PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038448

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038448

Class 3 Truck Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

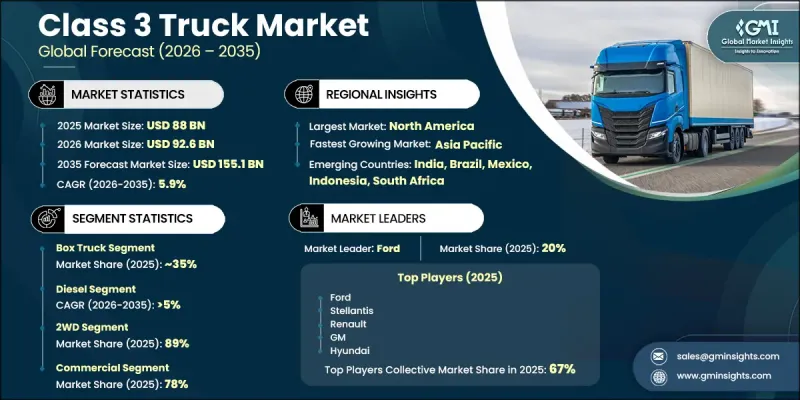

The Global Class 3 Truck Market was valued at USD 88 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 155.1 billion by 2035.

Growth is supported by the rapid evolution of digital retail channels and the increasing need for efficient distribution systems, which are driving higher demand for medium-duty vehicles. These trucks offer a balanced combination of payload capacity, maneuverability, and operational efficiency, making them well-suited for urban logistics and fleet optimization. Rising regulatory pressure on emissions is also accelerating the shift toward cleaner and alternative-fuel vehicle options, while continuous advancements in vehicle technologies are improving performance and sustainability. Additionally, expanding infrastructure projects across urban and semi-urban regions are contributing to market demand, as these vehicles are widely utilized for transportation and operational support. Their adaptability across logistics, construction, and service applications reinforces their importance in modern transportation networks. As industries continue to prioritize efficiency and environmental compliance, the Class 3 truck market is positioned for consistent long-term growth supported by evolving mobility and logistics requirements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $88 Billion |

| Forecast Value | $155.1 Billion |

| CAGR | 5.9% |

The box truck segment held a 35% share in 2025 and is expected to grow at a CAGR of 6% between 2026 and 2035. Growth in this segment is closely linked to the expansion of organized retail distribution, as enclosed vehicle structures provide enhanced protection and efficiency for transporting goods across urban routes.

The diesel-powered vehicles segment accounted for 66.3% share in 2025 and is projected to grow at a CAGR of 5% through 2035. Their strong torque output, higher payload capability, and operational reliability continue to support widespread adoption across demanding applications. Established fueling infrastructure further strengthens their position by ensuring uninterrupted fleet operations across regions.

United States Class 3 Truck Market held 90% share, generating USD 28.8 billion in 2025. Market expansion is supported by advanced logistics networks, increasing demand for rapid delivery services, and continuous investments in vehicle innovation. Strong manufacturing capabilities and ongoing technological advancements further enable the market to meet rising demand efficiently.

Key companies operating in the Global Class 3 Truck Industry include Toyota, Ford, Isuzu, Hyundai, Volkswagen, Renault, GM, Nissan, IVECO, and Stellantis. Companies in the Class 3 Truck Market are focusing on innovation, sustainability, and strategic expansion to strengthen their competitive position. Manufacturers are investing in alternative fuel technologies and electrification to comply with evolving emission standards while improving vehicle efficiency. Product development efforts emphasize enhanced payload capacity, durability, and advanced safety features to meet diverse operational requirements. Partnerships with logistics providers and fleet operators are helping companies expand their customer base and improve market penetration. Firms are also optimizing production processes and supply chains to reduce costs and improve delivery timelines. In addition, expanding presence in emerging markets and strengthening after-sales services are key strategies used to build long-term customer relationships and reinforce brand positioning.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Propulsion

- 2.2.3 Drive Configuration

- 2.2.4 End Use

- 2.2.5 Application

- 2.2.6 Vehicle

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in last-mile delivery and e-commerce logistics

- 3.2.1.2 Electrification of medium-duty trucks

- 3.2.1.3 Expansion of construction and infrastructure activities

- 3.2.1.4 Fleet modernization and telematics integration

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High upfront cost of electric and advanced trucks

- 3.2.2.2 Supply chain disruptions and component shortages

- 3.2.2.3 Limited charging and refueling infrastructure

- 3.2.2.4 Driver shortages and operational inefficiencies

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in emerging markets

- 3.2.3.2 Development of alternative fuel trucks (CNG, hydrogen)

- 3.2.3.3 Expansion of cold chain and specialized logistics

- 3.2.3.4 Rise of leasing and fleet-as-a-service models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Environmental protection agency (EPA)

- 3.4.1.2 National highway traffic safety administration (NHTSA) - FMVSS 500

- 3.4.1.3 Occupational safety and health administration (OSHA)

- 3.4.1.4 Canadian motor vehicle safety standards (CMVSS)

- 3.4.1.5 State-level road use regulations

- 3.4.2 Europe

- 3.4.2.1 EU machinery directive

- 3.4.2.2 CE marking compliance

- 3.4.2.3 Low voltage directive (LVD)

- 3.4.2.4 Electromagnetic compatibility (EMC) directive

- 3.4.2.5 National road homologation requirements

- 3.4.3 Asia Pacific

- 3.4.3.1 Chinese EV and LSV regulatory framework

- 3.4.3.2 Indian central motor vehicle rules (CMVR)

- 3.4.3.3 Japanese road transport vehicle act

- 3.4.3.4 ASEAN EV policy harmonization efforts

- 3.4.3.5 Australian design rules (ADR)

- 3.4.4 Latin America

- 3.4.4.1 Brazilian national traffic council (CONTRAN) regulations

- 3.4.4.2 Mexican NOM standards

- 3.4.4.3 Regional urban mobility and EV incentive programs

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC vehicle compliance and type approval regulations

- 3.4.5.2 South African national road traffic act (NRTA)

- 3.4.5.3 Tourism and free-zone operational standards

- 3.4.1 North America

- 3.5 Major market trends and disruptions

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price analysis (Driven by Primary Research)

- 3.10.1 Historical Price Trend Analysis

- 3.10.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.11 Trade data analysis (Driven by Paid Research)

- 3.11.1 Import/export volume & value trends

- 3.11.2 Key trade corridors & tariff impact

- 3.12 Cost breakdown analysis

- 3.13 Patent analysis (Driven by Primary Research)

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Impact of AI & generative AI on the market

- 3.15.1 AI-driven disruption of existing business models

- 3.15.2 GenAI use cases & adoption roadmap by segment

- 3.15.3 Risks, limitations & regulatory considerations

- 3.16 Capacity & production landscape (Driven by Primary Research)

- 3.16.1 Installed capacity by region & key producer

- 3.16.2 Capacity utilization rates & expansion pipelines

- 3.17 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.17.1 Base Case - key macro & industry variables driving CAGR

- 3.17.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.17.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Gasoline

- 5.3 Diesel

- 5.4 Hybrid

- 5.5 Electric

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Drive Configuration, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 2WD

- 6.3 AWD

Chapter 7 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Last-mile delivery & logistics

- 7.3 Utility & municipal services

- 7.4 Construction & infrastructure support

- 7.5 Field services & maintenance

- 7.6 Refrigerated transport / specialized logistics

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Industrial

- 8.3 Commercial

Chapter 9 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Walk-in trucks

- 9.3 Box trucks

- 9.4 City delivery trucks

- 9.5 Heavy-duty pickup trucks

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Southeast Asia

- 10.4.6 ANZ

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Argentina

- 10.5.3 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Ford

- 11.1.2 GM

- 11.1.3 Hyundai

- 11.1.4 IVECO

- 11.1.5 Nissan

- 11.1.6 Renault

- 11.1.7 Stellantis

- 11.1.8 Toyota

- 11.1.9 Volkswagen

- 11.2 Regional Players

- 11.2.1 Isuzu

- 11.2.2 Ashok Leyland

- 11.2.3 Fuso

- 11.2.4 Hino

- 11.2.5 Mahindra

- 11.2.6 Tata

- 11.3 Emerging Players

- 11.3.1 Dongfeng

- 11.3.2 Foton

- 11.3.3 JAC

- 11.3.4 Kia

- 11.3.5 SAIC