PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038408

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038408

Mental Health Apps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

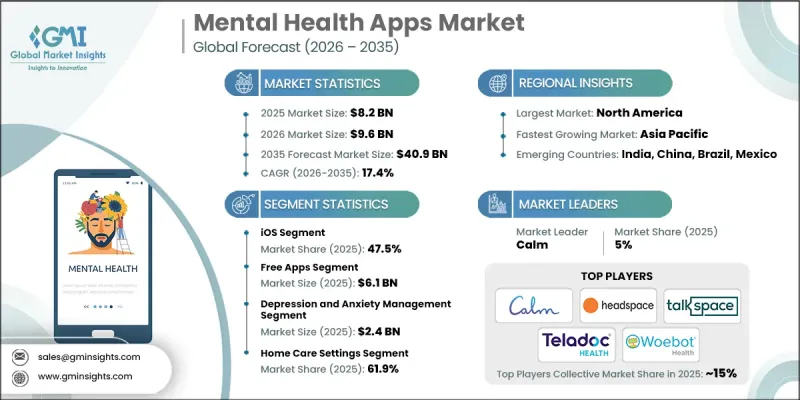

The Global Mental Health Apps Market was valued at USD 8.2 billion in 2025 and is estimated to grow at a CAGR of 17.4% to reach USD 40.9 billion by 2035.

Growth is driven by the increasing prevalence of mental health conditions and the rising acceptance of virtual therapy solutions. Greater awareness of mental well-being and the importance of early intervention is further supporting market expansion. Digital platforms enable users to access therapy, self-care tools, and behavioral support in a more convenient and scalable manner. The integration of advanced technologies such as artificial intelligence, conversational chat systems, and digital therapeutic models is improving user engagement and personalization. Employers are also increasingly adopting structured wellness programs that incorporate digital mental health tools to support workforce well-being. Additionally, preventive care approaches and self-guided mental wellness practices are gaining traction, further strengthening adoption across diverse user groups. These combined factors are positioning mental health applications as an essential component of modern healthcare ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8.2 Billion |

| Forecast Value | $40.9 Billion |

| CAGR | 17.4% |

The iOS segment held a share of 47.5% in 2025. This leadership is supported by strong smartphone penetration and high digital engagement among users. The ecosystem's stable performance, enhanced privacy features, and seamless integration with wearable devices contribute to its strong adoption. Subscription-based models are widely supported within this environment, encouraging sustained user engagement. Developers also tend to prioritize premium wellness and clinically oriented applications for this platform due to its consistent performance capabilities and user experience quality.

The free apps segment generated USD 6.1 billion in 2025, supported by its wide accessibility and broad user base. These applications provide mental health support without financial barriers, making them accessible to individuals across different income groups. The availability of no-cost solutions encourages higher adoption rates, particularly among users seeking initial or supplementary mental health support. This affordability factor plays a key role in expanding overall market reach and increasing user engagement across diverse populations.

North America Mental Health Apps Market accounted for a 57.6% share in 2025. The region's high incidence of mental health conditions, including anxiety, depression, and substance-related disorders, is driving demand for digital solutions. Increasing awareness and acceptance of mental health care are further supporting market expansion. In addition, growing confidence in digital healthcare tools is encouraging wider adoption among both consumers and healthcare professionals. The shift toward technology-enabled care delivery is reinforcing the role of mobile applications in supporting mental wellness across the region.

Key companies operating in the Global Mental Health Apps Market include Calm, Headspace Inc., Talkspace, Teladoc Health, Inc., Woebot, Wysa, Spring Health, BetterSleep, Fabulous, 7 Cups of Tea, Youper, Inc., Mindscape, Dario Mind, MoodMission Pty Ltd., and rhope. Companies in the Mental Health Apps Market are strengthening their competitive position through technological advancement, strategic partnerships, and user-focused innovation. They are integrating artificial intelligence and machine learning capabilities to enhance personalization and improve user engagement. Many players are expanding their service offerings by introducing subscription-based models and premium wellness features. Collaborations with healthcare providers and corporate organizations are helping increase adoption across institutional channels. In addition, companies are focusing on improving data security and privacy standards to build user trust. Expansion into emerging markets and continuous product updates are further supporting growth, while investment in digital therapeutics and behavioral health solutions is enhancing long-term market positioning.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Platform type trends

- 2.2.3 Revenue model trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of virtual therapy for mental health

- 3.2.1.2 Increasing awareness regarding mental health

- 3.2.1.3 Rise in target population suffering from mental conditions

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy and connectivity issues

- 3.2.3 Opportunities

- 3.2.3.1 Integration with wearable and biometric data

- 3.2.3.2 Corporate wellness and B2B mental health platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Pricing analysis, 2025 (Driven by Primary Research)

- 3.8 Impact of AI & generative AI on the market (Driven by Primary Research)

- 3.8.1 AI-driven disruption of existing business models

- 3.8.2 GenAI use cases & adoption roadmap by segment

- 3.9 Reimbursement scenario

- 3.10 Start-up scenario

- 3.11 Gap analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by Primary Research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Platform Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 iOS

- 5.3 Android

- 5.4 Other platform type

Chapter 6 Market Estimates and Forecast, By Revenue Model, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Free apps

- 6.3 Subscription-based

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Depression and anxiety management

- 7.3 Meditation management

- 7.4 Stress management

- 7.5 Wellness management

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Home care settings

- 8.3 Mental hospitals

- 8.4 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 7 cups of Tea

- 10.2 BetterSleep

- 10.3 Calm

- 10.4 Dario Mind

- 10.5 Fabulous

- 10.6 Headspace Inc.

- 10.7 Mindscape

- 10.8 MoodMission Pty Ltd.

- 10.9 rhope

- 10.10 Spring Health

- 10.11 Talkspace

- 10.12 Teladoc Health, Inc.

- 10.13 Woebot

- 10.14 Wysa

- 10.15 Youper, Inc.