PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038372

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038372

High-Speed Data Converter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

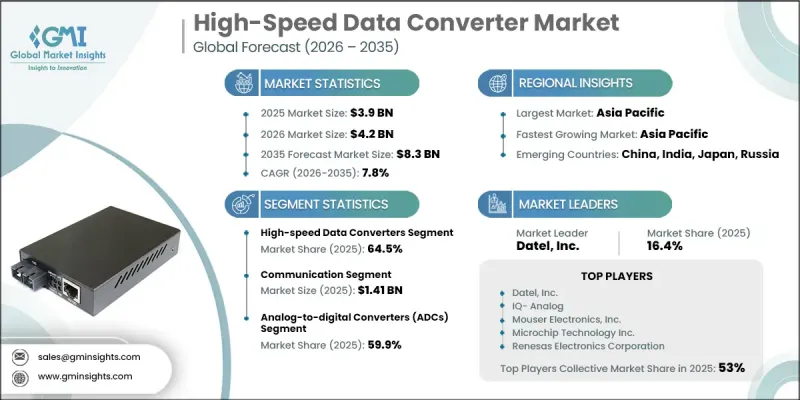

The Global High-Speed Data Converter Market was valued at USD 3.9 billion in 2025 and is estimated to grow at a CAGR of 7.8% to reach USD 8.3 billion by 2035.

The market is witnessing strong expansion as industries increasingly rely on high-speed and real-time data processing across communication, computing, and sensing applications. Rising digitalization and the continuous growth of data-intensive ecosystems are increasing the need for advanced signal conversion technologies. Expanding digital infrastructure and the growing requirement for higher bandwidth capabilities are further strengthening demand for high-performance analog-to-digital and digital-to-analog converters. Rapid advancements in semiconductor design and fabrication technologies are improving converter efficiency, accuracy, and processing speed. The increasing integration of intelligent systems in connected environments is also contributing to market expansion. Demand is further reinforced by the growing complexity of modern electronic systems, which require precise and high-speed data handling. Continuous innovation in converter architectures is enhancing performance across multiple end-use industries. The shift toward real-time analytics, edge computing, and high-frequency signal processing is accelerating adoption, making high-speed data converters a critical component in next-generation electronic systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.9 Billion |

| Forecast Value | $8.3 Billion |

| CAGR | 7.8% |

The growth of the market is strongly supported by the rapid rollout of advanced wireless communication networks, including next-generation connectivity platforms that require low latency and high bandwidth performance. Expanding wireless infrastructure, increasing deployment of sensing and radar technologies, and rising integration of advanced automotive electronics are further driving demand. The increasing use of data-centric applications across cloud and edge environments is also contributing to market growth. In addition, the expansion of autonomous and unmanned systems is creating new opportunities for high-performance data conversion technologies. Continuous improvements in semiconductor architectures are enabling better system efficiency, improved signal integrity, and broader application scope across industries.

The high-speed data converters segment accounted for a 64.5% share in 2025 owing to its extensive use across communication systems, radar applications, aerospace technologies, and high-performance computing platforms. These converters are essential for applications requiring rapid signal processing, high bandwidth handling, and real-time data accuracy. Their ability to support large-scale and complex operations while maintaining precision makes them a core component in advanced electronic systems. The growing reliance on high-speed processing across critical industries continues to strengthen demand for this segment.

The test and measurement segment is projected to grow at a CAGR of 8.9% during 2026-2035, driven by increasing demand for high-precision and high-speed signal analysis. Rising complexity in electronic systems and the need for accurate real-time measurement are supporting adoption across scientific research, semiconductor evaluation, and defense applications. The requirement for high-resolution testing solutions in advanced technologies is further accelerating the use of high-speed data converters in this segment.

North America High-Speed Data Converter Market held a share of 29.1% in 2025, supported by strong digital infrastructure development and rapid technological adoption. The region continues to witness increased deployment of high-bandwidth communication networks and expansion of data center infrastructure. Early adoption of advanced connectivity technologies is further driving demand for high-speed data converters. A well-established semiconductor ecosystem, combined with strong capabilities in defense and aerospace industries, continues to support regional market growth and technological advancement.

Major players in the Global High-Speed Data Converter Market include Analog Devices, Inc., Broadcom Inc., Cirrus Logic, Inc., Asahi Kasei Microdevices Corporation, Avia Semiconductor Ltd., Infineon Technologies AG, Datel, Inc., IQ-Analog, Mouser Electronics, Inc., MediaTek Inc., Microchip Technology Inc., NXP Semiconductors, ON Semiconductor, Qualcomm Technologies, Inc., Realtek Semiconductor Corp., Renesas Electronics Corporation, ROHM Semiconductor, Samsung Electronics Co., Ltd., Skyworks Solutions, Inc., STMicroelectronics, Texas Instruments, and Xilinx, Inc. Companies operating in the Global High-Speed Data Converter Market are focusing on advanced semiconductor innovation, product miniaturization, and performance optimization to strengthen their competitive position. They are investing in research and development to enhance signal accuracy, increase processing speed, and improve energy efficiency. Strategic collaborations and partnerships are being used to accelerate technological advancement and expand market reach. Firms are also diversifying product portfolios to address the growing demand across communication, automotive, and industrial sectors. Emphasis on integration with AI-driven systems and edge computing platforms is supporting next-generation applications.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Sampling rate trends

- 2.2.3 Resolution trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid adoption of 5G and next-generation wireless communication infrastructure

- 3.2.1.2 Increasing demand for high-performance data acquisition systems

- 3.2.1.3 Expansion of data-centric applications in cloud computing and data centers

- 3.2.1.4 Growing integration of high-speed converters in radar, imaging, and defense systems

- 3.2.1.5 Rising adoption of advanced automotive electronics and autonomous systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High power consumption and thermal management constraints in high-speed converters

- 3.2.2.2 Design complexity and integration challenges in high-frequency systems

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for high-speed converters in aerospace and space electronics

- 3.2.3.2 Increasing adoption of high-speed converters in medical imaging and diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035

- 5.1 Key trends

- 5.2 Analog-to-digital converters (ADCs)

- 5.3 Digital-to-analog converters (DACs)avionics software

Chapter 6 Market Estimates and Forecast, By Sampling Rate, 2022 - 2035

- 6.1 Key trends

- 6.2 High-speed data converters

- 6.3 General-purpose data converters

Chapter 7 Market Estimates and Forecast, By Resolution, 2022 - 2035

- 7.1 Key trends

- 7.2 Line Fit (OEM)

- 7.3 Aftermarket (retrofit & MRO)

- 7.4 Above 8MP

- 7.5 8-bit

- 7.6 10-bit

- 7.7 12-bit

- 7.8 16-bit

- 7.9 24-bit and above

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Communication

- 8.4 Industrial automation

- 8.5 Test & management

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Datel, Inc.

- 10.1.2 IQ- Analog

- 10.1.3 Mouser Electronics, Inc.

- 10.1.4 Microchip Technology Inc.

- 10.1.5 Renesas Electronics Corporation

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Analog Devices, Inc.

- 10.2.1.2 Broadcom Inc.

- 10.2.1.3 Cirrus Logic, Inc.

- 10.2.1.4 ON Semiconductor

- 10.2.1.5 Qualcomm Technologies, Inc.

- 10.2.1.6 Skyworks Solutions, Inc.

- 10.2.1.7 Texas Instruments

- 10.2.1.8 Xilinx, Inc.

- 10.2.2 Europe

- 10.2.2.1 Infineon Technologies AG

- 10.2.2.2 NXP Semiconductors

- 10.2.2.3 STMicroelectronics

- 10.2.2.4 ROHM Semiconductor

- 10.2.3 Asia Pacific

- 10.2.3.1 Asahi Kasei Microdevices Corporation

- 10.2.3.2 MediaTek Inc.

- 10.2.3.3 Realtek Semiconductor Corp.

- 10.2.3.4 Samsung Electronics Co., Ltd.

- 10.2.3.5 Avia Semiconductor Ltd.

- 10.2.1 North America