PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038378

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038378

Dehydrated Green Bean Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

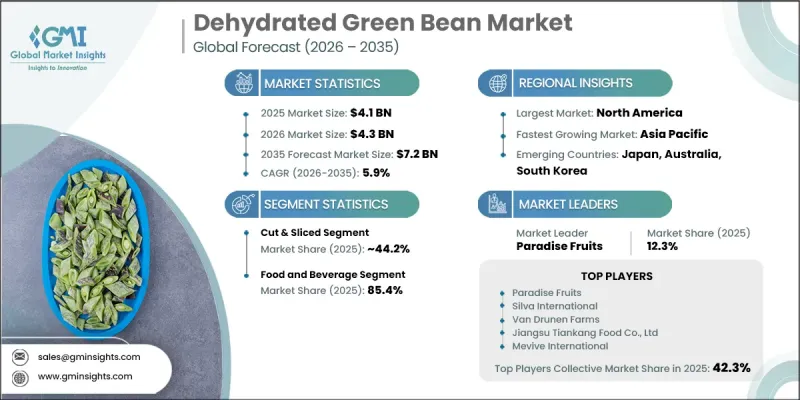

The Global Dehydrated Green Bean Market was valued at USD 4.1 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 7.2 billion by 2035.

The market is expanding steadily due to rising demand for shelf-stable vegetable ingredients across the food processing industry. Dehydrated green beans are widely utilized because they offer extended storage life, reduced transportation weight, and consistent availability throughout the year. Increasing consumer preference for convenience-oriented and minimally processed food products is further supporting market growth. Health-focused dietary trends are also contributing to stronger demand, as consumers increasingly seek natural, nutrient-rich ingredients in packaged foods. Advancements in dehydration technologies have improved product quality, color retention, and rehydration performance, making these ingredients more versatile for industrial use. In addition, the expansion of global distribution channels and improved cold chain alternatives are enhancing product accessibility. Growing consumption of ready-to-eat meals and long-shelf-life food solutions is reinforcing demand across multiple end-use industries, ensuring stable market expansion over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.1 Billion |

| Forecast Value | $7.2 Billion |

| CAGR | 5.9% |

The cut and sliced segment accounted for 44.2% share in 2025 and is projected to grow at a CAGR of 4.3% by 2035. This format is widely preferred due to its ease of use and suitability for quick preparation in both household and commercial food preparation environments. Its consistent texture and nutritional value make it adaptable for a variety of culinary applications. Rising demand for ready-to-use vegetable ingredients continues to support its strong market position.

The food & beverage segment held a share of 85.4% in 2025. This dominance is attributed to increasing consumption of plant-based and convenience food products. Dehydrated green beans are extensively incorporated into processed food formulations due to their long shelf life and retained nutritional properties. Growing preference for clean-label and naturally derived ingredients is further strengthening their role in packaged food production, supporting sustained demand across the food processing sector.

North America Dehydrated Green Bean Market was valued at USD 1.2 billion in 2025 and is projected to grow at a CAGR of 5.9% from 2026 to 2035. Market expansion in the region is driven by rising health awareness and increasing demand for convenient, plant-based food ingredients. Busy lifestyles are encouraging greater consumption of easy-to-prepare food products. The strong presence of a developed foodservice industry and increasing adoption of vegetarian and vegan diets are also contributing to steady market growth across the region.

Key companies operating in the Global Dehydrated Green Bean Market include Van Drunen Farms, BC Foods, Silva International, Xinghua Lianfu Food Co., Ltd, Mevive International, Harmony House Foods, Richfield Food, European Freeze Dry, Paradise Fruits, Jiangsu Tiankang Food Co., Ltd, and Sensient Natural Ingredients. Companies in the dehydrated green bean market are focusing on strengthening their market position through product innovation, process optimization, and capacity expansion. Many players are investing in advanced dehydration technologies to improve product quality, shelf life, and nutritional retention. Strategic partnerships with food manufacturers and distributors are helping expand market reach and improve supply chain efficiency. Firms are also emphasizing clean-label and natural ingredient positioning to align with evolving consumer preferences. Expansion into new geographic markets and development of diversified product formats are further supporting growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Form

- 2.2.3 Application

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for convenience foods

- 3.2.1.2 Rising health-conscious consumer preferences

- 3.2.1.3 Technological advancements in dehydration and processing

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production and processing

- 3.2.2.2 Limited consumer awareness about the benefits of dehydrated green beans

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for convenient, healthy snack options

- 3.2.3.2 Increasing popularity of plant-based and vegetarian diets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By form

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Whole dried beans

- 5.3 Cut & sliced

- 5.3.1 Sliced

- 5.3.2 Diced / cubed

- 5.4 Granulated

- 5.4.1 Chopped

- 5.4.2 Minced

- 5.4.3 Flakes

- 5.5 Powdered

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Food & beverages

- 6.2.1 Food manufacturing

- 6.2.2 Food service

- 6.2.3 Retail consumer products

- 6.3 Animal feed

- 6.3.1 Pet food

- 6.3.2 Livestock feed

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Supermarkets / hypermarkets

- 7.3 Convenience stores

- 7.4 Online retail

- 7.5 Specialty stores

- 7.6 Food service channels

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Van Drunen Farms

- 9.2 BC Foods

- 9.3 Silva International

- 9.4 Xinghua Lianfu Food Co., Ltd

- 9.5 Mevive International

- 9.6 Harmony House Foods

- 9.7 Richfield Food

- 9.8 European Freeze Dry

- 9.9 Paradise Fruits

- 9.10 Jiangsu Tiankang Food Co., Ltd

- 9.11 Sensient Natural Ingredients