PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038420

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038420

Advanced Ceramics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

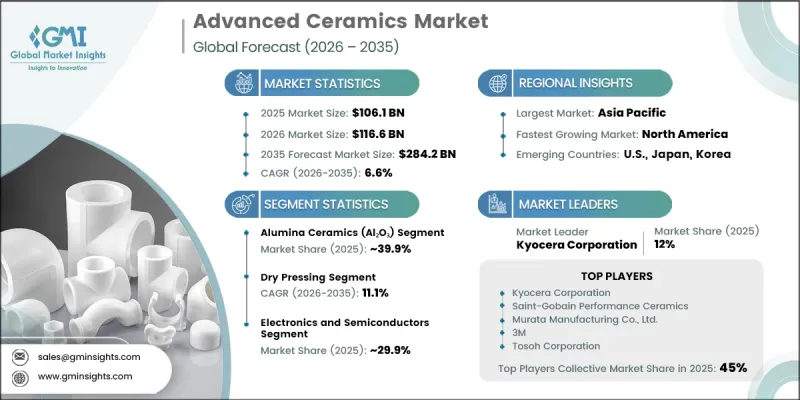

The Global Advanced Ceramics Market was valued at USD 106.1 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 284.2 billion by 2035.

The market has seen consistent growth over the past few years, driven by innovations in electrification, industrial automation, and medical technologies. Advanced ceramics are gaining importance in sectors emphasizing durability, sustainability, and miniaturization. Original equipment manufacturers in clean energy, high-performance computing, and e-mobility rely on ceramics for their heat resistance, wear resistance, and chemical inertness. Biocompatible grades of zirconia and alumina are widely used in medical devices, while aerospace and defense industries utilize ceramic coatings for thermal stability and weight reduction. Geopolitical shifts have prompted the development of local ceramic supply chains in the U.S. and EU, enhancing industrial resilience. Sustainable manufacturing processes and recyclable ceramic products are emerging due to regulatory pressures and corporate initiatives, with companies like CoorsTek and Saint-Gobain investing in low-carbon sintering and closed-loop production systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $106.1 Billion |

| Forecast Value | $284.2 Billion |

| CAGR | % |

The alumina ceramics segment held 39.9% share in 2025 The use of advanced raw materials such as alumina, zirconia, silicon carbide, and silicon nitride is driving applications across electronics, automotive, and medical sectors. These materials offer superior hardness, thermal stability, corrosion resistance, and high-performance miniaturized applications, making them essential for global industrial supply chains.

Dry pressing accounted for the largest share of 27.1% in 2025 and is projected to expand at a CAGR of 11.1% from 2026 to 2035. This process, along with sintering techniques, is widely used to manufacture high-density components with uniform and reliable material properties. Isostatic pressing is also commonly adopted to achieve consistent compaction, particularly for applications requiring high structural integrity. In addition, injection molding and extrusion methods are used to produce complex-shaped parts and continuous profiles tailored to diverse design requirements.

North America Advanced Ceramics Market held a 22.4% share in 2025, reflecting strong regional growth on a global scale. The market demonstrates a high level of technological advancement, driven by robust demand from aerospace, defense, electronics, healthcare, and clean energy industries. The region benefits from well-established research and development capabilities, advanced manufacturing infrastructure, and stringent performance and safety standards. These factors collectively support the development and adoption of high-performance ceramic solutions, strengthening North America's position as a key hub for premium advanced ceramics production and innovation.

Key players in the Global Advanced Ceramics Market include Morgan Advanced Materials, Saint-Gobain Performance Ceramics, Kyocera Corporation, Murata Manufacturing Co., Ltd., CoorsTek Inc., NGK Spark Plug Co., Ltd., McDanel Advanced Ceramic Technologies, CeramTec GmbH, 3M, Rauschert GmbH, Ferrotec Holdings Corporation, and Elan Technology. Companies in the Advanced Ceramics Market strengthen their position through multiple strategic initiatives. They are investing heavily in research and development to create high-performance, sustainable, and cost-efficient ceramics. Mergers, acquisitions, and strategic partnerships expand technological capabilities, production capacity, and geographic reach. Firms are also adopting low-carbon manufacturing processes and closed-loop production systems to meet sustainability targets. Diversifying product portfolios, entering new end-use sectors, and optimizing supply chains enhance operational efficiency and resilience..

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Manufacturing Process

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand in electronics and semiconductor packaging applications

- 3.2.1.2 Expansion of EVs and advanced driver-assistance systems (ADAS) adoption

- 3.2.1.3 Increased use in aerospace components for thermal and wear resistance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High processing costs and expensive raw material sourcing

- 3.2.3 Market opportunities

- 3.2.3.1 Ceramic use in solid-state battery technologies

- 3.2.3.2 Growing infrastructure for 5G and RF technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Material type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Alumina ceramics (Al2O3)

- 5.2.1 High-purity alumina (>99.5% Al2O3)

- 5.2.2 Standard alumina (95-99% Al2O3)

- 5.3 Silicon carbide ceramics (SiC)

- 5.3.1 Reaction bonded silicon carbide (RBSC)

- 5.3.2 Sintered silicon carbide (SSiC)

- 5.3.3 Hot pressed silicon carbide (HPSiC)

- 5.3.4 Others

- 5.4 Zirconia ceramics (ZrO2)

- 5.4.1 Yttria-stabilized zirconia (YSZ)

- 5.4.2 Magnesia-stabilized zirconia (MSZ)

- 5.4.3 Ceria-stabilized zirconia (CSZ)

- 5.4.4 Others

- 5.5 Silicon nitride ceramics (Si2N3)

- 5.5.1 Reaction bonded silicon nitride (RBSN)

- 5.5.2 Hot pressed silicon nitride (HPSN)

- 5.5.3 Others

- 5.6 Titanium carbide

- 5.7 Boron carbide

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Manufacturing Process, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dry pressing

- 6.3 Sintering

- 6.4 Isostatic pressing (CIP/HIP)

- 6.5 Injection molding

- 6.6 Extrusion and forming

- 6.7 Additive manufacturing / 3D printing

- 6.8 Tape casting

- 6.9 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Electronics and semiconductors

- 7.2.1 Semiconductor manufacturing equipment

- 7.2.2 Electronic substrates and packages

- 7.2.3 Capacitors and resistors

- 7.2.4 5G and RF applications

- 7.2.5 Others

- 7.3 Automotive applications

- 7.3.1 Engine components and thermal management

- 7.3.2 Electric vehicle power electronics

- 7.3.3 Sensors and emission control

- 7.3.4 Brake systems and wear parts

- 7.3.5 Others

- 7.4 Aerospace and defense

- 7.4.1 Thermal barrier coatings

- 7.4.2 Ceramic matrix composites (CMCs)

- 7.4.3 Armor and ballistic protection

- 7.4.4 Others

- 7.5 Medical and biomedical

- 7.5.1 Orthopedic implants

- 7.5.2 Dental applications

- 7.5.3 Surgical instruments

- 7.5.4 Others

- 7.6 Energy and power generation

- 7.6.1 Fuel cells and batteries

- 7.6.2 Solar energy applications

- 7.6.3 Nuclear applications

- 7.6.4 Others

- 7.7 Industrial and manufacturing

- 7.7.1 Cutting tools and wear parts

- 7.7.2 Chemical processing equipment

- 7.7.3 Refractory applications

- 7.7.4 Others

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Kyocera Corporation

- 9.2 CoorsTek Inc.

- 9.3 3M

- 9.4 CeramTec GmbH

- 9.5 Morgan Advanced Materials

- 9.6 Saint-Gobain Performance Ceramics

- 9.7 Rauschert GmbH

- 9.8 McDanel Advanced Ceramic Technologies

- 9.9 Elan Technology

- 9.10 Ferrotec (USA) Corporation

- 9.11 Advanced Ceramic Materials (ACM) Corporation

- 9.12 Blasch Precision Ceramics, Inc.

- 9.13 Momentive Technologies

- 9.14 MARUWA Co., Ltd

- 9.15 Superior Technical Ceramics

- 9.16 Schunk Group

- 9.17 NTK CERATEC CO., LTD.

- 9.18 Tosoh Corporation

- 9.19 Murata Manufacturing Co., Ltd.

- 9.20 Carborundum Universal Limited (CUMI)