PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038674

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038674

Air Conditioning System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

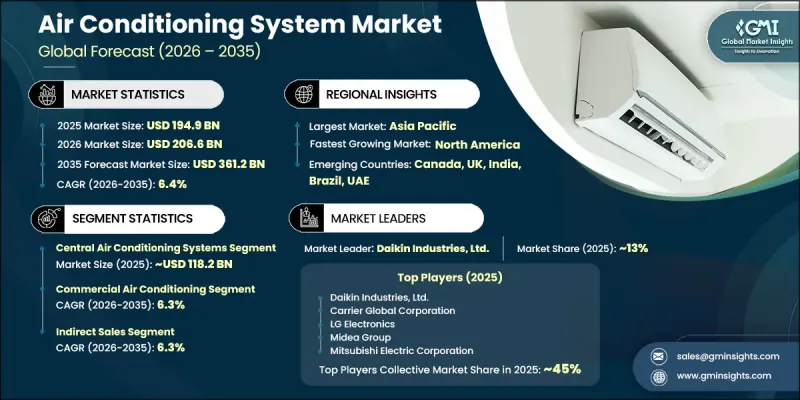

The Global Air Conditioning System Market was valued at USD 194.9 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 361.2 billion by 2035.

The market is expanding as rising global temperatures and shifting climate patterns significantly increase dependence on cooling solutions across all major regions. Growing intensity and frequency of heatwaves, along with extended warm seasons and higher average temperatures, are transforming air conditioning from a discretionary purchase into an essential requirement for thermal comfort and operational continuity. Urban environments are experiencing even stronger demand due to the heat island effect, which further elevates ambient temperatures and accelerates cooling needs. Residential, commercial, and industrial infrastructures are increasingly reliant on air conditioning systems to maintain indoor comfort and productivity levels. At the same time, improving income levels and rising living standards are reinforcing demand, particularly in emerging economies where consumers are upgrading from basic cooling alternatives to more advanced and energy-efficient systems. Expanding middle-class populations, easier access to financing, and rapid urban development across regions such as Asia-Pacific, the Middle East, Africa, and Latin America are further strengthening adoption rates. As climate variability continues to intensify globally, the demand for efficient, sustainable, and reliable air conditioning systems is expected to remain structurally strong over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $194.9 Billion |

| Forecast Value | $361.2 Billion |

| CAGR | 6.4% |

The central air conditioning systems segment accounted for USD 118.2 billion in 2025 and is projected to grow at a CAGR of 6.5% from 2026 to 2035. Increasing urban infrastructure development and large-scale construction activities are driving strong adoption of centralized cooling solutions across various building types. Rising construction of commercial complexes, healthcare facilities, transportation hubs, hospitality establishments, data processing centers, and high-density residential projects is boosting demand for centralized systems that ensure uniform temperature control, improved air quality management, and reduced noise levels. Additionally, the growing focus on energy efficiency and environmental sustainability is supporting the transition toward modern centralized systems equipped with advanced chillers, variable speed technologies, and intelligent control mechanisms that reduce energy consumption and operating expenses compared to decentralized cooling setups.

The indirect distribution channel held a 68.6% share in 2025 and is expected to grow at a CAGR of 6.3% through 2035. This channel includes distributors, dealers, wholesalers, retailers, and expanding online platforms that collectively enable manufacturers to reach a wider consumer base across diverse geographic regions. It plays a crucial role in penetrating emerging urban and semi-urban markets where direct sales networks are limited. The channel structure provides customers with easier access to multiple brands, competitive pricing options, localized product availability, and bundled installation and maintenance services. These advantages make indirect distribution especially effective in residential and light commercial applications, where convenience and service accessibility strongly influence purchasing decisions.

U.S. Air Conditioning System Market accounted for USD 43.4 billion in 2025 and is anticipated to grow at a CAGR of 6.5% from 2026 to 2035. Increasing temperatures, recurring heatwave events, and longer cooling seasons are significantly raising cooling demand across residential, commercial, and industrial sectors. Strong consumer purchasing power and high disposable income levels are also supporting widespread adoption of both standard and premium air conditioning systems. Replacement demand for aging HVAC infrastructure, along with upgrades to more energy-efficient solutions, is further reinforcing market expansion across the country.

Major players operating in the Global Air Conditioning System Industry include Panasonic Corporation, LG Electronics, Haier Group Corporation, Daikin Industries, Ltd., Carrier Global Corporation, Mitsubishi Electric Corporation, Samsung Electronics Co., Ltd., Johnson Controls, Bosch, Blue Star Limited, Gree Electric Appliances Inc., Midea Group, Trane Technologies (Ingersoll Rand), Voltas Limited, and Rheem Manufacturing Company. Key companies in the Air Conditioning System Market are focusing on enhancing energy efficiency through the development of inverter-based and smart HVAC technologies that reduce power consumption and improve operational performance. They are investing heavily in research and development to integrate IoT-enabled controls, predictive maintenance, and AI-driven climate management systems. Expansion of manufacturing facilities and strengthening of global supply chains are helping companies improve production capacity and reduce delivery timelines. Strategic collaborations with construction firms, real estate developers, and commercial infrastructure projects are increasing product adoption in large-scale installations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Cooling capacity

- 2.2.4 Refrigerant type

- 2.2.5 Energy efficiency class

- 2.2.6 End-use

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global temperatures and climate change

- 3.2.1.2 Growing disposable income and improved living standards

- 3.2.1.3 Technological advancements and smart features

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High energy consumption and operating costs

- 3.2.2.2 High initial installation costs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Pricing analysis (driven by primary research)

- 3.7.1 Historical price trend analysis

- 3.7.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.7.3 Regional price variations

- 3.7.4 Price sensitivity by end-user segment

- 3.8 Trade data analysis (driven by primary research)

- 3.8.1 Import/export volume & value trends

- 3.8.2 Key trade corridors & tariff impact

- 3.8.3 Trade policy implications

- 3.9 Capacity & production landscape (driven by primary research)

- 3.9.1 Installed capacity by region & key producer

- 3.9.2 Capacity utilization rates & expansion pipelines

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 GenAI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Central air conditioning systems

- 5.3 Split air conditioning systems

- 5.4 Window unit air conditioning system

- 5.5 Ductless mini-split systems

Chapter 6 Market Estimates & Forecast, By Cooling Capacity, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Low capacity (Less than 12,000 BTU)

- 6.3 Medium capacity (12,000 - 24,000 BTU)

- 6.4 High capacity (24,000 - 60,000 BTU)

- 6.5 Ultra-high capacity (Over 60,000 BTU)

Chapter 7 Market Estimates & Forecast, By Refrigerant Type, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 R-410A (Standard)

- 7.3 R-32 (Lower GWP)

- 7.4 R-290 (Propane/Natural Refrigerant)

- 7.5 Next-gen low-GWP refrigerants

Chapter 8 Market Estimates & Forecast, By Energy Efficiency Class, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Standard Efficiency

- 8.3 High Efficiency

- 8.4 Ultra-High Efficiency

Chapter 9 Market Estimates & Forecast, By End-Use, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Residential air conditioning

- 9.3 Commercial air conditioning

- 9.4 Industrial air conditioning

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Indonesia

- 11.4.7 Malaysia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Blue Star Limited

- 12.2 Bosch

- 12.3 Carrier Global Corporation

- 12.4 Daikin Industries Ltd.

- 12.5 Gree Electric Appliances Inc.

- 12.6 Haier Group Corporation

- 12.7 Johnson Controls

- 12.8 LG Electronics

- 12.9 Midea Group

- 12.10 Mitsubishi Electric Corporation

- 12.11 Panasonic Corporation

- 12.12 Rheem Manufacturing Company

- 12.13 Samsung Electronics Co., Ltd.

- 12.14 Trane Technologies (Ingersoll Rand)

- 12.15 Voltas Limited