PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038727

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038727

Polypropylene Yarn Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

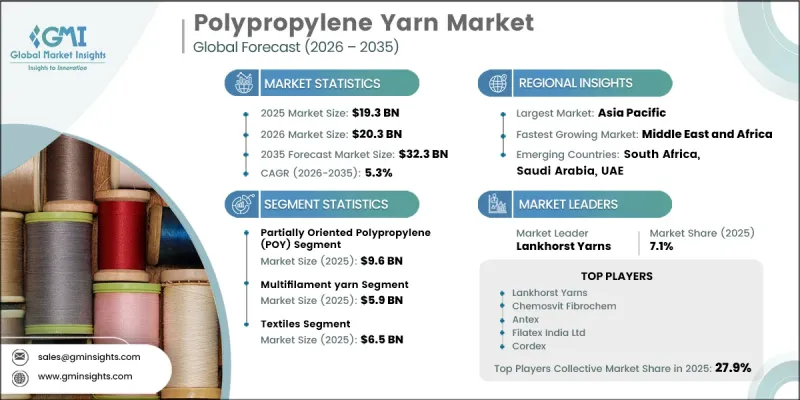

The Global Polypropylene Yarn Market was valued at USD 19.3 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 32.3 billion by 2035.

The market continues to evolve as industries demand durable, lightweight, and cost-effective synthetic materials for a wide range of applications. Polypropylene yarn is produced through extrusion and spinning techniques using polypropylene polymer, offering properties such as low moisture absorption, chemical resistance, and structural stability. These characteristics make it suitable for environments that require reliable performance under varying conditions. The material can be manufactured in multiple formats, including multifilament, monofilament, and tape yarn, allowing flexibility across different end uses. Its ability to retain strength despite repeated use and exposure to external elements contributes to its consistent demand. In addition, the yarn's resistance to moisture supports dimensional stability and helps limit microbial development. The market is further supported by the material's recyclability, enabling reuse through controlled processing methods. As industries continue to prioritize efficiency and product longevity, polypropylene yarn remains a practical choice for functional textile applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $19.3 Billion |

| Forecast Value | $32.3 Billion |

| CAGR | 5.3% |

The partially oriented polypropylene yarn segment accounted for USD 9.6 billion in 2025. It serves as an intermediate product that allows flexible downstream processing, while fully drawn polypropylene yarn continues to see steady demand in applications requiring immediate dimensional stability and consistent performance. Together, these categories support improvements in production efficiency, filament consistency, and process control across industrial and packaging textile segments.

The multifilament polypropylene yarn segment captured USD 5.9 billion in 2025. Demand for both monofilament and multifilament variants remains strong across sectors that require durability, structural integrity, and long service life. Other yarn types, including spun and textured formats, are also utilized in applications that require enhanced flexibility, surface variation, and ease of handling, particularly in functional and furnishing-related textile products.

North America Polypropylene Yarn Market is expected to grow from USD 4.6 billion in 2025 to USD 7.3 billion by 2035. Growth in the region is supported by steady demand from sectors requiring reliable material performance and consistent supply. The United States continues to rely on these materials for various industrial and technical applications, contributing to sustained market expansion.

Key companies operating in the Global Polypropylene Yarn Market include Lotte Chemical Corporation, Filatex India Ltd, Barnet, Cordex, Chemosvit Fibrochem, BR Group a.s., Antex, Agropoli, Essegomma, Dostlar, and Lankhorst Yarns. Companies in the Polypropylene Yarn Market are strengthening their market presence through continuous innovation and product development focused on improving durability, efficiency, and performance characteristics. Investments in advanced manufacturing technologies are helping enhance production quality and reduce operational costs. Strategic partnerships and distribution agreements are being formed to expand market reach and improve supply chain efficiency. Firms are also focusing on sustainability by incorporating recyclable materials and optimizing resource utilization. Capacity expansion and geographic diversification are enabling companies to meet rising global demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Process Type

- 2.2.2 Product Type

- 2.2.3 Application

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for lightweight industrial textiles

- 3.2.1.2 Increased use in packaging applications

- 3.2.1.3 Cost efficiency compared to natural fibers

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 Sensitivity to high temperature exposure

- 3.2.2.2 Limited dye absorption characteristics

- 3.2.3 Opportunities

- 3.2.3.1 Expanding use in agricultural applications

- 3.2.3.2 Growth in recyclable textile products

- 3.2.3.3 Technological improvements in yarn processing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Process Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Partially oriented polypropylene (POY)

- 5.3 Fully drawn polypropylene (FDY)

- 5.4 Draw textured yarn

Chapter 6 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Monofilament yarn

- 6.3 Multifilament yarn

- 6.4 Spun yarn

- 6.5 Textured yarn

- 6.6 Dyed yarn

- 6.7 Fibrillated yarn

- 6.8 Tape yarn

- 6.9 Air-textured yarn

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Textiles

- 7.3 Construction materials

- 7.4 Automotive

- 7.5 Packaging

- 7.6 Sports accessories

- 7.7 Medical textiles

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Antex

- 9.2 Agropoli

- 9.3 Barnet

- 9.4 BR Group a.s.

- 9.5 Chemosvit Fibrochem

- 9.6 Cordex

- 9.7 Dostlar

- 9.8 Essegomma

- 9.9 Filatex India Ltd

- 9.10 Lotte Chemical Corporation

- 9.11 Lankhorst Yarns