PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038402

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038402

Heat Stress Monitor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

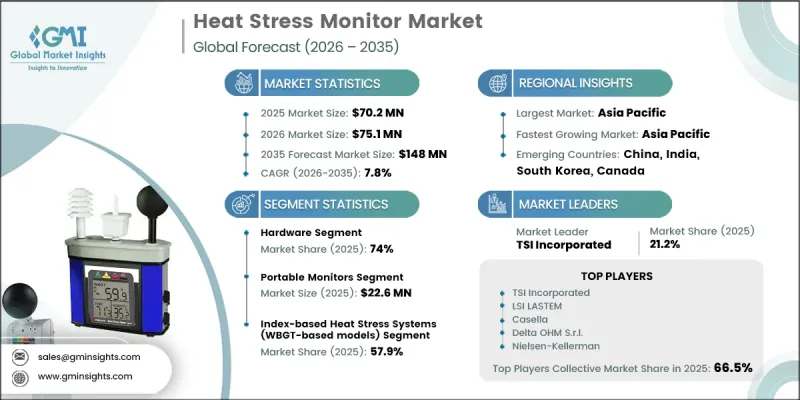

The Global Heat Stress Monitor Market was valued at USD 70.2 million in 2025 and is estimated to grow at a CAGR of 7.8% to reach USD 148 million by 2035.

The market expansion is attributed to stricter occupational heat safety regulations across industries and the increasing deployment of WBGT-based monitoring solutions in construction and mining operations. Rising frequency of extreme heat conditions across major industrial regions is further intensifying demand for real-time monitoring systems. The growing adoption of wearable and IoT-enabled devices is reshaping workplace safety practices by enabling continuous environmental and physiological tracking. Integration of heat stress monitoring solutions into defense operations and workforce safety programs is also strengthening market penetration. Increasing climate variability is exposing workers to prolonged heat exposure risks, driving organizations to adopt advanced mitigation strategies. In addition, expanding implementation of heat illness prevention initiatives across manufacturing and construction sectors is accelerating product adoption. Continuous technological improvements in real-time sensing, combined with portable and connected monitoring systems, are enhancing operational efficiency and broadening market reach across industrial applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $70.2 Million |

| Forecast Value | $148 Million |

| CAGR | 7.8% |

The hardware segment accounted for 74% share in 2025. Hardware solutions dominate the heat stress monitor industry due to their essential role in capturing accurate real-time environmental and physiological data in industrial settings. Devices such as WBGT meters, portable monitoring systems, and wearable sensors are widely used for safety compliance and on-site risk management. Their precision, reliability, and seamless integration into occupational safety frameworks make them critical across construction, mining, and manufacturing environments.

The portable monitors segment reached USD 22.6 million in 2025. Strong demand is driven by their extensive use in field-based operations such as construction, oil and gas, and mining activities. Their mobility, rapid deployment capability, and real-time data measurement make them highly suitable for dynamic and high-risk environments. These devices support immediate safety decisions and ensure adherence to occupational heat safety regulations, maintaining strong adoption across outdoor industrial applications.

North America Heat Stress Monitor Market accounted for 28.1% share in 2025. The region's growth is supported by rising regulatory enforcement focused on occupational heat safety and increasing cases of heat-related illnesses across industries including construction, logistics, and manufacturing. The adoption of WBGT-based systems and wearable monitoring technologies is expanding steadily across the United States and Canada. Government bodies and private organizations are increasingly investing in IoT-enabled monitoring platforms and real-time analytics solutions to enhance worker safety and improve heat risk management practices.

Key companies operating in the Global Heat Stress Monitor Industry include TSI Incorporated, Sper Scientific, Lutron Electronic Enterprise, Casella, TES Electrical Electronic Corp., Delta OHM S.r.l., AZ Instrument Corp., REED Instruments, Nielsen-Kellerman, Tenmars Electronics, PCE Instruments, LSI LASTEM, Kyoto Electronics Manufacturing, Sato Keiryoki Mfg. Co., Ltd., General Tools & Instruments, and Romteck Australia. Companies in the Heat Stress Monitor Market are focusing on strengthening their market position through continuous product innovation and integration of advanced sensor technologies. Many players are investing in IoT-enabled and wearable monitoring solutions to provide real-time data analytics and improved user safety. Strategic collaborations with industrial organizations are helping expand adoption across high-risk sectors. Firms enhance product portability, accuracy, and durability to meet field requirements in extreme environments. Expansion into emerging markets, along with compliance-driven product development aligned with occupational safety regulations, is further supporting growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Offering trends

- 2.2.2 Product type trends

- 2.2.3 Technology trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 OSHA heat safety rulemaking accelerating workplace compliance demand

- 3.2.1.2 Rising WBGT monitoring adoption in construction and mining sectors

- 3.2.1.3 Increasing heatwave frequency across United States and India industrial zones

- 3.2.1.4 Defense sector investments in soldier heat strain monitoring systems

- 3.2.1.5 Integration of IoT-enabled wearable heat stress monitors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High calibration costs for accurate WBGT measurement devices

- 3.2.2.2 Data accuracy issues in wearable physiological sensors

- 3.2.3 Market opportunities

- 3.2.3.1 AI-based predictive heat stress analytics integration

- 3.2.3.2 Smart PPE adoption across logistics and warehousing sectors

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Offering, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software & analytics

- 5.4 Services

Chapter 6 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Fixed/area monitors

- 6.3 Portable monitors

- 6.4 Wearable monitors

Chapter 7 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Environmental heat stress monitoring systems

- 7.3 Physiological heat strain monitoring systems

- 7.4 Index-based heat stress systems (WBGT-based models)

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Manufacturing

- 8.3 Construction

- 8.4 Oil & Gas

- 8.5 Energy & Utilities

- 8.6 Mining

- 8.7 Agriculture

- 8.8 Military & Defense

- 8.9 Sports & Athletics

- 8.10 Healthcare & Research

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 TSI Incorporated

- 10.1.2 Delta OHM S.r.l.

- 10.1.3 LSI LASTEM

- 10.1.4 Casella

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Nielsen-Kellerman

- 10.2.1.2 REED Instruments

- 10.2.1.3 Sper Scientific

- 10.2.1.4 General Tools & Instruments

- 10.2.2 Asia Pacific

- 10.2.2.1 AZ Instrument Corp.

- 10.2.2.2 TES Electrical Electronic Corp.

- 10.2.2.3 Tenmars Electronics

- 10.2.2.4 Sato Keiryoki Mfg. Co., Ltd.

- 10.2.2.5 Kyoto Electronics Manufacturing

- 10.2.2.6 Lutron Electronic Enterprise

- 10.2.3 Europe

- 10.2.3.1 PCE Instruments

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Romteck Australia