PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038707

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038707

Pet Care Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

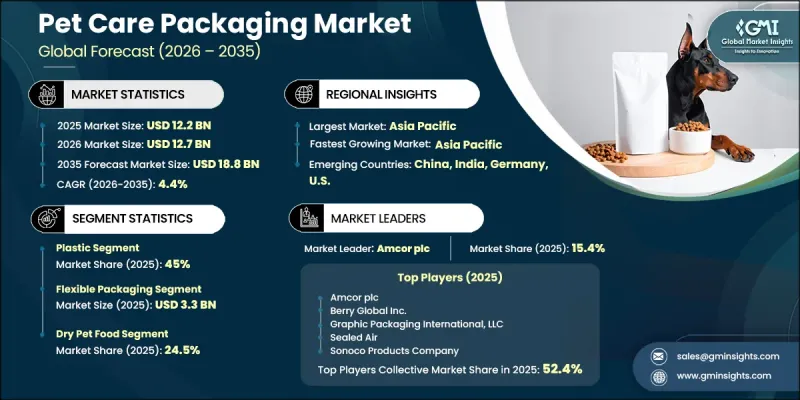

The Global Pet Care Packaging Market was valued at USD 12.2 billion in 2025 and is estimated to grow at a CAGR of 4.4% to reach USD 18.8 billion by 2035.

The market growth is supported by rising pet ownership worldwide, increasing expenditure on companion animal nutrition and healthcare products, and the growing popularity of premium pet food offerings. Expansion of online retail channels and direct-to-consumer pet brands is also strengthening demand for advanced packaging formats. In addition, rising consumer preference for convenient packaging solutions with features such as easy handling, resealability, and portion control is shaping product development trends. At the same time, sustainability concerns are driving a shift toward eco-friendly and recyclable materials, influencing both design innovation and material selection. Packaging is increasingly being viewed not just as a protective layer but also as a branding and product differentiation tool in the pet care industry, supporting premium positioning and customer engagement across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.2 Billion |

| Forecast Value | $18.8 Billion |

| CAGR | 4.4% |

The pet care packaging market is driven by increasing pet adoption rates and rising spending on pet wellness products, which continues to boost demand for packaged food and healthcare items. Growing consumer preference for functional packaging features such as resealable closures, improved durability, and user-friendly handling is further enhancing market expansion. Sustainability is also playing a major role, with manufacturers shifting toward environmentally responsible materials and innovative packaging designs. Collectively, these factors are encouraging the development of more efficient, functional, and eco-conscious packaging solutions across the industry.

The paper and paperboard segment is expected to register a CAGR of 5.6% during 2025-2035, supported by rising demand for recyclable and biodegradable packaging solutions. Increasing sustainability commitments from pet food manufacturers and retailers are encouraging the use of fiber-based materials across dry food packaging, pet treats, and secondary packaging formats, strengthening the shift toward environmentally friendly alternatives.

The dry pet food segment accounted for 24.5% in 2025, driven by its widespread consumption, extended shelf life, and strong preference among pet owners. This category requires packaging with high barrier properties and moisture resistance to preserve freshness, nutritional quality, and product stability, which continues to generate consistent and large-scale demand for packaging solutions.

North America Pet Care Packaging Market held a 34.7% share in 2025. Market expansion in the region is supported by high pet ownership rates and increasing demand for premium pet food and care products. Strong consumer inclination toward pet humanization is driving the need for high-quality, functional, and visually appealing packaging solutions across the regional market.

Key companies operating in the Global Pet Care Packaging Market include Amcor plc, Berry Global Inc., Huhtamaki, Mondi, Sealed Air, Smurfit Kappa, Sonoco Products Company, WestRock Company, DS Smith, Constantia Flexibles, Coveris, Graphic Packaging International, LLC, Silgan Holdings, Trivium Packaging, ProAmpac, Printpack, PPC Flex Company Inc., ATID Packaging, NNZ Group BV, Plastek Group, and Winpak LTD. Companies in the Pet Care Packaging Market are focusing on sustainability-driven innovation by developing recyclable, biodegradable, and lightweight packaging materials to meet environmental regulations and consumer expectations. Many players are investing in advanced manufacturing technologies to enhance packaging durability, shelf life, and functional performance. Expansion of product portfolios with resealable, portion-controlled, and convenience-oriented packaging formats is also a key strategy. Strategic collaborations with pet food brands and retail chains are helping companies strengthen market reach and improve customization capabilities. In addition, firms are increasingly leveraging digital printing and smart packaging technologies to enhance branding and consumer engagement.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Packaging type trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet ownership and humanization of pets

- 3.2.1.2 Growing demand for packaged and processed pet food

- 3.2.1.3 Expansion of e-commerce and direct-to-consumer pet brands

- 3.2.1.4 Increasing focus on convenience and functional packaging features

- 3.2.1.5 Rising adoption of sustainable and eco-friendly packaging solutions

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of sustainable and specialty packaging materials

- 3.2.2.2 Complex regulatory compliance and packaging standardization requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of smart and connected packaging solutions for pet care products

- 3.2.3.2 Expansion of customized and small-batch packaging for niche pet nutrition segments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Plastic

- 5.3 Paper & paperboard

- 5.4 Metal

- 5.5 Multi-material / laminated

Chapter 6 Market Estimates and Forecast, By Packaging Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Flexible packaging

- 6.3 Rigid plastic containers

- 6.4 Folding cartons

- 6.5 Rigid metal containers

- 6.6 Corrugated boxes

- 6.7 Tubes

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Dry pet food

- 7.3 Wet pet food

- 7.4 Pet treats

- 7.5 Pet litter

- 7.6 Pet healthcare & supplements

- 7.7 Pet grooming products

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Amcor plc

- 9.1.2 Berry Global Inc.

- 9.1.3 Graphic Packaging International, LLC

- 9.1.4 Sealed Air

- 9.1.5 Sonoco Products Company

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 Plastek Group

- 9.2.1.2 PPC Flex Company Inc.

- 9.2.1.3 Printpack

- 9.2.1.4 ProAmpac

- 9.2.1.5 Silgan Holdings

- 9.2.1.6 WestRock Company

- 9.2.1.7 Winpak LTD.

- 9.2.2 Asia Pacific

- 9.2.2.1 ATID Packaging

- 9.2.3 Europe

- 9.2.3.1 Constantia Flexibles

- 9.2.3.2 Coveris

- 9.2.3.3 DS Smith

- 9.2.3.4 Huhtamaki

- 9.2.3.5 Mondi

- 9.2.3.6 NNZ Group BV

- 9.2.3.7 Smurfit Kappa

- 9.2.3.8 Trivium Packaging

- 9.2.1 North America