PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038352

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038352

Data Center Refrigerant Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

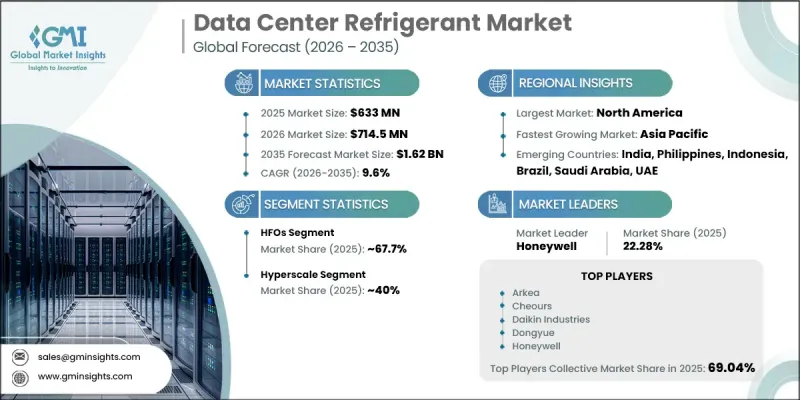

The Global Data Center Refrigerant Market was valued at USD 633 million in 2025 and is estimated to grow at a CAGR of 9.6% to reach USD 1.62 billion by 2035.

The market is undergoing a major transformation driven by the rapid expansion of digital infrastructure, including hyperscale facilities, cloud platforms, and accelerating global data consumption. Increasing computational workloads from artificial intelligence, big data analytics, and high-density computing environments are significantly raising thermal management requirements across modern data centers. As a result, demand for advanced refrigerants that ensure efficient heat control, operational stability, and optimized energy performance is increasing steadily.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $633 Million |

| Forecast Value | $1.62 Billion |

| CAGR | 9.6% |

The industry is also experiencing a structural shift away from traditional high-global-warming-potential refrigerants toward low-emission and energy-efficient alternatives. Regulatory pressure from global climate agreements and regional environmental policies is accelerating the adoption of next-generation refrigerants. Operators are increasingly focusing on reducing emissions, improving leakage control, and enhancing lifecycle management practices to comply with evolving sustainability requirements. This transition is further reinforced by rising emphasis on lowering operating costs and improving energy efficiency across large-scale digital infrastructure.

The HFOs segment held a 67.7% share in 2025 and is projected to grow at a CAGR of 10.2% through 2035. HFO refrigerants continue to dominate due to tightening environmental regulations and the global push toward decarbonization. Their significantly lower global warming potential, combined with strong cooling efficiency, makes them a preferred solution for next-generation data center cooling systems. The ongoing phase-out of high-GWP refrigerants is further accelerating their adoption across the industry.

The hyperscale segment accounted for 40% share in 2025 and is expected to grow at a CAGR of 10.4% from 2026 to 2035. This segment leads the market due to extremely high computing densities and large-scale infrastructure operated by major cloud and technology providers. These facilities generate substantial heat loads from artificial intelligence workloads, cloud computing, and advanced digital services, requiring highly efficient refrigerant-based cooling systems to maintain continuous operations and system stability.

U.S. Data Center Refrigerant Market held a 79% share in 2025, generating USD 176.3 million. Growth in the country is strongly supported by rapid hyperscale data center expansion driven by artificial intelligence, cloud computing, and data-intensive applications. Continuous investments in new facilities by leading technology firms are increasing demand for advanced cooling systems. Rising adoption of high-density server infrastructure is further intensifying thermal loads, strengthening the need for high-performance refrigerants. In addition, strict energy efficiency regulations and sustainability mandates are encouraging the shift toward low-GWP refrigerant solutions and modern thermal management technologies.

Key companies operating in the Global Data Center Refrigerant Market include Daikin Industries, Linde plc, Honeywell, Chemours, AGC, Dongyue, Zhejiang Juhua, Arkea and Sinochem. Companies in the Data Center Refrigerant Market are actively focusing on developing low-global warming potential refrigerants that align with tightening environmental regulations and sustainability targets. A major strategy involves increasing investment in research and development to enhance refrigerant efficiency, thermal stability, and compatibility with high-density computing environments. Market players are also strengthening partnerships with data center operators and cooling system manufacturers to integrate advanced refrigerant solutions into next-generation infrastructure. Expansion of production capabilities in high-demand regions is being prioritized to ensure supply chain stability and faster delivery. Additionally, firms are emphasizing compliance-driven innovation, improving leakage detection systems, and enhancing lifecycle management solutions.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast Model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Refrigerant

- 2.2.3 Data Center

- 2.2.4 Cooling

- 2.2.5 Application

- 2.2.6 End-Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in hyperscale and cloud data center expansion

- 3.2.1.2 Surge in AI, machine learning, and high-performance computing workloads

- 3.2.1.3 Increase in adoption of energy-efficient and sustainable cooling solutions

- 3.2.1.4 Rise in regulatory push for low-GWP refrigerants

- 3.2.1.5 Surge in colocation and edge data center deployments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial costs of new systems

- 3.2.2.2 Complex integration with existing infrastructure

- 3.2.3 Market opportunities

- 3.2.3.1 Rise in demand for HFO-based and natural refrigerants

- 3.2.3.2 Surge in adoption of liquid and hybrid cooling technologies

- 3.2.3.3 Increase in sustainability and carbon reduction initiatives by operators

- 3.2.3.4 Rise in retrofitting and upgrading of legacy data center infrastructure

- 3.2.3.5 Surge in strategic partnerships and R&D for advanced cooling solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and Innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Regulatory guideline

- 3.5.1 North America

- 3.5.1.1 U.S.: American Innovation and Manufacturing (AIM) Act

- 3.5.1.2 Canada: Canadian Environmental Protection Act (CEPA)

- 3.5.2 Europe

- 3.5.2.1 Germany: EU F-Gas Regulation (EU 2024/573)

- 3.5.2.2 UK: UK Fluorinated Greenhouse Gases Regulations

- 3.5.2.3 France: RE2020 Environmental Regulation (Buildings & Cooling Efficiency)

- 3.5.2.4 Italy: National Energy Efficiency Directive Implementation

- 3.5.3 Asia Pacific

- 3.5.3.1 China: Kigali Amendment Implementation Framework

- 3.5.3.2 India: Ozone Depleting Substances and HFC Phase-down Rules

- 3.5.3.3 Japan: Act on Rational Use and Proper Management of Fluorocarbons

- 3.5.3.4 Australia: Ozone Protection and Synthetic Greenhouse Gas Management Act

- 3.5.4 Latin America

- 3.5.4.1 Brazil: National Solid Waste Policy (PNRS - Cooling Equipment Inclusion)

- 3.5.4.2 Mexico: General Law on Climate Change

- 3.5.4.3 Argentina: National Environmental Protection Framework

- 3.5.5 MEA

- 3.5.5.1 UAE: Federal Law No. 24 for Environmental Protection

- 3.5.5.2 Saudi Arabia: Saudi Energy Efficiency Program (SEEP)

- 3.5.5.3 South Africa: National Environmental Management: Air Quality Act (NEMAQA)

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Data Center Capacity & Infrastructure Landscape

- 3.9.1 Installed capacity (MW) by country

- 3.9.2 Expansion pipeline 2025-2027

- 3.9.3 Utilization rates & supply demand

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-Driven Disruption of Existing Business Models

- 3.10.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Service Delivery Capacity & Provider Infrastructure (Driven by Primary Research)

- 3.11.1 Provider Network Density & Coverage by Region (Driven by Primary Research)

- 3.11.2 Capacity Gaps & Addressable Demand Mismatch (Driven by Primary Research)

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.13.1 Base Case - Key Macro & Industry Variables Driving CAGR

- 3.13.2 Optimistic Scenarios - Favourable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company Tier Benchmarking

- 4.6.1 Tier Classification Criteria & Qualifying Thresholds

- 4.6.2 Tier Positioning Matrix by Revenue, Geography & Innovation

Chapter 5 Market Estimates & Forecast, By Refrigerant, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 HFCs

- 5.2.1 R-134A

- 5.2.2 R-404A

- 5.3 HFOs

- 5.4 Others

Chapter 6 Market Estimates & Forecast, By Data Center, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Enterprise

- 6.3 Colocation

- 6.4 Cloud

- 6.5 Hyperscale

Chapter 7 Market Estimates & Forecast, By Cooling, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Air cooling

- 7.3 Liquid cooling

- 7.4 Free cooling

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 IT cooling system

- 8.3 Facility cooling system

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 BFSI

- 9.3 IT and Telecom

- 9.4 Government and Defense

- 9.5 Healthcare

- 9.6 Energy

- 9.7 Manufacturing

- 9.8 Retail

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Belgium

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 AGC

- 11.1.2 Arkema

- 11.1.3 Chemours Company

- 11.1.4 Daikin Industries

- 11.1.5 Dongyue

- 11.1.6 Linde plc

- 11.1.7 Orbia Fluor & Energy Materials

- 11.1.8 Sinochem

- 11.1.9 Solstice Advanced Materials

- 11.1.10 Zhejiang Juhua

- 11.2 Regional Players

- 11.2.1 Central Glass

- 11.2.2 Changshu 3F Zhonghao New Chemical

- 11.2.3 Gujarat Fluorochemicals (GFL)

- 11.2.4 Halocarbon Products Corporation

- 11.2.5 Kanto Denka Kogyo

- 11.2.6 Navin Fluorine International

- 11.2.7 Sanmei Chemical (Zhejiang Sanmei)

- 11.2.8 Shandong Huaan New Material

- 11.2.9 SRF Limited

- 11.2.10 Zhejiang Yonghe Refrigerant

- 11.3 Emerging Players

- 11.3.1 Sanmei Chemical

- 11.3.2 Shandong Huaan New Material

- 11.3.3 Tazzetti

- 11.3.4 Zhejiang Yonghe Refrigerant