PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038356

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038356

Wireless Home Security Camera Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

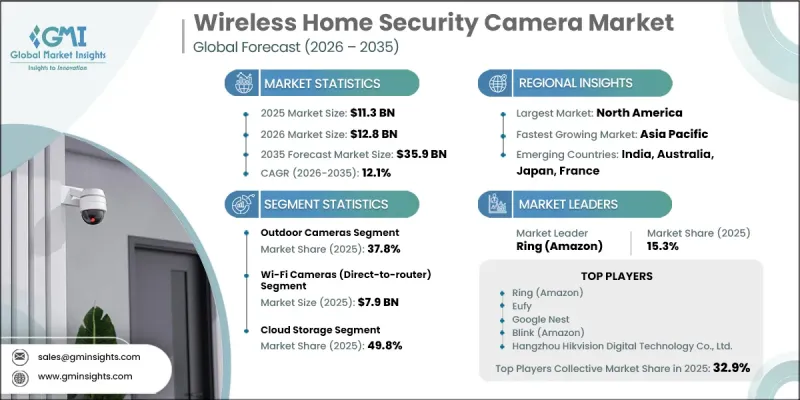

The Global Wireless Home Security Camera Market was valued at USD 11.3 billion in 2025 and is estimated to grow at a CAGR of 12.1% to reach USD 35.9 billion by 2035.

The market growth is driven by increasing safety concerns in urban residential areas, rising adoption of smart home ecosystems, and growing demand for remote monitoring and real-time surveillance solutions. Continuous improvements in AI-based video analytics are enhancing object detection accuracy and reducing false alarms, which is increasing consumer trust in connected security systems. Declining hardware costs are also making wireless cameras more affordable across both developed and emerging economies. In addition, the integration of cloud storage services, mobile-based monitoring applications, and home automation platforms is strengthening overall product adoption. Expanding smartphone penetration and improved internet connectivity are further supporting real-time access to surveillance data, making wireless home security cameras a core component of modern connected living environments across global residential markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.3 Billion |

| Forecast Value | $35.9 Billion |

| CAGR | 12.1% |

The outdoor camera segment accounted for a 37.8% share in 2025, driven by its essential role in external property monitoring and intrusion prevention. These systems are widely preferred due to their durability, weather resistance, wide field of view, and enhanced night vision capabilities. Growing demand for continuous perimeter security and instant alerts has further reinforced their adoption across residential properties in multiple regions.

The Wi-Fi camera segment captured USD 7.9 billion in 2025, supported by its simple installation process and compatibility with existing wireless networks. These systems do not require additional hubs, making them highly convenient for residential users. Their integration with mobile applications and smart home platforms enables seamless remote monitoring, contributing to strong and consistent demand across various consumer segments.

North America Wireless Home Security Camera Market captured a 35.5% share in 2025. Market expansion in the region is supported by rising concerns regarding residential security, increasing penetration of smart home devices, and strong awareness of connected surveillance technologies. Adoption of AI-enabled cameras integrated with home automation systems is particularly strong across the U.S. and Canada. Continued investment in broadband infrastructure and the rollout of advanced connectivity technologies, including high-speed internet and next-generation mobile networks, are further enhancing market growth.

Key companies operating in the Wireless Home Security Camera Industry include Arlo Technologies, Inc., Hangzhou Hikvision Digital Technology Co., Ltd., Ring (Amazon), Google Nest, Swann Communications Pty. Ltd., Wyze Labs, Inc., Xiaomi Corporation, Reolink, Lorex Technology Inc, SimpliSafe, Inc., CP Plus International, D-Link Corporation, Hanwha Techwin Co., Ltd., Amcrest Technologies, Blink (Amazon), Eufy, Frontpoint Security Solutions, LLC, Guardian Protection Services, Inc., NRG Energy, K&F Concept, and Vector Security, Inc. Companies in the Wireless Home Security Camera Market are focusing on advancing artificial intelligence capabilities to improve motion detection accuracy, facial recognition, and real-time threat identification. Many players are investing in cloud-based storage platforms and subscription-based services to generate recurring revenue and enhance data accessibility. Integration with smart home ecosystems and voice-controlled assistants is also being prioritized to improve user convenience and ecosystem compatibility. Firms are expanding product portfolios with high-resolution, energy-efficient, and battery-operated camera systems to meet diverse consumer needs. Strategic partnerships with telecom providers and smart home platform developers are supporting broader distribution and ecosystem integration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Connectivity type trends

- 2.2.3 Resolution trends

- 2.2.4 Storage type trends

- 2.2.5 Distribution channel trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising urban residential burglary rates globally

- 3.2.1.2 Smart home ecosystem adoption accelerating device integration

- 3.2.1.3 AI-powered motion detection reducing false alerts

- 3.2.1.4 Growing demand for remote home monitoring via mobile apps

- 3.2.1.5 Declining hardware costs enabling mass affordability

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy concerns and regulatory scrutiny increasing

- 3.2.2.2 Cybersecurity vulnerabilities in connected camera networks

- 3.2.3 Market opportunities

- 3.2.3.1 Edge AI reducing cloud dependency and latency

- 3.2.3.2 Integration with voice assistants and home automation platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Indoor cameras

- 5.3 Outdoor cameras

- 5.4 Doorbell cameras

Chapter 6 Market Estimates and Forecast, By Connectivity Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Wi-Fi cameras (Direct-to-router)

- 6.3 Gateway/bridge-based cameras

- 6.4 Cellular cameras (4G/5G-enabled)

Chapter 7 Market Estimates and Forecast, By Resolution, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 HD (≤1080p)

- 7.3 2K (1440p)

- 7.4 Ultra HD (4K and above)

Chapter 8 Market Estimates and Forecast, By Storage Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Cloud storage

- 8.3 Local storage (SD/NVR)

- 8.4 Hybrid storage

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Online

- 9.3 Offline

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Ring

- 11.1.2 Google Nest

- 11.1.3 Hangzhou Hikvision Digital Technology Co., Ltd.

- 11.1.4 Xiaomi Corporation

- 11.1.5 Arlo Technologies, Inc.

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Amcrest Technologies

- 11.2.1.2 Blink

- 11.2.1.3 Guardian Protection Services, Inc.

- 11.2.1.4 SimpliSafe, Inc.

- 11.2.1.5 Frontpoint Security Solutions, LLC

- 11.2.1.6 Vector Security, Inc.

- 11.2.1.7 Lorex Technology Inc

- 11.2.2 Asia Pacific

- 11.2.2.1 CP Plus International

- 11.2.2.2 D-Link Corporation

- 11.2.2.3 Hanwha Techwin Co., Ltd.

- 11.2.2.4 Reolink

- 11.2.3 Europe

- 11.2.3.1 NRG Energy

- 11.2.3.2 Swann Communications Pty. Ltd.

- 11.2.1 North America

- 11.3 Niche Players/Disruptors

- 11.3.1 Eufy

- 11.3.2 Wyze Labs, Inc.

- 11.3.3 K&F Concept