PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038763

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038763

Cutting Tool Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

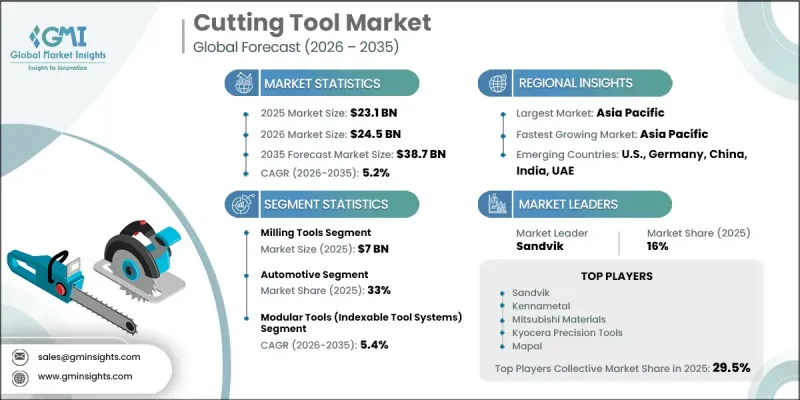

The Global Cutting Tool Market was valued at USD 23.1 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 38.7 billion by 2035.

This market is experiencing significant growth, driven largely by advancements in manufacturing methods. With the rise of automation and Industry 4.0 practices, there is an increasing demand for precision tools that produce defect-free parts. Industries like automotive, aerospace, and electronics particularly benefit from such accuracy. Additionally, the shift toward using lighter and stronger materials, including composites and high strength alloys, necessitates more advanced cutting tools that can handle these tough materials. Another key driver is the ongoing infrastructure boom, especially in rapidly developing economies, which raises the need for tools suitable for large machines and site equipment. Along with this, the focus on optimizing raw material use and minimizing waste continues to push manufacturers toward more durable, cost-effective cutting tools.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $23.1 Billion |

| Forecast Value | $38.7 Billion |

| CAGR | 5.2% |

Furthermore, the drive for greener production methods is accelerating within the cutting tools industry, as companies increasingly prioritize sustainability alongside performance. Manufacturers are adopting eco-friendly practices at every stage, from sourcing raw materials to improving energy efficiency during the manufacturing process. Advances in cutting tool coatings and materials are enabling longer tool lifespans and reduced waste, while also enhancing cutting efficiency. Additionally, there is a growing emphasis on recycling and reusing cutting tools, reducing the overall environmental footprint. Many companies are also focusing on reducing hazardous emissions and minimizing the use of harmful chemicals during the production process.

In 2025, the automotive segment held a 33% share and is projected to grow at a CAGR of 5.4% from 2026 to 2035. Strong growth in this segment is expected within the cutting tools market due to rising demand for fuel-efficient vehicles. The ongoing shift toward electric vehicle production is also increasing the requirement for advanced cutting tools to support more precise and efficient automotive manufacturing processes.

The milling tools segment accounted for USD 7 billion in 2025. The rapid expansion of this segment can be attributed to the wide range of tasks milling tools can handle in multiple industries. These tools are essential for producing complex profiles with high precision, and they are commonly used in automotive, aerospace, and electronics. As product designs demand lighter yet more durable parts, milling tools are gaining popularity due to their ability to cut through advanced materials. Innovations, such as multi-purpose designs and improved coatings, have also contributed to the segment's growth by extending tool life and reducing operational costs.

United States Cutting Tool Market was valued at USD 3.5 billion in 2025. The U.S. manufacturing sector, which spans a wide range of industries, is a key factor driving this dominance. The automotive and aerospace sectors fuel the demand for highly accurate tools that meet stringent quality standards. Additionally, the integration of robotics, sensors, and cloud analytics in manufacturing further boosts market growth by enhancing operational efficiency.

Key companies in the Global Cutting Tool Industry include Ceratizit S.A., Cougar Cutting Tools, Emuge Corporation, Greenleaf Corporation, Ingersoll Cutting Tools, Iscar Ltd., Kennametal Inc., Mapal Inc., Mitsubishi Materials Corporation, Mohawk Special Cutting Tools, OSG Corporation, Sandvik Coromant, Seco Tools AB, Tungaloy Corporation, and Walter Technologies. In response to the increasing demand for cutting-edge products, companies in the cutting tool market are focusing on technological advancements to enhance their market position. Leading players are investing heavily in research and development to improve the performance of their tools and increase their lifespan. They are also actively exploring sustainable manufacturing techniques to meet environmental regulations and consumer demands for greener products. Additionally, strategic partnerships, mergers, and acquisitions are being utilized to expand product offerings and strengthen supply chains. Companies are also incorporating digital tools, such as smart sensors and IoT-enabled devices, to enhance precision and operational efficiency in manufacturing.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Tool Type

- 2.2.3 Cutting Material

- 2.2.4 Tool Configuration

- 2.2.5 End Use Industry

- 2.2.6 Distribution Channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2025 (driven by primary research)

- 3.6.1 Historical price trend analysis

- 3.6.2 Pricing strategy by tool type (premium / value / cost-plus)

- 3.6.3 Price variation by product type & technology generation

- 3.6.4 Consumer price sensitivity analysis

- 3.7 Regulatory landscape

- 3.7.1 Environmental regulations: REACH (EU), conflict minerals compliance

- 3.7.2 Quality and safety standards: ISO 9001, ISO 16084 (cutting tool standards)

- 3.7.3 Trade policies and tariffs impacting tool exports

- 3.7.4 Regional regulatory frameworks

- 3.8 Impact of AI & generative AI on the market

- 3.8.1 AI-driven disruption of traditional business models

- 3.8.2 GenAI use cases & adoption roadmap by customer segment

- 3.8.3 Risks, limitations & regulatory considerations

- 3.8.4 AI-enabled smart home ecosystem integration

- 3.9 Trade data analysis (driven by paid database) (HS Code: 8207)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.10.1 Channel coverage by region & format (modern vs. traditional trade)

- 3.10.2 Last-mile infrastructure gaps & emerging channel shifts

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Tool Type, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Drilling tools

- 5.2.1 Twist drills

- 5.2.2 Gun drills

- 5.2.3 Indexable drills

- 5.2.4 Solid carbide drills

- 5.3 Milling tools

- 5.3.1 End mills

- 5.3.2 Face mills

- 5.3.3 Solid carbide mills

- 5.4 Turning tools

- 5.4.1 Indexable turning inserts

- 5.4.2 Boring bars

- 5.4.3 Grooving and parting tools

- 5.5 Threading tools

- 5.5.1 Thread mills

- 5.5.2 Taps

- 5.5.3 Thread forming tools

- 5.6 Reaming tools

- 5.6.1 Machine reamers

- 5.6.2 Hand reamers

- 5.6.3 Adjustable reamers

- 5.7 Countersinking and deburring tools

- 5.7.1 Countersinks

- 5.7.2 Deburring tools

- 5.7.3 Chamfer mills

- 5.8 Deep-hole drilling tools

Chapter 6 Market Estimates & Forecast, By Cutting Material, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Solid carbide tools

- 6.3 Polycrystalline diamond (PCD) tools

- 6.4 Polycrystalline cubic boron nitride (PCBN) tools

- 6.5 High-speed steel (HSS) tools

- 6.6 Cermet tools

- 6.7 Ceramic tools

Chapter 7 Market Estimates & Forecast, By Tool Configuration, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Modular tools (indexable tool systems)

- 7.3 Monolithic tools (solid/brazed tools)

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Aerospace & defense

- 8.4 Construction

- 8.5 Consumer electronics

- 8.6 Energy

- 8.7 Tool and mold making

- 8.8 Others (marine, agriculture etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Top Global Players

- 11.1.1 Iscar (IMC Group)

- 11.1.2 Kennametal

- 11.1.3 Kyocera Precision Tools

- 11.1.4 Mitsubishi Materials

- 11.1.5 Sandvik Coromant

- 11.1.6 Seco Tools

- 11.1.7 Sumitomo Electric Hardmetal

- 11.2 Regional Key Players

- 11.2.1 Ingersoll Cutting Tools

- 11.2.2 Korloy

- 11.2.3 Mapal

- 11.2.4 OSG Corporation

- 11.2.5 Walter

- 11.2.6 Widia

- 11.2.7 Zhuzhou Cemented Carbide

- 11.3 Emerging and Specialized Players

- 11.3.1 Allied Machine & Engineering

- 11.3.2 BIG Kaiser Precision

- 11.3.3 Carmex Precision Tools

- 11.3.4 Fullerton Tool

- 11.3.5 Greenleaf Corporation

- 11.3.6 Harvey Tool

- 11.3.7 Monster Tool Company