PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038671

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038671

Implantable Pacemakers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

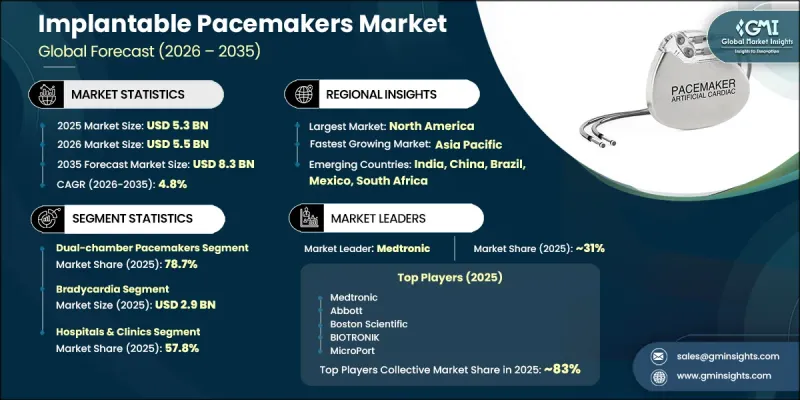

The Global Implantable Pacemakers Market was valued at USD 5.3 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 8.3 billion by 2035.

The market is expanding due to the rising burden of cardiovascular diseases and the increasing adoption of minimally invasive cardiac procedures across healthcare systems worldwide. Growing preference for advanced cardiac rhythm management solutions, supported by favorable reimbursement frameworks, is further strengthening market adoption. Implantable pacemakers are medical devices designed to regulate abnormal heart rhythms by delivering controlled electrical impulses to maintain a stable heart rate. These devices continuously monitor cardiac electrical activity and intervene when irregularities occur, ensuring effective rhythm correction. The increasing incidence of atrial fibrillation and bradyarrhythmias is strongly linked to aging populations, sedentary behavior, obesity, diabetes, and poor dietary habits, all of which are becoming more prevalent globally. Expanding elderly populations are also contributing significantly to demand, as age-related conduction disorders such as atrioventricular block and sick sinus syndrome are becoming more common. As life expectancy rises, the need for long-term cardiac rhythm management solutions is expected to remain strong, supporting sustained market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.3 Billion |

| Forecast Value | $8.3 Billion |

| CAGR | 4.8% |

The dual-chamber pacemakers segment held a share of 78.7% in 2025. This segment leads due to its ability to maintain atrioventricular synchrony, resulting in improved cardiac efficiency and better patient outcomes compared to single-chamber alternatives. Strong clinical preference for dual-chamber systems, particularly in high-risk and elderly patient populations, along with their suitability for a wide range of conduction disorders, continues to reinforce their market dominance.

The bradycardia segment accounted for USD 2.9 billion in 2025. Bradycardia remains a primary clinical indication for implantable pacemakers, as these devices are widely accepted as the standard treatment for managing slow heart rhythms. The condition is commonly associated with age-related degeneration of the cardiac conduction system, cardiovascular disorders, medication effects, and autonomic dysfunction. Patients often experience symptoms such as fatigue, dizziness, fainting episodes, and shortness of breath, which can significantly reduce quality of life and increase cardiovascular risk. Implantable pacemakers effectively restore normal heart rhythm through controlled stimulation, improving both symptom management and overall patient outcomes.

North America Implantable Pacemakers Market accounted for a 41.7% share in 2025. The region's leadership is supported by a high prevalence of cardiovascular and rhythm-related disorders driven by aging demographics, obesity, hypertension, diabetes, and lifestyle-related risk factors. Strong technological advancement further strengthens the regional market, with manufacturers continuously focusing on innovation in areas such as leadless systems, MRI-compatible devices, extended battery performance, and remote monitoring capabilities.

Key companies operating in the Global Implantable Pacemakers Industry include Abbott, BIOTRONIK, Boston Scientific, Lepu Medical, MEDICO, Medtronic, MicroPort, Shree Pacetronix, and Vitatron. Companies in the implantable pacemakers market are prioritizing continuous innovation in cardiac rhythm management technologies to improve device safety, longevity, and performance. Significant investments in research and development are enabling the introduction of miniaturized devices, leadless systems, and advanced monitoring capabilities. Strategic collaborations with hospitals and cardiac care centers are strengthening clinical adoption and expanding procedural access. Manufacturers are also focusing on enhancing battery efficiency and device durability to reduce replacement frequency and improve patient convenience. Expansion into emerging healthcare markets is supporting broader patient reach and revenue diversification.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cardiovascular diseases & aging demographics

- 3.2.1.2 Technological advancements in leadless and MRI-compatible devices

- 3.2.1.3 Growing adoption of remote monitoring and telehealth solutions

- 3.2.1.4 Favorable reimbursement scenario

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of implantable pacemakers

- 3.2.2.2 Risks and complications

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of ambulatory surgical centers for cost-effective procedures

- 3.2.3.2 AI-enabled predictive analytics for cardiac rhythm management

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario (Driven by primary research)

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Patent analysis (Driven by primary research)

- 3.11 Pricing analysis, 2025 (Driven by primary research)

- 3.12 Investment and funding analysis

- 3.13 Supply chain analysis

- 3.14 Impact of AI and Generative AI on the market

- 3.14.1 AI-driven disruption of existing business models

- 3.14.2 GenAI use cases and adoption roadmap by segment

- 3.14.3 Risks, limitations and regulatory considerations

- 3.15 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Single-chamber pacemakers

- 5.2.1 Single-chamber atrial

- 5.2.2 Single-chamber ventricular

- 5.3 Dual-chamber pacemakers

- 5.4 Biventricular/CRT pacemakers

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Bradycardia

- 6.3 Arrhythmias

- 6.4 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals & clinics

- 7.3 Cardiac care centers

- 7.4 Ambulatory surgical centers

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 BIOTRONIK

- 9.3 Boston Scientific

- 9.4 Lepu Medical

- 9.5 MEDICO

- 9.6 Medtronic

- 9.7 MicroPort

- 9.8 Shree Pacetronix

- 9.9 Vitatron