PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038422

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038422

Europe Heavy Duty Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

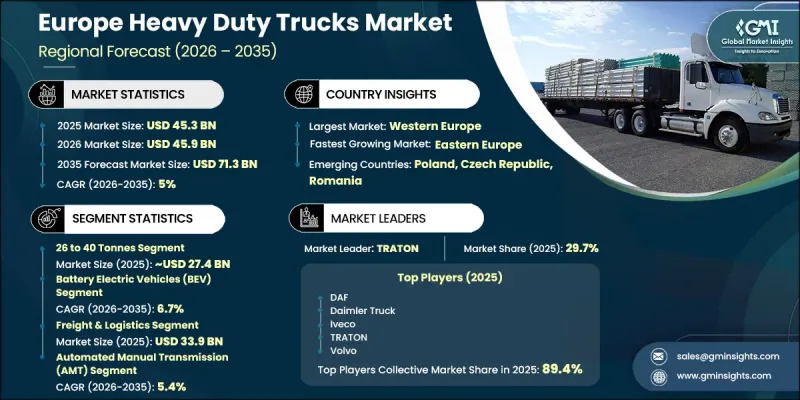

Europe Heavy Duty Trucks Market was valued at USD 35.9 billion in 2025 and is estimated to grow at a CAGR of 4.5% to reach USD 53.4 billion by 2035.

Several factors are driving this growth, including stricter emission regulations, increasing demand for electric trucks, and efforts to make freight transportation more sustainable. As technology advances, modern heavy-duty trucks are incorporating features such as telematics, Advanced Driver Assistance Systems (ADAS), and automation, which improve fleet management and safety. Companies are aligning their product offerings with the latest regulatory guidelines and consumer needs, pushing forward innovation in the market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $35.9 Billion |

| Forecast Value | $53.4 Billion |

| CAGR | 4.5% |

The Europe market is also influenced by government incentives and infrastructure investments. Many countries in the EU are focused on building hydrogen stations and EV charging networks to help commercial vehicles meet low-emission targets. Subsidies for electric trucks, along with benefits like free navigation rights and exemptions from emission zones in cities, are encouraging fleet operators to adopt these newer vehicles. With the rise of e-commerce and the demand for long-distance freight transport, there is a growing need for trucks that are both efficient and environmentally friendly. These developments are accelerated by collaborations between governments, truck manufacturers, and technology firms to enhance route design, maintenance, and communication between vehicles and road infrastructure.

The 26 to 40 tonnes segment held 60.4% share, generating USD 21.7 billion in 2025. Trucks within this weight class typically include tractor-trailer configurations designed for both long-haul and regional transport operations. These vehicles are widely recognized for optimizing payload efficiency while maintaining balanced fuel consumption, all while adhering to European Union highway regulations. Their widespread use spans multiple industries due to their operational versatility. European road infrastructure is structured around standardized axle load limits, making this weight range particularly well-suited for cross-border freight movement. As a result, these trucks maximize cargo capacity without encountering regulatory or infrastructure-related restrictions across EU member states.

The freight and logistics segment generated USD 26.9 billion in 2025. This segment holds a dominant position in the Europe heavy-duty truck market, supported by strong demand for long-haul transportation and well-established regional distribution networks that underpin national supply chains. Within this space, consistent and route-based delivery operations present a favorable opportunity for battery electric vehicle adoption, as fixed routes allow for efficient charging infrastructure deployment at centralized hubs without disrupting operational timelines.

Germany Heavy-Duty Truck Market reached USD 4.5 billion in 2025 and is expected to grow at a CAGR of 3.2% between 2026 and 2035. Market performance has been influenced by a slowdown in freight activity, rising borrowing costs, and delayed purchasing decisions for new vehicles. Uncertainty surrounding evolving electric vehicle regulations across Europe has also contributed to cautious investment behavior. Despite the implementation of emissions standards and infrastructure initiatives, diesel-powered trucks continue to dominate the market. Electrification remains primarily concentrated in short-distance and regional transport, with limited adoption observed in long-haul operations.

Key players in the Europe Heavy Duty Trucks Market include Daimler Truck, DAF Trucks, IVECO, Volvo, Ford, Nikola IVECO, Hyundai Motor, Foton Motor, and DAEWOO. To strengthen their position in the European heavy-duty truck market, companies are focusing on several strategic approaches. First, they are heavily investing in research and development to meet stringent emission regulations and align with growing consumer demands for environmentally friendly solutions. Additionally, partnerships between truck manufacturers and governments are vital for advancing infrastructure and providing incentives for electric truck adoption. Companies are also focusing on enhancing their fleet management systems with telematics and automation to improve efficiency and safety. To stay competitive, manufacturers are innovating by integrating advanced technologies such as ADAS and IoT, offering features that improve route optimization, maintenance schedules, and real-time vehicle diagnostics.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Class

- 2.2.3 Tonnage Capacity

- 2.2.4 Propulsion

- 2.2.5 Axle

- 2.2.6 Horsepower

- 2.2.7 Transmission

- 2.2.8 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent CO2 emissions regulations driving fleet modernization

- 3.2.1.2 E-commerce growth fueling demand for freight transportation

- 3.2.1.3 Total cost of ownership benefits of electric and alternative fuel trucks

- 3.2.1.4 Infrastructure investment in pan-European transport corridors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Battery range limitations for long-haul operations

- 3.2.2.2 Limited charging and refueling infrastructure in Eastern Europe

- 3.2.3 Market opportunities

- 3.2.3.1 Retrofit and conversion market for existing ICE fleets

- 3.2.3.2 Battery-as-a-Service and Truck-as-a-Service business models

- 3.2.3.3 Hydrogen fuel cell truck adoption in heavy-haul segments

- 3.2.1 Growth drivers

- 3.3 Technology and innovation landscape

- 3.3.1 Current technological trends

- 3.3.1.1 Diesel Internal Combustion Engines (ICE)

- 3.3.1.2 Automated Manual Transmission (AMT) Systems

- 3.3.1.3 Telematics & Fleet Management Systems

- 3.3.1.4 Advanced Driver Assistance Systems (ADAS)

- 3.3.2 Emerging technologies

- 3.3.2.1 Battery Electric Powertrains (BEV Trucks)

- 3.3.2.2 Autonomous Trucking & Platooning Systems

- 3.3.2.3 Hydrogen Fuel Cell Powertrains (FCEV Trucks)

- 3.3.1 Current technological trends

- 3.4 Growth potential analysis

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 Western Europe

- 3.6.1.1 Germany - Kraftfahrt-Bundesamt (KBA)

- 3.6.1.2 France - France Transport Directorate

- 3.6.1.3 Netherlands - Netherlands Vehicle Authority

- 3.6.2 Eastern Europe

- 3.6.2.1 Poland - General Inspectorate of Road Transport (GITD)

- 3.6.2.2 Czech Republic - Ministry of Transport

- 3.6.2.3 Slovakia - Ministry of Transport and Construction

- 3.6.3 Northern Europe

- 3.6.3.1 Sweden - Sweden Transport Agency

- 3.6.3.2 Norway - Public Roads Administration

- 3.6.3.3 Estonia - Estonian Transport Administration

- 3.6.4 Southern Europe

- 3.6.4.1 Italy - Ministry of Infrastructure and Transport

- 3.6.4.2 Spain - Direccion General de Trafico (DGT)

- 3.6.4.3 Portugal - Instituto da Mobilidade e dos Transportes (IMT)

- 3.6.1 Western Europe

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Trade Data Analysis (Driven by Paid Database)

- 3.9.1 Import/Export Volume & Value Trends

- 3.9.2 Key Trade Corridors & Tariff Impact

- 3.10 Capacity & Production Landscape (Driven by Primary Research)

- 3.10.1 Installed Capacity by Region & Key Producer

- 3.10.2 Capacity Utilization Rates & Expansion Pipelines

- 3.11 Cost breakdown analysis

- 3.11.1 Raw Material Procurement Costs

- 3.11.2 Manufacturing & Assembly Costs

- 3.11.3 Powertrain & Component Costs

- 3.11.4 Quality Control, Testing & Compliance Costs

- 3.12 Patent analysis (Driven by Primary Research)

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable Practices

- 3.13.2 Waste Reduction Strategies

- 3.13.3 Energy Efficiency in Production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon Footprint Considerations

- 3.14 Charging & Refueling Infrastructure Development

- 3.14.1 Public Charging Network Coverage & Density by Country

- 3.14.2 Megawatt Charging System (MCS) Deployment Status

- 3.14.3 Depot Charging Infrastructure Investment Trends

- 3.14.4 Hydrogen Refueling Station Network Development

- 3.15 Impact of AI & generative AI on the market

- 3.15.1 AI-driven disruption of existing business models

- 3.15.2 GenAI use cases & adoption roadmap by segment

- 3.15.3 Risks, limitations & regulatory considerations

- 3.16 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.16.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.16.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Western Europe

- 4.2.2 Eastern Europe

- 4.2.3 Northern Europe

- 4.2.4 Southern Europe

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company Tier Benchmarking

- 4.6.1 Tier Classification Criteria & Qualifying Thresholds

- 4.6.2 Tier Positioning Matrix by Revenue, Geography & Innovation

Chapter 5 Market Estimates and Forecast, By Class, 2022 - 2035 ($ Million, Units)

- 5.1 Key trends

- 5.2 Class 7

- 5.3 Class 8

Chapter 6 Market Estimates and Forecast, By Tonnage Capacity, 2022 - 2035 ($ Million, Units)

- 6.1 Key trends

- 6.2 16 to 26 tones

- 6.3 26 to 40 tones

- 6.4 Above 40 tones

Chapter 7 Market Estimates and Forecast, By Propulsion, 2022 - 2035 ($ Million, Units)

- 7.1 Key trends

- 7.2 Diesel

- 7.3 Battery Electric Vehicles (BEV)

- 7.4 Hybrid & Plug-in Hybrid Electric Vehicles (HEV/PHEV)

- 7.5 Fuel Cell Electric Vehicles (FCEV)

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Axle, 2022 - 2035 ($ Million, Units)

- 8.1 Key trends

- 8.2 4x2

- 8.3 6x2

- 8.4 6x4

- 8.5 6x6

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Horsepower, 2022 - 2035 ($ Million, Units)

- 9.1 Key trends

- 9.2 Below 300HP

- 9.3 300HP - 400HP

- 9.4 400HP - 500HP

- 9.5 500HP & Above

Chapter 10 Market Estimates and Forecast, By Transmission, 2022 - 2035 ($ Million, Units)

- 10.1 Key trends

- 10.2 Manual transmission

- 10.3 Automatic transmission

- 10.4 Automated Manual Transmission (AMT)

Chapter 11 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Million, Units)

- 11.1 Key trends

- 11.2 Freight & Logistics

- 11.3 Construction & Mining

- 11.4 Utility Services

- 11.5 Others

Chapter 12 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Million, Units)

- 12.1 Key trends

- 12.2 Western Europe

- 12.2.1 Germany

- 12.2.2 France

- 12.2.3 Netherlands

- 12.2.4 Belgium

- 12.2.5 Switzerland

- 12.2.6 Austria

- 12.2.7 Rest of Western Europe

- 12.3 Eastern Europe

- 12.3.1 Poland

- 12.3.2 Czech Republic

- 12.3.3 Portugal

- 12.3.4 Slovakia

- 12.3.5 Romania

- 12.3.6 Rest of Eastern Europe

- 12.4 Northern Europe

- 12.4.1 UK

- 12.4.2 Denmark

- 12.4.3 Sweden

- 12.4.4 Norway

- 12.4.5 Iceland

- 12.4.6 Rest of Northern Europe

- 12.5 Southern Europe

- 12.5.1 Italy

- 12.5.2 Spain

- 12.5.3 Greece

- 12.5.4 Rest of Southern Europe

Chapter 13 Company Profiles

- 13.1 Global players

- 13.1.1 Daimler Truck

- 13.1.2 Volvo

- 13.1.3 TRATON

- 13.1.4 Iveco Group

- 13.1.5 DAF Trucks

- 13.1.6 Ford Trucks

- 13.1.7 TATRA Trucks

- 13.1.8 BYD

- 13.1.9 SANY

- 13.1.10 Sinotruk

- 13.1.11 Hyundai Motor

- 13.1.12 Isuzu Motors

- 13.1.13 Dongfeng Motor

- 13.1.14 Hino Motors

- 13.2 Regional players

- 13.2.1 GINAF Trucks

- 13.2.2 BMC Automotive

- 13.2.3 Kamaz

- 13.2.4 Sisu Auto

- 13.3 Emerging players

- 13.3.1 Einride

- 13.3.2 Windrose