PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038761

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038761

Automotive Electric Actuators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

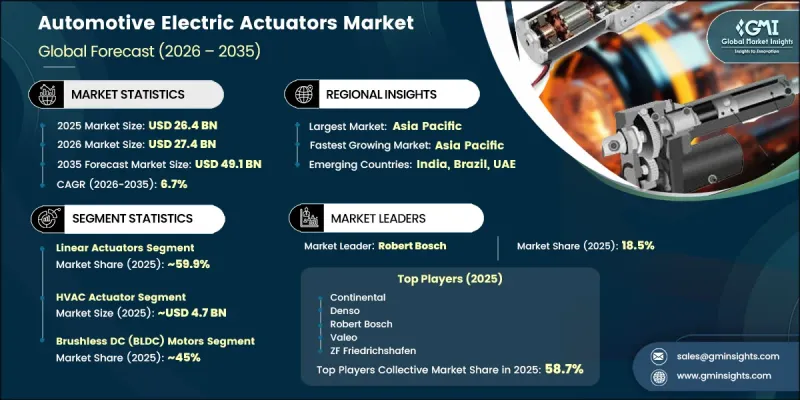

The Global Automotive Electric Actuators Market was valued at USD 26.4 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 49.1 billion by 2035.

The market expansion is supported by the growing presence of major OEMs and strong government initiatives encouraging electric vehicle adoption. As environmental priorities intensify and regulatory frameworks promote cleaner mobility solutions, the demand for efficient and reliable vehicle components such as electric actuators continues to increase. The automotive electric actuators industry is further benefiting from advancements in vehicle electrification, increasing integration of automated systems, and rising consumer expectations for enhanced comfort and performance. Continuous innovation in automotive engineering is driving the integration of intelligent actuation systems across vehicle platforms. Additionally, rising investments in electric mobility infrastructure and production capabilities are strengthening long-term growth prospects. The market is also supported by the shift toward energy-efficient vehicle systems and the growing emphasis on sustainability across the automotive value chain.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $26.4 Billion |

| Forecast Value | $49.1 Billion |

| CAGR | 6.7% |

The presence of major automotive manufacturers and supportive government policies aimed at accelerating electric vehicle deployment is creating strong growth opportunities for actuator manufacturers. Leading automakers are investing heavily in electric vehicle production across key regions, further strengthening demand for advanced actuator technologies. As regulatory support increases and environmental considerations become prominent, the need for dependable and high-performance automotive components continues to rise, reinforcing the importance of electric actuators in modern vehicle architectures.

The linear actuators segment held a 59.9% share, generating USD 15.8 billion in 2025. These actuators are widely preferred due to their ability to convert rotary motion into linear movement, enabling various essential vehicle functions. Their capability to deliver high force within controlled motion ranges makes them highly suitable for automotive applications, contributing to their strong market dominance.

The HVAC actuator segment accounted for 17.8% share in 2025, reaching a value of USD 4.7 billion. These actuators play a critical role in regulating temperature, airflow, and overall cabin comfort. Modern automotive systems rely on multiple actuators to manage air distribution and thermal control, supporting improved passenger comfort and system efficiency.

United States Automotive Electric Actuators Market reached USD 4.2 billion in 2025 and is expected to grow at a CAGR of 6.5% from 2026 to 2035. The country maintains a leading position in North America due to higher actuator integration per vehicle, driven by demand for advanced features, comfort, and stringent safety requirements. Regulatory standards and technological advancements continue to support widespread adoption of actuator-based systems across vehicles.

Key players operating in the Global Automotive Electric Actuators Industry include Aisin, BorgWarner, Continental, Denso, Johnson Electric, Mitsubishi Electric, Nidec, Robert Bosch, Valeo, and ZF Friedrichshafen. Companies in the automotive electric actuators market are focusing on innovation, strategic collaborations, and expanding production capabilities to strengthen their competitive position. Investments in research and development are enabling the creation of advanced, energy-efficient actuator systems tailored for electric and autonomous vehicles. Firms are also forming partnerships with OEMs to secure long-term supply agreements and enhance product integration. Geographic expansion into high-growth markets and the establishment of localized manufacturing facilities are helping companies improve supply chain efficiency and reduce costs. Additionally, organizations are prioritizing digitalization and smart actuator technologies to align with evolving automotive trends.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Actuator

- 2.2.3 Product

- 2.2.4 Motor Technology

- 2.2.5 Application

- 2.2.6 Vehicle

- 2.2.7 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing Adoption of Electric Vehicles (EVs)

- 3.2.1.2 Advancements in Autonomous Driving Technologies

- 3.2.1.3 Rising Consumer Preferences for Comfort and Convenience

- 3.2.1.4 Rising Automotive Safety Standards

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Integration Challenges with Traditional Mechanical Systems

- 3.2.2.2 Dependency on Rare Earth Materials for Actuator Manufacturing

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing Government Incentives for EV Adoption

- 3.2.3.2 Growth in Hybrid Electric Vehicle (HEV) Production

- 3.2.3.3 Integration of Smart Technologies in Vehicle Systems

- 3.2.1 Growth drivers

- 3.3 Technology and innovation landscape

- 3.3.1 Current technologies

- 3.3.1.1 Brushless DC (BLDC) Motors

- 3.3.1.2 Piezoelectric Actuators

- 3.3.1.3 Hydraulic Electric Actuators

- 3.3.1.4 Electromechanical Actuators

- 3.3.2 Emerging technologies

- 3.3.2.1 Wireless Electric Actuators

- 3.3.2.2 Shape Memory Alloy Actuators

- 3.3.2.3 Magnetic Linear Actuators

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Pricing analysis (Driven by Primary Research)

- 3.5.1 Historical price trend analysis

- 3.5.2 Pricing strategy by player type (Premium / Value / Cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 US - U.S. Environmental Protection Agency (EPA)

- 3.6.1.2 Canada - Transport Canada (TC)

- 3.6.2 Europe

- 3.6.2.1 EU - European Commission (EC)

- 3.6.2.2 Germany - German Federal Motor Transport Authority (KBA)

- 3.6.3 Asia Pacific

- 3.6.3.1 China - China National Standards (GB)

- 3.6.3.2 India - Automotive Research Association of India (ARAI)

- 3.6.4 Latin America

- 3.6.4.1 Brazil - INMETRO

- 3.6.4.2 Colombia - National Road Safety Agency (ANSV)

- 3.6.5 Middle East & Africa

- 3.6.5.1 UAE - Emirates Authority for Standardization and Metrology (ESMA)

- 3.6.5.2 South Africa - South African Bureau of Standards (SABS)

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent landscape (Driven by Primary Research)

- 3.10 Cost breakdown analysis

- 3.10.1 Raw material procurement costs

- 3.10.2 Manufacturing and assembly costs

- 3.10.3 Production equipment and tooling costs

- 3.10.4 Quality control and testing costs

- 3.11 Trade Data Analysis (Driven by Paid Database)

- 3.11.1 Import/Export Volume & Value Trends

- 3.11.2 Key Trade Corridors & Tariff Impact

- 3.12 Capacity & Production Landscape (Driven by Primary Research)

- 3.12.1 Installed Capacity by Region & Key Producer

- 3.12.2 Capacity Utilization Rates & Expansion Pipelines

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable Practices

- 3.13.2 Waste Reduction Strategies

- 3.13.3 Energy Efficiency in Production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon Footprint Considerations

- 3.14 Impact of AI & Generative AI on the Market

- 3.14.1 AI-driven disruption of existing business models

- 3.14.2 GenAI use cases & adoption roadmap by segment

- 3.14.3 Risks, limitations & regulatory considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Actuator, 2022 - 2035 ($ Mn, Units)

- 5.1 Key trends

- 5.2 Linear actuators

- 5.3 Rotary actuators

Chapter 6 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn, Units)

- 6.1 Key trends

- 6.2 Throttle Actuator

- 6.3 Turbo Actuator

- 6.4 Brake Actuator

- 6.5 HVAC Actuator

- 6.6 Power Window Actuator

- 6.7 Headlamp Actuator

- 6.8 EGR Actuator

- 6.9 Power Seat Actuator

- 6.10 Mirror Glass Actuators

- 6.11 Others

Chapter 7 Market Estimates and Forecast, By Motor Technology, 2022 - 2035 ($ Mn, Units)

- 7.1 Key trends

- 7.2 Brushed DC motors

- 7.3 Brushless DC (BLDC) motors

- 7.4 Stepper motors

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn, Units)

- 8.1 Key trends

- 8.2 Engine

- 8.3 Body & Exterior

- 8.4 Interior

Chapter 9 Market Estimates and Forecast, By Vehicle, 2022 - 2035 ($ Mn, Units)

- 9.1 Key trends

- 9.2 Passenger cars

- 9.2.1 Hatchback

- 9.2.2 Sedan

- 9.2.3 SUV

- 9.3 Commercial vehicles

- 9.3.1 LCV

- 9.3.2 MCV

- 9.3.3 HCV

Chapter 10 Market Estimates and Forecast, By Sales Channel, 2022 - 2035 ($ Mn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Netherlands

- 11.3.8 Norway

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 South Korea

- 11.4.4 India

- 11.4.5 Australia

- 11.4.6 Thailand

- 11.4.7 Indonesia

- 11.4.8 Singapore

- 11.4.9 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Chile

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global players

- 12.1.1 Robert Bosch

- 12.1.2 Denso

- 12.1.3 Continental

- 12.1.4 Valeo

- 12.1.5 ZF Friedrichshafen

- 12.1.6 Mitsubishi Electric

- 12.1.7 BorgWarner

- 12.1.8 Aisin

- 12.1.9 Mahle

- 12.1.10 Nidec

- 12.1.11 Johnson Electric

- 12.1.12 Magna

- 12.1.13 HELLA

- 12.2 Regional players

- 12.2.1 Hyundai Mobis

- 12.2.2 Vitesco Technologies

- 12.2.3 Marelli

- 12.2.4 NTN

- 12.2.5 Schaeffler

- 12.3 Emerging players

- 12.3.1 Thyssenkrupp

- 12.3.2 Minebea Mitsumi