PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038460

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038460

Security Labels Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

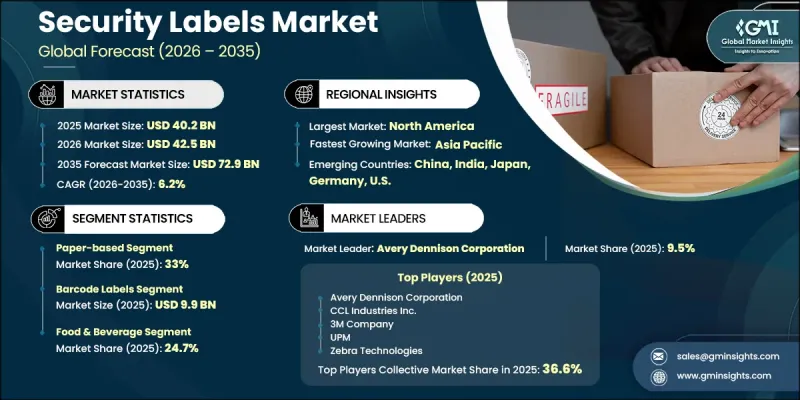

The Global Security Labels Market was valued at USD 40.2 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 72.9 billion by 2035.

The security labeling industry is gaining strong momentum as organizations increasingly prioritize product authentication, supply chain transparency, and brand protection. Regulatory pressure surrounding traceability and anti-counterfeiting measures plays a central role in shaping market demand, particularly across sensitive industries where product integrity is critical. The adoption of advanced labeling technologies, including digitally enabled solutions, is accelerating as businesses aim to improve tracking accuracy and operational visibility. Growing reliance on tamper-evident packaging within expanding logistics and distribution networks is further strengthening the need for reliable labeling systems. At the same time, rising concerns around counterfeit goods and unauthorized duplication are encouraging companies to invest in more sophisticated security features. The integration of intelligent labeling formats and covert identification technologies is becoming increasingly important, enabling enhanced verification capabilities while maintaining operational efficiency. Continuous innovation in labeling materials and technologies is supporting long-term market expansion by aligning with evolving compliance standards and industry requirements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $40.2 Billion |

| Forecast Value | $72.9 Billion |

| CAGR | 6.2% |

The paper-based security labels segment accounted for a 33% share in 2025, supported by their affordability, ease of production, and compatibility with large-scale printing systems. These labels are widely utilized due to their adaptability in high-volume environments and their ability to support various identification and security applications. Their alignment with sustainability goals, including recyclability and reduced environmental impact, further strengthens their widespread adoption. The scalability of paper-based solutions makes them a preferred choice for industries requiring cost-efficient yet effective labeling systems.

The barcode labels segment generated USD 9.9 billion in 2025, maintaining a leading position due to their reliability and widespread integration into tracking and identification systems. Their simplicity, cost efficiency, and seamless compatibility with existing scanning technologies make them a practical solution for managing large-scale operations. The steady growth of organized distribution networks and global trade activities continues to drive the demand for barcode-based solutions, ensuring their ongoing relevance in modern supply chain ecosystems.

North America Security Labels Market held 35.2% share in 2025, driven by strict regulatory frameworks and a high focus on product authentication and compliance. The region is witnessing increasing deployment of advanced labeling technologies that enhance traceability and operational transparency. Strong investment in digital tracking systems and secure labeling infrastructure is contributing to sustained growth. The demand is further supported by the need to maintain product integrity and ensure efficient monitoring across complex supply chains, positioning the region as a leader in technological advancement within the security labels industry.

Key companies operating in the Global Security Labels Market include 3M Company, Avery Dennison Corporation, CCL Industries Inc., Zebra Technologies, Brady Corporation, Sato Holdings, UPM, Tesa SE Group, Authentix Inc., Holostik India Limited, Uflex Limited, SICPA, IMS Brand Protection, Laser Printing Industries, Shosky Security, and Holographic Label Sdn Bhd. Companies in the Security Labels Market are focusing on strengthening their competitive position through continuous innovation in smart and secure labeling technologies. Investments in research and development are enabling the creation of advanced features that improve traceability, authentication, and product protection. Market participants are expanding their global footprint through partnerships, acquisitions, and distribution network enhancements to reach broader customer bases. Emphasis on sustainability is encouraging the development of eco-friendly materials and recyclable label solutions. Firms are also leveraging digital integration and data-driven systems to enhance supply chain visibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Material trends

- 2.2.3 Application trends

- 2.2.4 End-use industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pharmaceutical serialization and track-and-trace mandates

- 3.2.1.2 Increasing counterfeit incidents in luxury and electronics sectors

- 3.2.1.3 Growth in e-commerce requiring tamper-evident packaging solutions

- 3.2.1.4 Adoption of RFID-enabled labels for supply chain visibility

- 3.2.1.5 Integration of smart authentication technologies (QR, NFC)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation cost of advanced security label technologies

- 3.2.2.2 Complex integration with existing packaging lines

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in blockchain-based product authentication solutions

- 3.2.3.2 Expansion in emerging markets with weak anti-counterfeit infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Barcode labels

- 5.3 Holographic labels

- 5.4 Radio frequency identification (RFID) labels

- 5.5 Electronic article surveillance (EAS) labels

- 5.6 Near field communication (NFC) labels

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Paper-based

- 6.3 Polymer-based

- 6.4 Metal-based

- 6.5 Fabric labels

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Bottles & jars

- 7.3 Boxes & cartons

- 7.4 Bags & pouches

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.3 Healthcare & pharmaceutical

- 8.4 Chemicals & fertilizers

- 8.5 Consumer goods

- 8.6 Automotive

- 8.7 Retail

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 3M Company

- 10.1.2 Avery Dennison Corporation

- 10.1.3 CCL Industries Inc.

- 10.1.4 UPM

- 10.1.5 Zebra Technologies

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Brady Corporation

- 10.2.1.2 Authentix Inc.

- 10.2.2 Asia Pacific

- 10.2.2.1 Uflex Limited

- 10.2.2.2 Sato Holdings

- 10.2.2.3 Holostik India Limited

- 10.2.2.4 Holographic Label Sdn Bhd

- 10.2.3 Europe

- 10.2.3.1 Tesa SE Group

- 10.2.3.2 SICPA

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 IMS Brand Protection

- 10.3.2 Laser Printing Industries

- 10.3.3 Shosky Security