PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038290

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038290

North America Cordless Garden Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

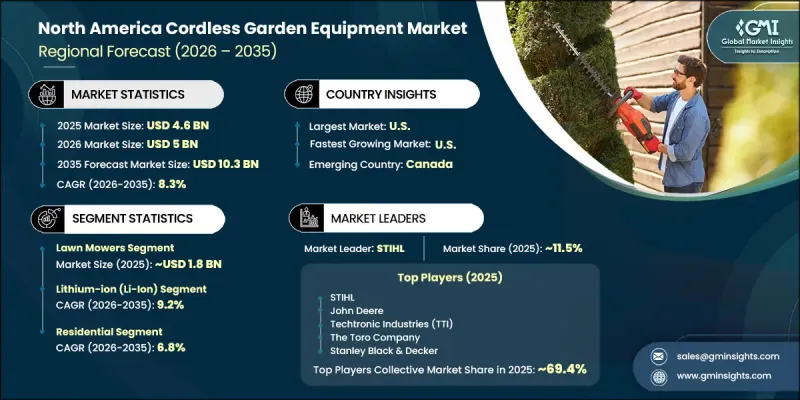

North America Cordless Garden Equipment Market was valued at USD 4.6 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 10.3 billion by 2035.

Growth is driven by increased homeowner investment in lawn care and garden enhancement activities across the region. Consumers are prioritizing convenience, portability, and reduced noise when selecting equipment, which is accelerating the shift toward cordless solutions. Ongoing usage throughout different seasonal cycles continues to sustain demand, while accessibility through both retail outlets and digital platforms supports consistent product availability. Advancements in lithium-ion battery technology are playing a critical role in shaping market dynamics, with improvements in charging speed, lifespan, and efficiency enhancing product performance. These batteries deliver reliable and consistent power, allowing cordless tools to match the effectiveness of traditional fuel-based alternatives, further strengthening their adoption across residential and professional applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.6 Billion |

| Forecast Value | $10.3 Billion |

| CAGR | 8.3% |

The lawn mowers segment generated USD 1.8 billion in 2025 and is forecast to grow at a CAGR of 9% between 2026 and 2035. This segment maintains its leading position due to its fundamental importance in routine lawn care. Cordless variants provide superior maneuverability, quieter operation, and simplified handling compared to conventional options. Continuous enhancements in motor performance and battery endurance have improved cutting efficiency and extended runtime, making them suitable for a wide range of lawn sizes. Growing consumer preference for user-friendly and low-maintenance equipment continues to reinforce demand within this category.

The lithium-ion (Li-Ion) battery segment accounted for 72.6% share in 2025 and is expected to grow at a CAGR of 9.2% through 2035. This segment leads due to its superior energy performance, lightweight structure, and extended lifecycle compared to other battery technologies. Lithium-ion batteries enable faster recharging, consistent power delivery, and minimal upkeep, making them highly effective for cordless equipment. Their ability to sustain performance without power fluctuations enhances overall efficiency and user experience. Continued technological progress and declining production costs are further accelerating adoption, reinforcing the segment's dominance.

U.S. Cordless Garden Equipment Market captured USD 4.1 billion in 2025 and is anticipated to grow at a CAGR of 8.3% from 2026 to 2035. Demand is strongly supported by residential property trends, where outdoor maintenance remains a priority. Consumers show a strong preference for battery-powered tools that offer quieter operation and ease of handling. Key purchasing considerations include battery longevity, charging efficiency, and compatibility across multiple devices. Distribution channels are well established, with strong presence across physical retail networks and online platforms. Demand from professional service providers also contributes to market expansion, particularly for equipment designed for prolonged use. Seasonal patterns continue to influence purchasing behavior, with heightened activity during peak landscaping periods.

Key players operating in the North America Cordless Garden Equipment Market include AriensCo, Bosch, EGO Power+, Exmark Manufacturing, Greenworks, Honda Power Equipment, Husqvarna, John Deere, Makita, Mean Green (Generac), Scag Power Equipment, Stanley Black & Decker, STIHL Inc., Techtronic Industries (TTI), and The Toro Company. Companies in the North America Cordless Garden Equipment Market are strengthening their market position through continuous product innovation, particularly in battery technology and motor efficiency. They are focusing on expanding lithium-ion platforms that support multiple tools within a single battery system to improve user convenience and brand loyalty. Strategic partnerships and acquisitions are being pursued to enhance product portfolios and technological capabilities. Firms are also investing in expanding their distribution networks across both offline retail and e-commerce channels to increase accessibility. Emphasis on sustainability, including reduced emissions and noise levels, is shaping product development strategies. Additionally, companies are targeting professional users with high-performance equipment while maintaining affordability and ease of use for residential consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Product type

- 2.2.3 Battery type

- 2.2.4 Price

- 2.2.5 End use

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of battery-powered and eco-friendly garden tools

- 3.2.1.2 Growing popularity of home gardening and landscaping activities

- 3.2.1.3 Expansion of residential landscaping and property maintenance services

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 Higher upfront cost compared to corded or gas-powered equipment

- 3.2.2.2 Limited battery life and charging requirements

- 3.2.3 Opportunities

- 3.2.3.1 Integration of smart and IoT-enabled garden equipment

- 3.2.3.2 Rising trend of sustainable and noise-free outdoor tools in urban areas

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.9.3 Price comparison: battery vs gas-powered equipment

- 3.9.4 Impact of battery cost on overall equipment pricing

- 3.9.5 Regional price variations & drivers

- 3.10 Trade data analysis (HS Code- 8467.21) (driven by paid database)

- 3.10.1 Import/export volume & value trends (driven by paid data base)

- 3.10.2 Key trade corridors & tariff impact (driven by paid data base)

- 3.10.3 Major exporting & importing countries

- 3.10.4 Trade policy impact on market dynamics

- 3.11 Capacity & production landscape (driven by primary research)

- 3.11.1 Installed capacity by region & key producer (driven by primary research)

- 3.11.2 Capacity utilization rates & expansion pipelines (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Lawn mowers

- 5.3 Chainsaws

- 5.4 Hedge trimmers

- 5.5 Leaf blowers

- 5.6 Grass trimmers

- 5.7 Other tools

Chapter 6 Market Estimates & Forecast, By Battery Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Lithium-Ion (Li-Ion)

- 6.3 Nickel-Cadmium (NiCd)

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Price, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Online

- 9.3 Offline

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 AriensCo

- 11.2 Bosch

- 11.3 EGO Power+

- 11.4 Exmark Manufacturing

- 11.5 Greenworks

- 11.6 Honda Power Equipment

- 11.7 Husqvarna

- 11.8 John Deere

- 11.9 Makita

- 11.10 Mean Green (Generac)

- 11.11 Scag Power Equipment

- 11.12 Stanley Black & Decker

- 11.13 STIHL Inc.

- 11.14 Techtronic Industries (TTI)

- 11.15 The Toro Company