PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038410

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038410

Electric Vehicle Battery Case Box Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

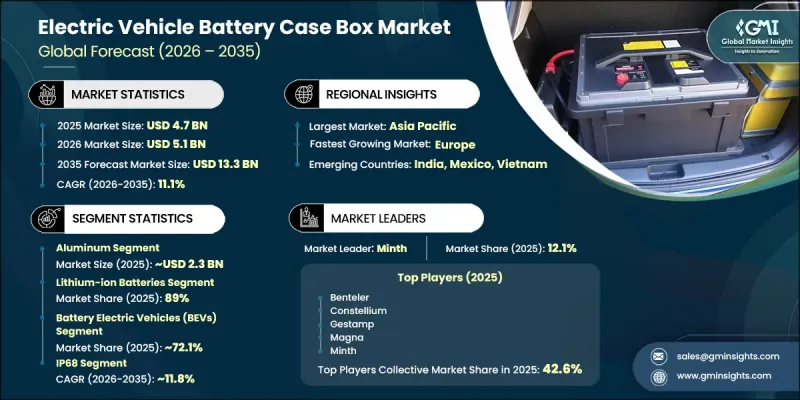

The Global Electric Vehicle Battery Case Box Market was valued at USD 4.7 billion in 2025 and is estimated to grow at a CAGR of 11.1% to reach USD 13.3 billion by 2035.

The market is experiencing expansion driven by the rapid evolution of electric mobility and the rising need for safer, lighter, and more thermally efficient battery enclosure systems. Material innovation and structural engineering are playing a critical role in shaping product development, with aluminum gaining traction due to its lightweight strength characteristics, while composite materials are increasingly favored for their design adaptability and performance efficiency. Regulatory frameworks focused on domestic sourcing requirements and recycled material usage are further reshaping supply chains, compelling manufacturers to expand production capacity across regional hubs. Additionally, lithium-ion battery integration remains the dominant foundation of demand; while emerging solid-state technologies are introducing new thermal and structural design requirements. The growing complexity of battery systems, combined with higher energy density requirements, is intensifying the need for advanced enclosure solutions that support safety, durability, and thermal regulation. Overall, the market is evolving toward highly engineered, regionally optimized, and material-efficient solutions that align with next-generation electric vehicle platforms.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.7 Billion |

| Forecast Value | $13.3 Billion |

| CAGR | 11.1% |

The aluminum segment accounted for 49% share in 2025 and generated USD 2.3 billion. This dominance is supported by aluminum's high strength-to-weight efficiency and excellent corrosion resistance, particularly in structural underbody applications. Advanced aluminum alloys such as 6000 and 7000 series offer tensile strengths exceeding 300 MPa while maintaining significantly lower density than steel, enabling weight reductions of nearly 40% to 50% without compromising structural integrity. These characteristics contribute to improved vehicle efficiency and extended driving range. Aluminum also supports advanced manufacturing techniques such as extrusion-based frame structures and die-cast corner assemblies, which enhance design integration and simplify production processes. Its ability to improve overall vehicle energy efficiency through reduced mass further strengthens its adoption across electric vehicle platforms.

The lithium-ion battery segment held a 89% share in 2025, valued at USD 4.2 billion, driven by high energy density performance ranging between 150-300 Wh/kg, along with continuous improvements in battery technologies supported by advanced development initiatives. As battery pack capacities increased from about 40 kWh in 2018 to over 65 kWh by 2024, the demand for more sophisticated enclosure systems also rose significantly. Higher-performance battery chemistries, particularly nickel manganese cobalt systems, generate increased thermal loads during high charging and discharging cycles, necessitating advanced cooling integration and structural reinforcement. In contrast, lithium iron phosphate systems generally require simpler thermal management setups and offer lower cost structures. These evolving chemistry profiles are increasingly influencing enclosure design requirements, making thermal and structural compatibility a key engineering focus.

U.S. Electric Vehicle Battery Case Box Market reached USD 691.5 million in 2025 and is projected to grow at a CAGR of 9.6% between 2026 and 2035. Market performance in the country has been shaped by fluctuating policy incentives and regulatory adjustments, although long-term growth remains supported by rising electric vehicle adoption. Government-led initiatives continue to play a crucial role in market expansion, particularly through financial incentives that encourage domestic production of electric vehicles and battery components. Policies such as the Inflation Reduction Act are reinforcing local manufacturing by promoting the use of regionally sourced materials and strengthening supply chain localization within the industry.

Key companies operating in the Electric Vehicle Battery Case Box Market include Novelis (Hindalco), Constellium, Minth Group, SGL Carbon, Benteler, Magna, Kautex, Gestamp, Ningbo Xusheng, and Trinseo. Companies in the Electric Vehicle Battery Case Box Market are actively strengthening their competitive position through investments in advanced material technologies, lightweight engineering solutions, and scalable manufacturing capabilities. Many firms are expanding regional production facilities to align with localization requirements and reduce supply chain risks. Strategic collaborations with automotive OEMs are becoming increasingly common to ensure early integration of enclosure systems into vehicle design platforms. In addition, continuous research and development efforts focus on improving thermal management performance and structural safety features. Manufacturers are also adopting automation and digital production technologies to enhance precision and reduce operational costs. Product innovation, particularly in composite and high-grade aluminum solutions, remains a key strategy for differentiation.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Vehicle

- 2.2.4 Battery Technology

- 2.2.5 Protection Level

- 2.2.6 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Accelerating Global EV Adoption & Production Volumes

- 3.2.1.2 Stringent Safety & Regulatory Standards for Battery Protection

- 3.2.1.3 Advancements in Lightweight Materials & Manufacturing Technologies

- 3.2.1.4 Growing Demand for High-Performance Lithium-ion Battery Systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Material & Production Costs for Advanced Enclosures

- 3.2.2.2 Supply Chain Disruptions & Material Availability Constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Rising Demand for Solid-State Battery Enclosures

- 3.2.3.2 Expansion in Emerging EV Markets

- 3.2.3.3 Development of Recyclable & Sustainable Case Materials

- 3.2.1 Growth drivers

- 3.3 Technology and innovation landscape

- 3.3.1 Current technologies

- 3.3.1.1 Aluminum Battery Case Enclosures

- 3.3.1.2 Steel-Based Battery Housing Systems

- 3.3.1.3 Structural Battery Pack Casings

- 3.3.2 Emerging technologies

- 3.3.2.1 Composite Material Battery Enclosures

- 3.3.2.2 Liquid Cooling Integrated Battery Cases

- 3.3.2.3 3D-Printed Battery Housing Systems

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Pricing analysis (Driven by Primary Research)

- 3.5.1 Historical price trend analysis

- 3.5.2 Pricing strategy by player type (Premium / Value / Cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 US - National Highway Traffic Safety Administration (NHTSA)

- 3.6.1.2 Canada - Transport Canada (TC)

- 3.6.2 Europe

- 3.6.2.1 EU - European Commission (EC)

- 3.6.2.2 Germany - Federal Motor Transport Authority (KBA)

- 3.6.3 Asia Pacific

- 3.6.3.1 China - Ministry of Industry and Information Technology (MIIT)

- 3.6.3.2 India - Bureau of Indian Standards (BIS)

- 3.6.4 Latin America

- 3.6.4.1 Brazil - INMETRO

- 3.6.4.2 Argentina - National Institute of Industrial Technology (INTI)

- 3.6.5 Middle East & Africa

- 3.6.5.1 UAE - Dubai Roads and Transport Authority (RTA)

- 3.6.5.2 South Africa - South African Bureau of Standards (SABS)

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent landscape (Driven by Primary Research)

- 3.10 Cost breakdown analysis

- 3.10.1 Raw material procurement and preparation costs

- 3.10.2 Forming and fabrication processes

- 3.10.3 Machining and precision engineering costs

- 3.10.4 Surface treatment and coating processes

- 3.10.5 Quality inspection and in-line testing costs

- 3.11 Trade Data Analysis (Driven by Paid Database)

- 3.11.1 Import/Export Volume & Value Trends

- 3.11.2 Key Trade Corridors & Tariff Impact

- 3.12 Capacity & Production Landscape (Driven by Primary Research)

- 3.12.1 Installed Capacity by Region & Key Producer

- 3.12.2 Capacity Utilization Rates & Expansion Pipelines

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable Practices

- 3.13.2 Waste Reduction Strategies

- 3.13.3 Energy Efficiency in Production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon Footprint Considerations

- 3.14 Impact of AI & Generative AI on the Market

- 3.14.1 AI-driven disruption of existing business models

- 3.14.2 GenAI use cases & adoption roadmap by segment

- 3.14.3 Risks, limitations & regulatory considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Mn, Units)

- 5.1 Key trends

- 5.2 Aluminum

- 5.3 Steel

- 5.4 Composite Polymers

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Vehicle, 2022 - 2035 ($ Mn, Units)

- 6.1 Key trends

- 6.2 Battery Electric Vehicles (BEVs)

- 6.2.1 Two-wheelers & three-wheelers

- 6.2.2 Passenger cars

- 6.2.3 Commercial vehicles

- 6.3 Hybrid & Plug-in Hybrid Electric Vehicles (HEVs/PHEVs)

- 6.3.1 Passenger cars

- 6.3.2 Commercial vehicles

Chapter 7 Market Estimates and Forecast, By Battery Technology, 2022 - 2035 ($ Mn, Units)

- 7.1 Key trends

- 7.2 Lithium-ion Batteries

- 7.3 Solid-State Batteries

- 7.4 Nickel-Metal Hydride (NiMH) Batteries

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Protection Level, 2022 - 2035 ($ Mn, Units)

- 8.1 Key trends

- 8.2 IP67

- 8.3 IP68

- 8.4 Other Standards

Chapter 9 Market Estimates and Forecast, By Sales Channel, 2022 - 2035 ($ Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Sweden

- 10.3.7 Czech Republic

- 10.3.8 Netherlands

- 10.3.9 Norway

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 South Korea

- 10.4.4 India

- 10.4.5 Thailand

- 10.4.6 Indonesia

- 10.4.7 Vietnam

- 10.4.8 Malaysia

- 10.4.9 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Chile

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Magna

- 11.1.2 Novelis (Hindalco)

- 11.1.3 Constellium

- 11.1.4 Kautex

- 11.1.5 Minth Group

- 11.1.6 Ningbo Xusheng

- 11.1.7 SGL Carbon

- 11.1.8 Thyssenkrupp

- 11.1.9 Gestamp

- 11.1.10 Benteler

- 11.2 Regional players

- 11.2.1 GOHO Tech

- 11.2.2 Xiamen Apollo

- 11.2.3 Zhejiang Qicheng

- 11.2.4 Trinseo

- 11.2.5 Teijin Mobility

- 11.2.6 EMP Tech

- 11.3 Emerging players

- 11.3.1 GF Casting Solutions (Nemak)

- 11.3.2 Dura-Shiloh

- 11.3.3 Wometal

- 11.3.4 XD Thermal