PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038452

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038452

Electric Construction Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

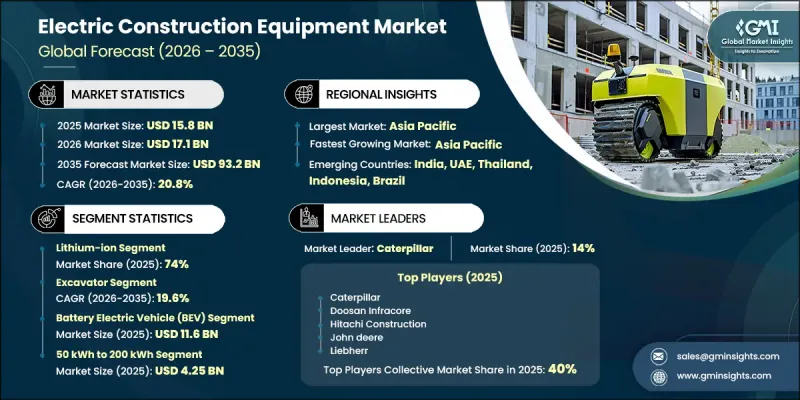

The Global Electric Construction Equipment Market was valued at USD 15.8 billion in 2025 and is estimated to grow at a CAGR of 20.8% to reach USD 93.2 billion by 2035.

Growth is driven by stricter environmental regulations, increasing financial incentives, and the long-term cost advantages associated with reduced fuel consumption and maintenance requirements. The construction sector is increasingly adopting electrified machinery to align with sustainability goals and improve operational efficiency. Technological advancements such as fast-charging systems, battery-swapping capabilities, and digital monitoring solutions are enhancing equipment performance and usability. In addition, the integration of connected technologies is enabling better equipment management and predictive maintenance. Asia-Pacific is expected to lead the market due to extensive infrastructure development and strong policy support for electrification. Continuous innovation in electric machinery and increasing investment in clean construction technologies are further strengthening the market outlook, positioning electric construction equipment as a key component of future infrastructure development.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $15.8 Billion |

| Forecast Value | $93.2 Billion |

| CAGR | 20.8% |

The electric construction equipment market is also benefiting from the growing demand for advanced and efficient machinery that supports modern construction requirements. Increasing focus on reducing emissions and improving operational productivity is encouraging the adoption of electrified equipment across job sites. Economic growth in North America is further supporting market expansion, driven by stricter emission standards and a growing emphasis on sustainable construction practices. Financial incentives aimed at reducing the high initial cost of electric equipment are also contributing to increased adoption.

The lithium-ion segment held a 74% share in 2025 and is expected to grow at a CAGR of 21% through 2035. This dominance is attributed to the increasing need for high-performance energy storage solutions that offer longer operational life and faster charging capabilities. These batteries play a critical role in enhancing the efficiency and reliability of both heavy-duty and compact electric construction equipment.

The excavator segment accounted for 57% share in 2025 and is projected to grow at a CAGR of 19.6% from 2026 to 2035. Demand for electric excavators is rising due to their flexibility and suitability for a wide range of construction activities. Their ability to operate with lower noise levels and reduced environmental impact further supports adoption, particularly in urban and infrastructure development projects.

China Electric Construction Equipment Market generated USD 2.47 billion in 2025. The country's strong position is supported by rapid urbanization, large-scale infrastructure investments, and increasing adoption of environmentally sustainable construction machinery. Government initiatives aimed at promoting clean energy and reducing emissions are further strengthening market growth, reinforcing China's leadership in the regional landscape.

Key companies operating in the Global Electric Construction Equipment Market include Komatsu, Caterpillar, Volvo Construction Equipment, Hitachi Construction Machinery, JCB, Liebherr, Hyundai Construction Equipment, Doosan Infracore, CNH Industrial, John Deere, and Kubota. Companies in the Electric Construction Equipment Market are focusing on innovation, electrification strategies, and strategic partnerships to strengthen their market position. They are investing in advanced battery technologies and energy management systems to improve performance and efficiency. Many players are expanding their product portfolios with fully electric and hybrid equipment to meet evolving regulatory and customer demands. Strategic collaborations with technology providers are enabling the integration of digital solutions such as remote monitoring and predictive maintenance. Additionally, companies are increasing production capacity and strengthening supply chains to support rising demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment

- 2.2.3 Battery Capacity

- 2.2.4 Battery Technology

- 2.2.5 End-User

- 2.2.6 Power Source

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component manufacturers

- 3.1.1.3 Battery manufacturers

- 3.1.1.4 Equipment manufacturers

- 3.1.1.5 Distributors and dealers

- 3.1.1.6 Aftermarket suppliers

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent emission regulations

- 3.2.1.2 Declining battery costs

- 3.2.1.3 Urbanization & infrastructure development

- 3.2.1.4 Advancements in battery & powertrain technology

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High upfront cost of electric equipment

- 3.2.2.2 Limited charging infrastructure

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in BEV and hybrid fleet transition

- 3.2.3.2 Integration of telematics & smart fleet management

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.2 Emerging technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 Inflation Reduction Act

- 3.5.1.2 Clean Air Act

- 3.5.2 Europe

- 3.5.2.1 European Green Deal

- 3.5.2.2 Euro 7 Emission Standards

- 3.5.3 Asia-Pacific

- 3.5.3.1 New Energy Vehicle (NEV) Credit Policy

- 3.5.3.2 Automotive Industry Standard (AIS) 156

- 3.5.4 Latin America

- 3.5.4.1 Programa Rota 2030

- 3.5.4.2 Mexican NOM Emissions Standards

- 3.5.5 Middle East & Africa

- 3.5.5.1 UAE Net Zero 2050 Strategy

- 3.5.5.2 South Africa Green Transport Strategy

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type

- 3.10 Capacity & Production Landscape (Driven by Primary Research)

- 3.10.1 Installed Capacity by Region & Key Producer

- 3.10.2 Capacity Utilization Rates & Expansion Pipelines

- 3.11 Trade Data Analysis (Driven by Paid Database)

- 3.11.1 Import/Export Volume & Value Trends

- 3.11.2 Key Trade Corridors & Tariff Impact

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Impact of AI & generative AI on the market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Equipment, 2022 - 2035 ($ Bn, Units)

- 5.1 Key trends

- 5.2 Excavators

- 5.3 Loaders

- 5.4 Bulldozers

- 5.5 Cranes

- 5.6 Dump Trucks

- 5.7 Roller

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Battery Capacity , 2022 - 2035 ($ Bn, Units)

- 6.1 Key trends

- 6.2 Less than 50 kWh

- 6.3 50 kWh to 200 kWh

- 6.4 More than 200 kWh

Chapter 7 Market Estimates & Forecast, By Battery Technology, 2022 - 2035 ($ Bn, Units)

- 7.1 Key trends

- 7.2 Lead-acid

- 7.3 Lithium-ion

- 7.4 Nickel-metal hydride

Chapter 8 Market Estimates & Forecast, By End-User, 2022 - 2035 ($ Bn, Units)

- 8.1 Key trends

- 8.2 Construction

- 8.3 Mining

- 8.4 Material Handling

- 8.5 Agriculture

- 8.6 Others

Chapter 9 Market Estimates & Forecast By Power Source, 2022 - 2035 ($ Bn, Units)

- 9.1 Key trends

- 9.2 Battery Electric Vehicles (BEV)

- 9.3 Plug-in Hybrid Electric Vehicles (PHEV)

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Caterpillar

- 11.1.2 CNH Industrial

- 11.1.3 Hitachi Construction Machinery

- 11.1.4 JCB

- 11.1.5 John Deere

- 11.1.6 Komatsu

- 11.1.7 Kubota

- 11.1.8 Liebherr

- 11.1.9 Sandvik

- 11.2 Regional players

- 11.2.1 Develon

- 11.2.2 Doosan Infracore

- 11.2.3 Hyundai Construction Equipment

- 11.2.4 LiuGong Machinery

- 11.2.5 Manitou

- 11.2.6 Mecalac

- 11.2.7 SDLG

- 11.3 Emerging players

- 11.3.1 Avant Tecno Oy

- 11.3.2 Kramer-Werke

- 11.3.3 Sunward Intelligent Equipment

- 11.3.4 Zoomlion Heavy Industry Science & Technology