PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038756

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038756

Small Cell Network Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

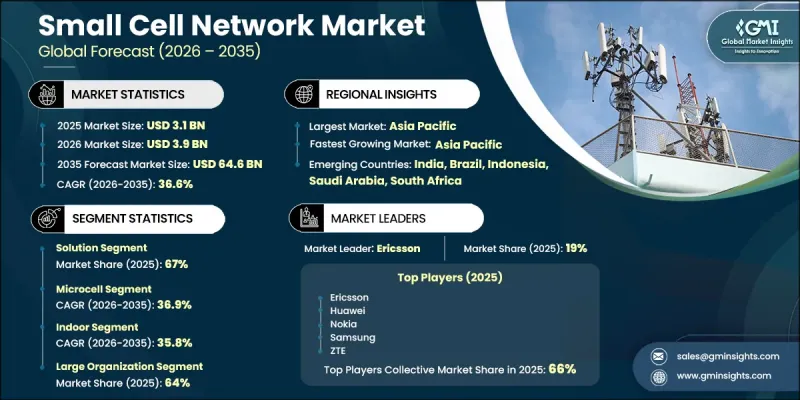

The Global Small Cell Network Market was valued at USD 3.1 billion in 2025 and is estimated to grow at a CAGR of 36.6% to reach USD 64.6 billion by 2035.

The accelerating rollout of next-generation mobile networks is significantly increasing the deployment of compact cellular infrastructure to support high-speed connectivity, particularly in densely populated urban environments and indoor spaces. Telecom operators are actively investing in these solutions to meet rising performance expectations driven by data-intensive applications. The surge in mobile data usage, fueled by digital services and connected platforms, is further intensifying the need for network densification to reduce congestion and enhance user experience. Additionally, the rapid expansion of connected ecosystems is creating demand for reliable, high-capacity wireless coverage. Emerging applications that require ultra-low latency and real-time responsiveness are further reinforcing the importance of small cell infrastructure. Industry transformation toward cloud-native architectures and flexible network models is also contributing to broader adoption, as operators prioritize scalable and cost-efficient deployment strategies supported by intelligent automation technologies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.1 Billion |

| Forecast Value | $64.6 Billion |

| CAGR | 36.6% |

The solution segment held a 67% share and is projected to grow at a CAGR of 36% through 2035. Telecommunications providers are increasingly adopting virtualized and cloud-enabled solutions that allow centralized control, rapid deployment, and improved scalability. These approaches reduce reliance on traditional hardware while enabling seamless integration with modern network architectures, ultimately enhancing operational flexibility and cost efficiency.

The microcell segment captured 37.8% share in 2025 and is expected to grow at a CAGR of 36.9% between 2026 and 2035. These medium-powered units are designed to deliver short-range coverage in high-density outdoor environments, supporting increased network capacity. Their ability to handle substantial traffic loads while extending coverage makes them a vital component in network densification strategies and in supporting advanced mobile network performance in urban areas.

U.S. Small Cell Network Market reached USD 723.9 million in 2025. Growth in the country is being driven by increasing investment in private wireless networks that prioritize secure, low-latency connectivity for enterprise applications. The demand for advanced communication infrastructure is expanding as organizations adopt connected technologies and automation systems. Telecommunications providers are also focusing on deploying dense network infrastructures to improve coverage and performance in high-traffic urban locations. Ongoing investments in advanced spectrum utilization and infrastructure development continue to strengthen market expansion.

Key companies operating in the Global Small Cell Network Market include Airspan Networks, Baicells Technologies, CommScope, Ericsson, Fujitsu, Huawei, Mavenir, Nokia, Samsung, and ZTE. Companies in the small cell network market are strengthening their market position through innovation, strategic alliances, and technology integration. Industry players are investing in cloud-native and virtualized network solutions to enhance scalability and reduce deployment costs. Partnerships with telecom operators and enterprises are enabling broader adoption of advanced connectivity solutions. Companies are also focusing on integrating artificial intelligence and automation to improve network efficiency, enable predictive maintenance, and optimize traffic management. Expanding global presence through infrastructure development and strengthening distribution networks are key priorities.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Cell

- 2.2.4 Technology

- 2.2.5 Deployment mode

- 2.2.6 End use

- 2.2.7 Organization size

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 5G network densification demand

- 3.2.1.2 Rising mobile data traffic

- 3.2.1.3 Increasing IoT and connected devices adoption

- 3.2.1.4 Demand for low-latency high-speed connectivity

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Backhaul connectivity constraints

- 3.2.2.2 High deployment and maintenance cost

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of private 5G enterprise networks

- 3.2.3.2 Growth of smart cities initiatives

- 3.2.3.3 Adoption of Open RAN architecture

- 3.2.3.4 Integration with edge computing and AI

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing analysis (Driven by Primary Research)

- 3.5.1 Historical price trend analysis

- 3.5.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 Federal Communications Commission (FCC)

- 3.6.1.2 Innovation, Science and Economic Development Canada (ISED)

- 3.6.2 Europe

- 3.6.2.1 European Commission - DG CONNECT

- 3.6.2.2 Body of European Regulators for Electronic Communications (BEREC)

- 3.6.3 Asia Pacific

- 3.6.3.1 Ministry of Industry and Information Technology (MIIT), China

- 3.6.3.2 Telecom Regulatory Authority of India (TRAI)

- 3.6.4 Latin America

- 3.6.4.1 Agencia Nacional de Telecomunicacoes (ANATEL), Brazil

- 3.6.4.2 Instituto Federal de Telecomunicaciones (IFT), Mexico

- 3.6.5 Middle East & Africa

- 3.6.5.1 Communications and Information Technology Commission (CITC), Saudi Arabia

- 3.6.5.2 Independent Communications Authority of South Africa (ICASA)

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by Primary Research)

- 3.11 Trade data analysis (Driven by paid database)

- 3.11.1 Import/export volume & value trends

- 3.11.2 Key trade corridors & tariff impact

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 Gen AI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Network management software

- 5.2.2 Performance optimization software

- 5.3 Services

- 5.3.1 Professional service

- 5.3.2 Managed service

Chapter 6 Market Estimates & Forecast, By Cell, 2022 - 2035 ($Mn, Mn Units)

- 6.1 Key trends

- 6.2 Femtocell

- 6.3 Picocell

- 6.4 Microcell

- 6.5 Metro cells

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 4G LTE

- 7.3 5G

Chapter 8 Market Estimates & Forecast, By Deployment mode, 2022 - 2035 ($Mn, Mn Units)

- 8.1 Key trends

- 8.2 Indoor

- 8.3 Outdoor

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Telecom Operators & Service Providers

- 9.3 Enterprises

- 9.4 Smart Cities & Public Infrastructure

- 9.5 Healthcare

- 9.6 Education

- 9.7 Retail & Hospitality

- 9.8 Industrial & Manufacturing

Chapter 10 Market Estimates & Forecast, By Organization size, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 SME

- 10.3 Large organization

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Mn Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Nordics

- 11.3.7 Russia

- 11.3.8 Poland

- 11.3.9 Romania

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Vietnam

- 11.4.7 Indonesia

- 11.4.8 Philippines

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global players

- 12.1.1 Airspan

- 12.1.2 Baicells

- 12.1.3 CommScope

- 12.1.4 Ericsson

- 12.1.5 Fujitsu

- 12.1.6 Huawei

- 12.1.7 NEC

- 12.1.8 Nokia

- 12.1.9 Samsung

- 12.1.10 ZTE

- 12.2 Regional players

- 12.2.1 Casa Systems

- 12.2.2 ip.access

- 12.2.3 JMA Wireless

- 12.2.4 Mavenir

- 12.2.5 Parallel Wireless

- 12.2.6 Radisys

- 12.3 Emerging players

- 12.3.1 Genew Technologies

- 12.3.2 Rakuten Symphony

- 12.3.3 Sercomm

- 12.3.4 Solid