 Increasing adoption of active noise cancellation and premium features

- 3.2.1.3 Rising focus on fitness and mobile lifestyle

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Battery life limitations reduce usage satisfaction

- 3.2.2.2 Competition from budget alternatives with similar features

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of smart features and AI integration

- 3.2.3.2 Increasing adoption of multi-device connectivity

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis - North America (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis- North America (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium/Value/Cost-plus) (Driven by Primary Research)

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis- North America (Driven by Paid Database)

- 3.10.1 U.S. Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.2 Canada Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.3 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Distribution Infrastructure & Channel Penetration Landscape (Driven by Primary Research)

- 3.12.1 Channel Coverage by Region & Format (Modern vs. Traditional Retail) (Driven by Primary Research)

- 3.12.2 Last-Mile Infrastructure Gaps & Emerging Channel Shifts (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 U.S.

- 4.2.2 Canada

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022-2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 On-ear

- 5.3 In-ear

Chapter 6 Market Estimates & Forecast, By Connectivity, 2022-2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Bluetooth

- 6.3 Wi-Fi

- 6.4 NFC

Chapter 7 Market Estimates & Forecast, By Battery Life, 2022-2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Up to 12 hours

- 7.3 12 to 24 hours

- 7.4 Above 24 hours

Chapter 8 Market Estimates & Forecast, By Application, 2022-2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Music & entertainment

- 8.3 Gaming

- 8.4 Fitness & sports

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Price, 2022-2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Low

- 9.3 Medium

- 9.4 High

Chapter 10 Market Estimates & Forecast, By End User, 2022-2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Individual Consumers

- 10.3 Enterprise/Institutional

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Online

- 11.3 Offline

Chapter 12 Market Estimates and Forecast, By Country, 2022 - 2035 (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 U.S.

- 12.3 Canada

Chapter 13 Company Profiles

- 13.1 Anker

- 13.2 Apple

- 13.3 Beats

- 13.4 boAt (Imagine Marketing)

- 13.5 Bose

- 13.6 Huawei

- 13.7 JBL

- 13.8 Noise

- 13.9 Nothing

- 13.10 OnePlus

- 13.11 OPPO

- 13.12 Realme

- 13.13 Samsung

- 13.14 Sony

- 13.15 Xiaomi