PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038288

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038288

North America Plain Bearing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

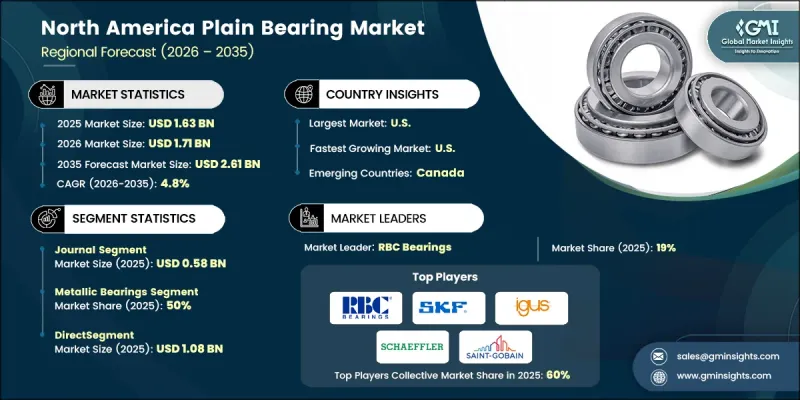

North America Plain Bearing Market was valued at USD 1.63 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 2.61 billion by 2035.

The region continues to rely heavily on a large installed base of aging industrial equipment that is routinely refurbished instead of replaced. This dynamic creates consistent demand for plain bearings, which are engineered to operate efficiently under demanding industrial conditions. Market growth is driven more by maintenance cycles, retrofitting activities, and efforts to extend equipment lifespan than by new machinery sales. Plain bearings remain essential components in heavy-duty operations due to their durability and ability to function reliably in harsh environments. The emphasis on refurbishment over replacement supports steady consumption patterns and reinforces long-term market stability. As industries prioritize operational continuity and cost control, plain bearings play a critical role in sustaining performance and ensuring equipment longevity across North America.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.63 Billion |

| Forecast Value | $2.61 Billion |

| CAGR | 4.8% |

Applications involving heavy equipment frequently operate under conditions of moderate speed and high load, where plain bearings offer advantages over alternative bearing types. These components deliver strong resistance to impact, accommodate misalignment, and maintain performance under stress. End users tend to prioritize reliability, ease of servicing, and predictable wear characteristics, which has led to a preference for well-established bearing designs. Metal and composite variants continue to gain traction as they align with the operational needs of industries focused on maximizing productivity while minimizing large-scale capital investments. As a result, plain bearings have become deeply embedded in industrial operations across the region, supporting consistent performance and cost efficiency.

The journal bearings segment generated USD 0.58 billion in 2025. This configuration is widely used to support rotating shafts subjected to radial loads while enabling smooth sliding motion. These bearings are particularly suitable for environments characterized by high load demands and moderate operating speeds. Their design allows stable performance through direct surface interaction or lubrication-assisted operation, making them a dependable choice for a wide range of mechanical systems requiring consistent motion and durability.

The metallic plain bearings segment accounted for 50% share in 2025, establishing them as the dominant material segment. These bearings are widely selected for their high load-bearing capacity, extended service life, and ability to withstand elevated temperatures. Manufactured using various material combinations, they can be tailored to meet specific operational requirements. Their cost-effectiveness and durability make them a preferred solution for applications involving sustained mechanical stress and long operating cycles, supporting their widespread adoption across multiple industrial environments.

U.S. Plain Bearing Market held 72.7% share in 2025, generating USD 1.19 billion. The country's market strength is supported by a broad base of industries that depend on long-lasting mechanical systems. Plain bearings are widely used to manage radial loads, absorb mechanical stress, and ensure smooth and predictable motion. Demand is largely driven by ongoing maintenance, repair, and equipment life-extension efforts rather than expansion through new capacity. This reliance on refurbishment cycles helps maintain steady demand and reinforces market resilience, even during periods of fluctuating capital investment.

Key participants in the North America Plain Bearing Industry include AST Bearings, Bowman Bearing Technologies, Bunting Bearings, Daido Metal USA, ELCEE Group, ElringKlinger AG, GGB Bearing Technology, igus GmbH, Isostatic Industries, JTEKT North America (Koyo), NSK, NTN, Oiles America, RBC Bearings, Saint-Gobain Bearings, Schaeffler Group, SKF Group, THK, Timken Aurora Bearing, Timken Company, and ZOLLERN GmbH & Co. KG. Companies operating in the North America Plain Bearing Market are focusing on strengthening their competitive position through product innovation, operational efficiency, and strategic collaborations. Manufacturers are investing in advanced materials and engineering techniques to enhance durability, reduce wear, and improve performance under demanding conditions. Many players are expanding their product portfolios to address diverse application requirements while also improving customization capabilities. Partnerships with distributors and end users are helping companies broaden market reach and strengthen customer relationships. In addition, firms are optimizing supply chains and production processes to reduce costs and improve delivery timelines.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Type

- 2.2.3 Material

- 2.2.4 End use industry

- 2.2.5 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Strong installed base of heavy industry & machinery

- 3.2.1.2 Aerospace & defense reliability requirements

- 3.2.1.3 Shift toward low-maintenance & sealed systems

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Competitive pressure from rolling bearings

- 3.2.2.2 Raw material & input cost sensitivity

- 3.2.3 Opportunities

- 3.2.3.1 Self-lubricating & composite bearing expansion

- 3.2.3.2 Digital monitoring & smart maintenance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Pricing analysis, 2025 (driven by primary research)

- 3.7.1 Historical price trend analysis

- 3.7.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.7.3 Impact of raw material volatility on pricing

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Consumer behavior analysis

- 3.10.1 Purchasing patterns

- 3.10.2 Preference analysis

- 3.10.3 Regional variations in consumer behavior

- 3.10.4 Impact of e-commerce on buying decisions

- 3.11 Trade data analysis (driven by paid data base) (HS Code 8483.30)

- 3.11.1 Import/export volume & value trends

- 3.11.2 Key trade corridors & tariff impact analysis

- 3.11.3 North America trade flows

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.2.1 Predictive maintenance & bearing life optimization

- 3.12.2.2 Design optimization & material selection

- 3.12.2.3 Supply chain forecasting & demand planning

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (driven by primary research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By country

- 4.2.1.1 U.S.

- 4.2.1.2 Canada

- 4.2.1 By country

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Angular contact

- 5.3 Journal

- 5.4 Linear

- 5.5 Thrust

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Metallic bearings

- 6.3 Polymer bearings

- 6.4 Composite bearings

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Automotive & transportation

- 7.3 Industrial machinery

- 7.4 Aerospace & defense

- 7.5 Energy & power

- 7.6 Construction machinery

- 7.7 Agriculture equipment

- 7.8 Mining & drilling

- 7.9 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 U.S.

- 9.3 Canada

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 SKF Group

- 10.1.2 Schaeffler Group

- 10.1.3 Timken Company

- 10.1.4 NSK

- 10.1.5 NTN Corporation

- 10.1.6 GGB Bearing Technology

- 10.1.7 Saint-Gobain Bearings

- 10.2 Regional players

- 10.2.1 RBC Bearings

- 10.2.2 igus GmbH

- 10.2.3 ElringKlinger AG

- 10.2.4 JTEKT North America (Koyo)

- 10.2.5 Oiles America

- 10.2.6 Daido Metal USA

- 10.2.7 THK

- 10.3 Emerging players

- 10.3.1 ZOLLERN GmbH & Co. KG

- 10.3.2 Bunting Bearings LLC

- 10.3.3 Bowman Bearing Technologies

- 10.3.4 Timken Aurora Bearing

- 10.3.5 Isostatic Industries

- 10.3.6 AST Bearings LLC

- 10.3.7 ELCEE Group