PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038638

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038638

Membrane Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

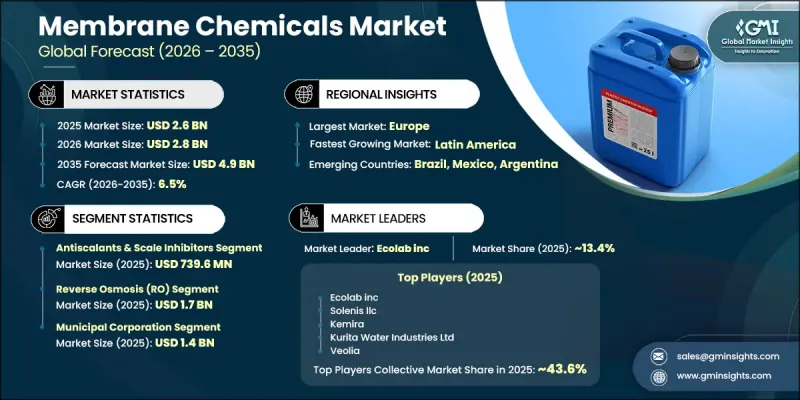

The Global Membrane Chemicals Market was valued at USD 2.6 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 4.9 billion by 2035.

The market is witnessing steady expansion as global water stress intensifies, pushing industries and municipalities toward advanced filtration and desalination technologies. Membrane-based systems rely heavily on specialized chemical treatments such as antiscalants, biocides, and cleaning agents to maintain efficiency, reduce fouling, and extend membrane lifespan. Rising investments in desalination and wastewater treatment infrastructure are significantly increasing chemical consumption across treatment facilities. Industrial sectors, including energy production, oil and gas operations, and manufacturing, are also adopting membrane systems to comply with stricter discharge regulations and improve water efficiency. Government-backed water security initiatives and recycling programs are further accelerating the deployment of membrane technologies, strengthening long-term demand for supportive chemical solutions. Continuous operation requirements and the need for system reliability ensure recurring chemical usage, creating stable revenue streams for manufacturers. Advancements in process optimization, environmental compliance, and sustainable water management practices are further reinforcing the market outlook across both developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.6 Billion |

| Forecast Value | $4.9 Billion |

| CAGR | 6.5% |

The antiscalants and scale inhibitors segment captured USD 739.6 million in 2025, due to their essential role in preventing scaling and maintaining membrane performance. These chemicals are widely used to reduce downtime and improve operational continuity in both industrial and desalination applications. Demand is further supported by the use of biocides and disinfectants to control microbial growth, along with coagulants and flocculants that assist in pretreatment processes. Additional chemical categories, such as pH regulators and dechlorination agents, are increasingly utilized to maintain optimal operating conditions and protect membrane integrity.

The reverse osmosis segment reached USD 1.7 billion in 2025, driven by its extensive use in producing high-quality water and desalination outputs. This technology depends on continuous chemical support, including antiscalants, cleaning solutions, and microbial control agents, to ensure stable and efficient operation. Growing adoption of reverse osmosis systems across municipal and industrial sectors continues to reinforce demand for membrane treatment chemicals globally.

North America Membrane Chemicals Market accounted for USD 715.3 million in 2025. The region is experiencing increased adoption of membrane-based water treatment systems due to infrastructure modernization, strict environmental regulations, and rising emphasis on water conservation. Industries are integrating advanced monitoring systems alongside high-performance chemical treatments to improve efficiency and operational control. Expanding water reuse initiatives and consistent industrial demand are further strengthening regional market expansion.

Major players operating in the Global Membrane Chemicals Industry are Kurita Water Industries Ltd, Veolia, Kemira, Ecolab Inc., Genesys, Solenis LLC, Lenntech B.V., King Lee Technologies, H2O Innovation, Universal Water Chemicals Pvt Ltd, Reverse Osmosis Chemicals International, L K Chemicals, and Thermax Limited. Key strategies adopted by companies in the Membrane Chemicals Market include expanding product portfolios with high performance and eco-friendly formulations to meet tightening environmental regulations and industry standards. Firms are heavily investing in research and development to improve antifouling, anti-scaling, and microbial control efficiency while extending membrane life cycles. Strategic collaborations with water treatment plants and industrial operators are strengthening long-term supply agreements and market penetration. Companies are also focusing on geographic expansion into water-stressed regions where desalination is rising rapidly. Digital monitoring integration and smart dosing systems are being deployed to enhance chemical efficiency and reduce operational costs. In addition, mergers, acquisitions, and partnerships help companies expand technological capabilities and strengthen global distribution networks, ensuring sustained competitiveness and long-term growth in the membrane chemicals industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Technology

- 2.2.4 End User

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for desalination in water-scarce regions

- 3.2.1.2 Increasing industrial water treatment requirements

- 3.2.1.3 Government investments in sustainable water infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High operational costs of membrane chemical treatment

- 3.2.2.2 Limited technical expertise for advanced membrane maintenance

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of Advanced Water Reuse and Zero Liquid Discharge (ZLD) Systems

- 3.2.3.2 Growing Adoption of High-Purity Water in Emerging Industries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Antiscalants & Scale Inhibitors

- 5.2.1 Phosphonates (ATMP, HEDP, PBTC)

- 5.2.2 Polycarboxylates (Polyacrylates, Polymaleates)

- 5.2.3 Fluorescent-Tagged Antiscalants

- 5.2.4 Others

- 5.3 Cleaning Chemicals

- 5.3.1 Acid Cleaners (Citric, HCl, Phosphoric, Oxalic)

- 5.3.2 Alkaline Cleaners (NaOH, KOH, Na2CO3)

- 5.3.3 Oxidizing Cleaners (NaOCl, H2O2, Peracetic Acid)

- 5.3.4 Enzymatic Cleaners (Proteases, Lipases, Amylases)

- 5.3.5 Others

- 5.4 Coagulants & Flocculants

- 5.4.1 Inorganic Coagulants (Ferric Chloride, Alum, PAC)

- 5.4.2 Organic Polymers (Cationic, Anionic, Non-ionic)

- 5.5 pH Adjusters & Buffers

- 5.5.1 Acids (H2SO4, HCl, CO2)

- 5.5.2 Bases (NaOH, Na2CO3, Lime)

- 5.6 Biocides & Disinfectants

- 5.6.1 Oxidizing Biocides

- 5.6.2 Non-oxidizing Biocides

- 5.7 Dechlorination Agents

- 5.8 Boron Removal Chemicals

- 5.8.1 Ion Exchange Resins (Boron-Selective)

- 5.8.2 Electrodeionization (Kurita KCDI-UPz)

- 5.8.3 pH Elevation Chemicals

- 5.9 Corrosion Inhibitors

- 5.9.1 Phosphate-based Inhibitors

- 5.9.2 Silicate-based Inhibitors

- 5.9.3 Organic Inhibitors (Azoles, Phosphonates)

- 5.10 Antifoaming Agents

- 5.11 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Reverse Osmosis (RO)

- 6.2.1 Seawater Reverse Osmosis (SWRO)

- 6.2.2 Brackish Water Reverse Osmosis (BWRO)

- 6.3 Thermal Desalination (MSF/MED)

- 6.4 Nanofiltration (NF)

- 6.5 Hybrid Systems (NF-RO, HPRO, OARO, FO)

- 6.6 Ultrafiltration (UF) & Microfiltration (MF)

- 6.7 Membrane Bioreactor (MBR)

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 Municipal Corporation

- 7.2.1 Seawater Desalination

- 7.2.2 Brackish Water Desalination

- 7.3 Oil & Gas Industry

- 7.3.1 Enhanced Oil Recovery (EOR)

- 7.3.2 Produced Water Treatment

- 7.3.3 Offshore Platform Water Treatment

- 7.4 Petrochemicals & Refining

- 7.5 Power Generation

- 7.6 Industrial Water Treatment

- 7.6.1 Food & Beverages

- 7.6.2 Pharmaceuticals (Purified Water, WFI)

- 7.6.3 Textiles

- 7.6.4 Mining (Phosphate)

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Kurita Water Industries Ltd

- 9.2 Genesys

- 9.3 Kemira

- 9.4 Lenntech B.V.

- 9.5 Reverse Osmosis Chemicals International

- 9.6 King Lee Technologies

- 9.7 H2O Innovation

- 9.8 Veolia

- 9.9 Universal Water Chemicals Pvt Ltd

- 9.10 L K CHEMICALS

- 9.11 Thermax Limited

- 9.12 Ecolab inc

- 9.13 Solenis llc