PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038666

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038666

Conventional Rotators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

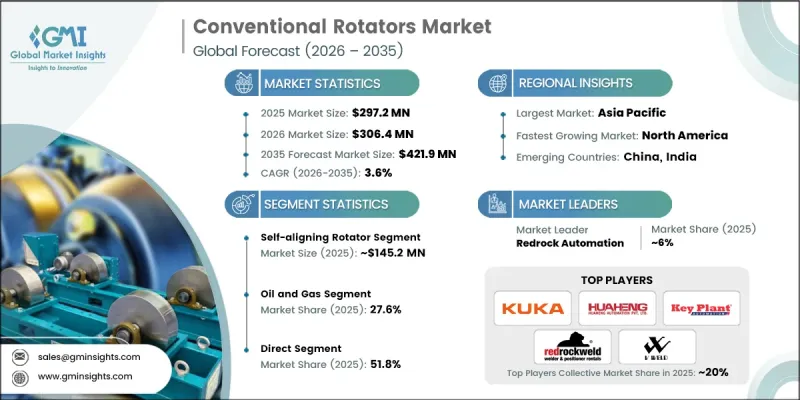

The Global Conventional Rotators Market was valued at USD 297.2 million in 2025 and is estimated to grow at a CAGR of 3.6% to reach USD 421.9 million by 2035.

Growth is driven by increasing adoption of controlled rotation systems that enhance accuracy in cylindrical welding operations and reduce structural deformation during fabrication. Industries are increasingly prioritizing high-quality weld consistency, reduced rework, and improved productivity, which is strengthening the adoption of conventional rotators. These systems enable stable positioning of heavy components, ensuring improved dimensional precision and operational efficiency. Rising focus on automation in fabrication facilities is further accelerating demand, as manufacturers aim to minimize manual intervention and optimize workflow continuity. Integration with advanced welding systems such as manipulators and automated production lines is also improving operational scalability. Additionally, ongoing industrial modernization and the need for faster turnaround times in heavy engineering projects are reinforcing market adoption across global manufacturing environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $297.2 Million |

| Forecast Value | $421.9 Million |

| CAGR | 3.6% |

The market is further influenced by the growing emphasis on streamlined fabrication processes and enhanced production efficiency across heavy engineering sectors. Manufacturers are increasingly investing in equipment that supports continuous operation, reduces handling time, and improves workplace safety. Conventional rotators are becoming essential in enabling synchronized welding operations and supporting high-volume industrial output.

The self-aligning rotator segment generated USD 145.2 million in 2025 and is expected to grow at a CAGR of 4% from 2026 to 2035. This segment remains highly significant due to its ability to automatically adjust roller positioning based on the curvature and diameter of cylindrical components. Such functionality eliminates the need for manual adjustments and improves operational precision. These systems are particularly effective in handling components with irregular shapes, uneven surfaces, or varying thickness levels, which are common in heavy fabrication environments, thereby improving workflow efficiency and weld accuracy.

The self-aligning rotator segment generated USD 145.2 million in 2025 and is expected to grow at a CAGR of 4% from 2026 to 2035. These systems are designed to automatically adapt roller angles according to the workpiece geometry, removing the need for manual calibration. Their ability to manage cylindrical parts with minor distortions or inconsistent dimensions makes them highly valuable in heavy-duty fabrication processes where precision and stability are critical for achieving consistent welding outcomes.

U.S. Conventional Rotators Market accounted for USD 74.3 million in 2025 and is projected to grow at a CAGR of 3.5% from 2026 to 2035. Market growth in the country is supported by strong demand from industrial sectors requiring high-precision welding solutions. Expanding infrastructure projects, ongoing maintenance activities in energy systems, and increased industrial fabrication requirements are supporting equipment adoption. The shift toward digitalized manufacturing and automation is also contributing to demand for advanced rotators equipped with smart monitoring and operational efficiency features. Established fabrication facilities and strict quality standards further reinforce the need for high-performance rotational welding equipment across the region.

Key companies operating in the Global Conventional Rotators Market include Cascade Corporation, KUKA Robotics, Indexator, Key Plant Automation, Huaheng Automation, Amin Machinery, Anvin Engineers, Cubuilt Engineers, Innovic Technology, Intermercato, MG Welding, Mogra Engineering, Redrock Automation, SENLISWELD, and V-Weld. Companies in the Conventional Rotators Market are focusing on automation enhancement and product performance optimization to strengthen their market position. They are investing in advanced control systems that improve precision, load handling capacity, and operational safety. Strategic partnerships with industrial fabrication firms are helping expand application reach and improve customization capabilities. Manufacturers are also emphasizing integration with automated welding systems to support continuous production workflows. Expansion of service networks and aftersales support is improving customer retention and operational reliability. Additionally, companies are prioritizing digital monitoring technologies and predictive maintenance features to enhance equipment lifespan, reduce downtime, and improve efficiency across heavy industrial welding applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Market estimates & forecasts parameters

- 1.4 Forecast Model

- 1.4.1 Key trends for market estimates

- 1.4.2 Quantified market impact analysis

- 1.4.2.1 Mathematical impact of growth parameters on forecast

- 1.4.3 Scenario analysis framework

- 1.5 Primary research and validation

- 1.5.1 Some of the primary sources (but not limited to)

- 1.6 Data mining sources

- 1.6.1 Paid Sources

- 1.7 Primary research and validation

- 1.7.1 Primary sources

- 1.8 Research Trail & confidence scoring

- 1.8.1 Research trail components

- 1.8.2 Scoring components

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Welding Types

- 2.2.4 Load Carrying Capacity

- 2.2.5 Application

- 2.2.6 End Use Industry

- 2.2.7 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component manufacturers

- 3.1.3 Rotator OEMs

- 3.1.4 Distributors & dealers

- 3.1.5 End users

- 3.1.6 After-sales service providers

- 3.1.7 Value addition at each stage

- 3.1.8 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for precision & efficiency in heavy manufacturing

- 3.2.1.2 Expansion of renewable energy projects

- 3.2.1.3 Infrastructure development in emerging economies

- 3.2.2 Pitfalls & challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Need for frequent maintenance & skilled operators

- 3.2.3 Opportunities

- 3.2.3.1 Retrofit & upgrade market for existing equipment

- 3.2.3.2 Emerging markets in Asia Pacific & Latin America

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.6.3 Historical price trend analysis

- 3.6.4 Pricing strategy by player type

- 3.7 Regulatory landscape

- 3.7.1 OSHA Safety Standards for Welding Equipment

- 3.7.2 ASME Codes & Standards

- 3.7.3 CE Marking Requirements (Europe)

- 3.7.4 API Standards for Oil & Gas Applications

- 3.7.5 Environmental Regulations

- 3.8 Trade data analysis (driven by primary research) - (HS Code - 84682090)

- 3.8.1 Import/Export Volume & Value Trends

- 3.8.2 Key Trade Corridors & Tariff Impact

- 3.9 Impact of AI & Generative AI on the Market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 GenAI use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Supply chain analysis

- 3.10.1 Key component sourcing dynamics

- 3.10.2 Lead time analysis

- 3.10.3 Supply chain disruptions & mitigation strategies

- 3.10.4 Localization vs. Global sourcing trends

- 3.11 Capacity & production landscape

- 3.11.1 Installed capacity by region & key producer

- 3.11.2 Capacity utilization rates & expansion pipelines

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Constant center line (CCL) rotator

- 5.2.1 Light-Duty CCL Rotators

- 5.2.2 Heavy-Duty CCL Rotators

- 5.3 Hydraulic fit up rotator

- 5.3.1 Mobile hydraulic rotators

- 5.3.2 Stationary hydraulic rotators

- 5.4 Self-aligning rotator

- 5.4.1 Manual adjustment self-aligning

- 5.4.2 Automatic self-aligning

Chapter 6 Market Estimates & Forecast, By Welding Type, 2022 - 2035, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Submerged arc welding (SAW)

- 6.2.1 Single-Wire SAW

- 6.2.2 Multi-Wire SAW

- 6.3 Tungsten Inert Gas (TIG) Welding

- 6.3.1 Manual TIG

- 6.3.2 Automated TIG

- 6.4 Metal Inert Gas (MIG) Welding

- 6.4.1 Short Circuit MIG

- 6.4.2 Spray Transfer MIG

- 6.5 Arc Welding

- 6.5.1 Shielded Metal Arc Welding (SMAW)

- 6.5.2 Flux-Cored Arc Welding (FCAW)

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Load Capacity, 2022 - 2035, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Up to 2 tons to 100 tons

- 7.3 100 tons to 500 ton

- 7.4 5000 ton to 2000 ton

- 7.5 More than 2000 tons

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Pressure vessel manufacturing

- 8.2.1 Industrial pressure vessels

- 8.2.2 LPG/ING storage vessels

- 8.3 Heat exchangers manufacturing

- 8.3.1 Shell & tube heat exchangers

- 8.3.2 Plate heat exchangers

- 8.4 Shipbuilding & offshore fabrication

- 8.4.1 Commercial shipbuilding

- 8.4.2 Offshore platforms & structures

- 8.5 Pipe welding

- 8.5.1 Oil & gas pipelines

- 8.5.2 Water & wastewater pipelines

- 8.6 Boilers & tanks

- 8.6.1 Industrial boilers

- 8.6.2 Storage tanks

- 8.7 Wind towers

- 8.7.1 Onshore wind towers

- 8.7.2 Offshore wind towers

- 8.8 Power generation equipment

- 8.8.1 Turbine components

- 8.8.2 Generator casings

- 8.9 Others (heavy equipment fabrication, plant construction, etc.)

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2022 - 2035, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Oil & Gas

- 9.2.1 Upstream

- 9.2.2 Midstream

- 9.2.3 Downstream

- 9.3 Shipbuilding

- 9.3.1 Commercial vessels

- 9.3.2 Defense vessels

- 9.4 Wind energy

- 9.4.1 Onshore wind

- 9.4.2 Offshore wind

- 9.5 Power generation

- 9.5.1 Thermal power

- 9.5.2 Nuclear power

- 9.5.3 Renewable power

- 9.6 Automotive

- 9.6.1 Heavy commercial vehicles

- 9.6.2 Component manufacturing

- 9.7 Aerospace

- 9.7.1 Aircraft manufacturing

- 9.7.2 Space & defense

- 9.8 General manufacturing

- 9.8.1 Heavy equipment fabrication

- 9.8.2 Plant & construction equipment

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Million) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Amin Machinery

- 12.2 Anvin Engineers

- 12.3 Cascade Corporation

- 12.4 Cubuilt Engineers

- 12.5 Huaheng Automation

- 12.6 Indexator

- 12.7 Innovic Technology

- 12.8 Intermercato

- 12.9 Key Plant Automation

- 12.10 KUKA Robotics

- 12.11 MG Welding

- 12.12 Mogra Engineering

- 12.13 Redrock Automation

- 12.14 SENLISWELD

- 12.15 V-Weld