PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038695

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038695

Polyvinyl Chloride Resin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

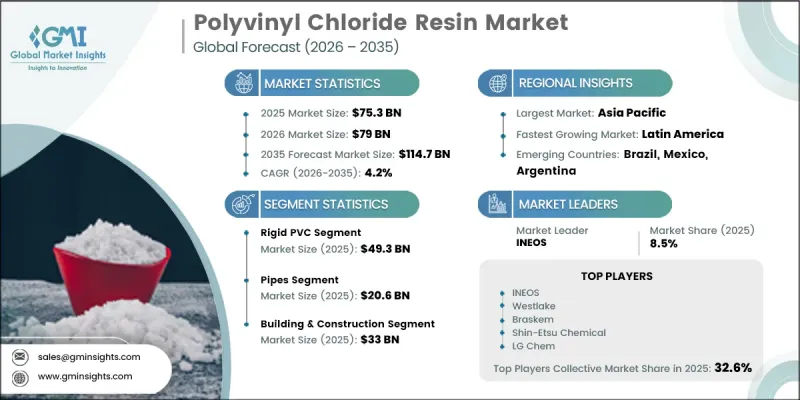

The Global Polyvinyl Chloride (PVC) Resin Market was valued at USD 75.3 billion in 2025 and is estimated to grow at a CAGR of 4.2% to reach USD 114.7 billion in 2035.

Market expansion is driven by strong and sustained demand across construction, infrastructure, packaging, automotive, and electrical industries, where PVC resin is widely used due to its durability and cost efficiency. The material's versatility across rigid and flexible applications continues to reinforce its global adoption. Increasing infrastructure development and urban expansion are supporting higher consumption of PVC-based products, particularly in building materials and utility systems. Rising industrial activity, coupled with demand for lightweight, corrosion-resistant, and long-lasting materials, is further strengthening market growth. Continuous improvements in polymerization techniques and processing methods, such as extrusion, molding, and calendering, are enhancing production efficiency and product customization capabilities. PVC resin's resistance to moisture, chemicals, and environmental wear makes it suitable for both indoor and outdoor applications, supporting long service life. The growing emphasis on material efficiency and recyclability is also influencing production strategies, as manufacturers focus on sustainable formulations and improved lifecycle performance. Overall, PVC resin remains a critical material in modern industrial and construction ecosystems due to its functional adaptability and strong mechanical properties.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $75.3 Billion |

| Forecast Value | $114.7 Billion |

| CAGR | 4.2% |

Rigid PVC accounted for the largest market value of USD 49.3 billion in 2025. Demand for rigid PVC is primarily driven by large-scale construction and infrastructure development activities, where its strength, stability, and resistance to corrosion make it highly suitable. The material is widely preferred in applications requiring durability and low maintenance, supporting its extensive use in structural and utility-based installations.

The building and construction segment reached USD 33 billion in 2025. PVC resin is extensively utilized in this sector due to its suitability for applications that require resistance to weather conditions, corrosion protection, and long-term structural reliability. Its consistent use in construction-related components continues to support steady demand across global infrastructure development projects.

North America Polyvinyl Chloride (PVC) Resin Market is projected to grow from USD 14.1 billion in 2025 to USD 22 billion in 2035. Growth in the region is influenced by infrastructure renewal activities, renovation projects, and stable demand from the construction and electrical sectors. Increased focus on recycling initiatives and regulatory compliance is also shaping market dynamics. In the United States, strong demand is supported by residential construction, utility upgrades, piping systems, and wire insulation applications, driven by ongoing housing development and industrial manufacturing stability across multiple regions.

INEOS, Braskem, Shin-Etsu Chemical, Westlake, LG Chem, Mitsubishi Chemical Corporation, Nexeo Plastics, LLC., SCG Chemicals, Solvay, SNG Microns, and Chemplast Sanmar are among the key companies operating in the polyvinyl chloride (PVC) resin market. Companies in the Polyvinyl Chloride (PVC) Resin Market are focusing on capacity expansion, product innovation, and sustainability-driven production strategies to strengthen their competitive position. Manufacturers are investing in advanced polymerization technologies to improve efficiency, consistency, and cost-effectiveness. There is also a strong emphasis on developing recyclable and eco-friendly PVC formulations in response to environmental regulations and sustainability goals. Strategic collaborations and long-term supply agreements with construction and industrial end users are helping companies secure stable demand. In addition, firms are expanding their global distribution networks and strengthening regional manufacturing bases to improve supply chain efficiency. Continuous research into high-performance grades of rigid and flexible PVC is enabling better application versatility, while digitalization in production and process optimization is further enhancing operational performance and market competitiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Application

- 2.2.3 End Use

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expanding infrastructure and construction activities

- 3.2.1.2 Cost-effective material for diverse applications

- 3.2.1.3 Demand for durable electrical insulation materials

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 Environmental concerns related to PVC disposal

- 3.2.2.2 Regulatory pressure on plastic material usage

- 3.2.3 Opportunities

- 3.2.3.1 Development of sustainable PVC formulations

- 3.2.3.2 Growth in medical and healthcare applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By type

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Rigid PVC

- 5.3 Flexible PVC

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dashboards

- 6.3 Consumer electronics

- 6.4 Sealants

- 6.5 Electric wires

- 6.6 Flooring

- 6.7 Pipes

- 6.8 Cable insulation

- 6.9 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Building & construction

- 7.4 Electrical & electronics

- 7.5 Medical & pharmaceuticals

- 7.6 Consumer goods

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Braskem

- 9.2 Nexeo Plastics, LLC.

- 9.3 Chemplast Sanmar

- 9.4 INEOS

- 9.5 LG Chem

- 9.6 Mitsubishi Chemical Corporation

- 9.7 Shin-Etsu Chemical

- 9.8 Solvay

- 9.9 SCG Chemicals

- 9.10 SNG Microns

- 9.11 Westlake