PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038481

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038481

Polyolefin Powders Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

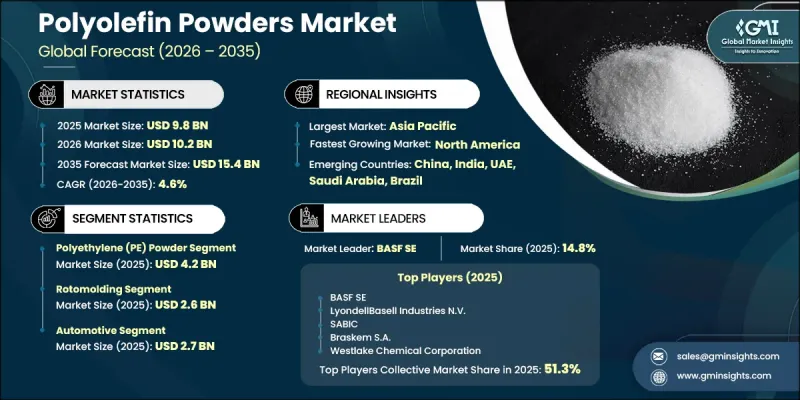

The Global Polyolefin Powders Market was valued at USD 9.8 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 15.4 billion in 2035.

Polyolefin powders are finely milled polymer particles derived mainly from polyethylene (PE), polypropylene (PP), and ethylene propylene diene monomer (EPDM), produced through grinding, precipitation, or emulsion-based processes. These materials are widely recognized for their chemical resistance, low moisture uptake, thermal stability, and processing convenience, which make them suitable for applications such as rotomolding, powder coatings, adhesives, and advanced manufacturing solutions. The market plays a crucial role in the broader polymer industry by enabling manufacturers to develop durable, flexible, and cost-efficient products with consistent performance. Their powder form supports accurate dosing, even dispersion, and improved processing efficiency compared to pellet and granular formats, which continues to support global adoption. Demand is also shaped by strong consumption across automotive, construction, and packaging sectors, where high-performance materials are essential. Advanced manufacturing economies depend on these powders to achieve improved product quality, sustainability objectives, and cost optimization. The industry includes both specialized producers and large-scale chemical manufacturers using grinding, cryogenic, and precipitation techniques to achieve targeted particle properties and performance consistency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.8 Billion |

| Forecast Value | $15.4 Billion |

| CAGR | 4.6% |

The polyethylene (PE) powder segment accounted for USD 4.2 billion in 2025, driven by strong versatility, affordability, and widespread use across rotomolding, coatings, adhesives, and additive manufacturing applications. The material is valued for its chemical resistance, low moisture absorption, and strong processing behavior, along with availability in multiple density grades, including LDPE and HDPE, allowing tailored use across applications. Polypropylene powders are also gaining steady traction due to higher temperature resistance, improved rigidity, and enhanced chemical stability compared to polyethylene-based alternatives.

The rotomolding segment reached USD 2.6 billion in 2025. This segment dominates consumption due to its ability to produce seamless, hollow, and structurally uniform components with consistent wall thickness. The process depends entirely on powder feedstocks, with polyethylene powders accounting for more than 90% of usage across products such as tanks, containers, playground structures, and automotive components. Successful processing requires controlled particle size distribution, stable flow characteristics, and consistent melting behavior to ensure high-quality finished parts.

North America Polyolefin Powders Market is expected to grow from USD 2.8 billion in 2025 to USD 4.3 billion by 2035. Growth in the region is supported by strong automotive manufacturing, adoption of advanced processing technologies, regulatory support for low-emission powder coating systems, and rising infrastructure development. The United States remains the key contributor, with widespread usage across rotomolding, coatings, adhesives, and additive manufacturing. The region also benefits from an integrated petrochemical base, strong polymer processing capabilities, and efficient supply chain alignment between producers and end users.

Major players operating in the Global Polyolefin Powders Industry include LyondellBasell Industries N.V., SABIC, BASF SE, Braskem S.A., Westlake Chemical Corporation, Mitsui Chemicals, Celanese Corporation, Honeywell International Inc., Clariant AG, Shamrock Technologies Inc., Micro Powders Inc., and Marcus Oil & Chemical. Companies in the polyolefin powders market are strengthening their position through capacity expansion, product innovation, and advanced polymer modification technologies. They are focusing on developing customized powder grades with improved particle uniformity, thermal resistance, and processing stability. Strategic collaborations with automotive, construction, and coatings manufacturers are supporting tailored product development. Investments in sustainable production methods, including energy-efficient processing and recyclable polymer solutions, are increasing. Firms are also expanding distribution networks to improve global supply chain efficiency while adopting digital process control systems for consistent quality assurance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Application

- 2.2.3 End use industry

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene (PE) Powder

- 5.3 Polypropylene (PP) Powder

- 5.4 Ethylene Propylene Diene Monomer (EPDM) Powder

- 5.5 Others (polybutene, polyolefin elastomers)

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Rotomolding

- 6.3 Masterbatches

- 6.4 Powder Coatings

- 6.5 Hot Melt Adhesives

- 6.6 Thermoplastic Elastomers

- 6.7 Additive Manufacturing (3D Printing)

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By End-Use Industry, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Construction

- 7.4 Packaging

- 7.5 Consumer Goods

- 7.6 Electrical & Electronics

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 Braskem S.A.

- 9.3 LyondellBasell Industries N.V.

- 9.4 SABIC

- 9.5 Westlake Chemical Corporation

- 9.6 Mitsui Chemicals

- 9.7 Celanese Corporation

- 9.8 Honeywell International Inc.

- 9.9 Clariant AG

- 9.10 Shamrock Technologies Inc.

- 9.11 Micro Powders Inc.

- 9.12 Marcus Oil & Chemical