PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038776

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038776

Seed Coating Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

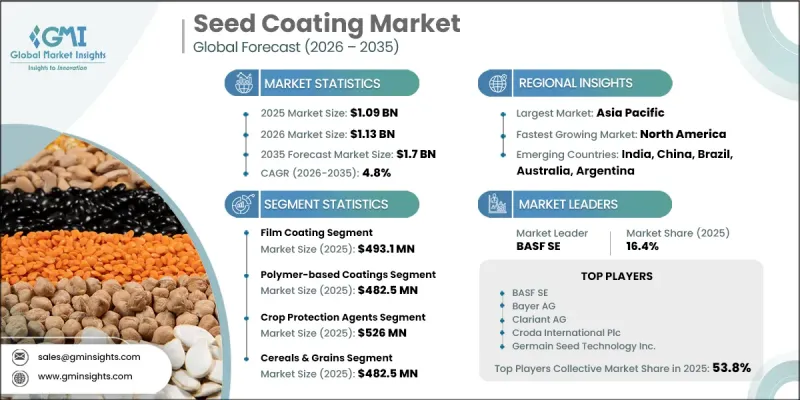

The Global Seed Coating Market was valued at USD 1.09 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 1.7 billion by 2035.

Seed coating refers to a set of agricultural processes that apply protective and functional layers to seeds using techniques such as film coating, pelleting, encrusting, and priming. These processes typically involve mixing, layering, drying, and quality assurance steps that improve seed durability, protect against pests and diseases, and ensure uniform planting performance. The result is improved germination, stronger crop establishment, and enhanced agronomic value compared to untreated seeds. Seed coating plays a crucial role in modern agricultural systems by converting raw seeds into higher-performing commercial products that support productivity and reduce crop losses. It is widely adopted in large-scale farming regions where consistent food production, efficient resource utilization, and pest management are essential. The industry combines advanced mechanical, chemical, and biological processing methods through both specialized facilities and large automated seed treatment systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.09 Billion |

| Forecast Value | $1.7 Billion |

| CAGR | 4.8% |

The seed coating market is also evolving through increased integration of precision agriculture practices and advanced seed enhancement technologies. Continuous improvements in formulation science are enabling better control over seed performance characteristics, including germination uniformity and environmental resistance. Rising demand for sustainable farming practices is encouraging the development of environmentally friendly coating materials that reduce chemical impact while maintaining effectiveness. Technological advancements in seed processing systems are further improving efficiency, scalability, and product consistency across large agricultural operations. Expanding global food demand is also driving greater adoption of treated seeds to improve yield reliability and reduce production risks.

The film coating segment accounted for USD 493.1 million in 2025. This method remains the most widely used due to its ability to deliver uniform seed coverage while preserving natural seed shape and ensuring precise delivery of active ingredients. It is highly compatible with modern sowing equipment and supports the application of multiple functional components in a single layer. Its efficiency and versatility make it a preferred choice among commercial seed producers and large-scale farming operations.

The polymer-based coatings segment reached USD 482.5 million in 2025. These coatings dominate the market due to their strong adhesion properties, controlled-release functionality, and compatibility with a wide range of active ingredients. They support improved seed protection and performance under varying environmental conditions. Other coating types, including biodegradable, mineral-based, and hybrid systems, are also used based on specific agricultural and environmental requirements. Growing emphasis on sustainability is further supporting the adoption of eco-friendly alternatives alongside advanced polymer formulations.

North America Seed Coating Market is projected to grow from USD 353.5 million in 2025 to USD 545.1 million by 2035. The region's growth is driven by rising demand for high-performance agricultural inputs that improve yield efficiency, pest resistance, and resource utilization. The adoption of advanced seed technologies is becoming standard practice in large-scale farming operations, particularly in row crop cultivation and specialty agriculture. Increasing use of precision farming systems and modern seed distribution networks is further strengthening market expansion. The integration of sustainable agricultural practices is also contributing to consistent adoption across the region.

Key companies operating in the Global Seed Coating Market include Bayer AG, BASF SE, Croda International Plc, Clariant AG, Sensient Technologies, Germain Seed Technology Inc., Brett Young Seeds Ltd, Michelman Inc, Precision Laboratories, and Smith Seed Service. Companies in the seed coating market are focusing on innovation, sustainability, and strategic expansion to strengthen their competitive position. They are investing in advanced formulation technologies to improve seed performance, durability, and environmental compatibility. Partnerships with seed producers and agricultural firms are helping expand product reach and improve application efficiency. Many players are prioritizing the development of bio-based and eco-friendly coating solutions to align with sustainability goals and regulatory requirements. Continuous research in polymer science and seed enhancement technologies is enabling better product differentiation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Coating technology

- 2.2.2 Coating material

- 2.2.3 Functional active ingredient

- 2.2.4 Crop type

- 2.2.5 End-user

- 2.2.6 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By coating material

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Coating Technology, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Film Coating

- 5.3 Encrusting

- 5.4 Pelleting

- 5.5 Priming & Enhancement Coatings

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Coating Material, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Polymer-Based Coatings

- 6.3 Natural/Biodegradable Materials

- 6.4 Mineral-Based Materials

- 6.5 Hybrid/Composite Materials

Chapter 7 Market Estimates and Forecast, By Functional Active Ingredient, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Crop Protection Agents

- 7.2.1 Insecticides

- 7.2.2 Fungicides

- 7.2.3 Nematicides

- 7.3 Nutritional Enhancements

- 7.4 Biological Agents

- 7.5 Seed Vigor & Germination Enhancers

- 7.6 Colorants & Markers

Chapter 8 Market Estimates and Forecast, By Crop Type, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Cereals & Grains

- 8.2.1 Corn/Maize

- 8.2.2 Wheat

- 8.2.3 Rice

- 8.2.4 Barley

- 8.2.5 Sorghum

- 8.2.6 Others

- 8.3 Oilseeds & Pulses

- 8.3.1 Soybean

- 8.3.2 Sunflower

- 8.3.3 Canola/Rapeseed

- 8.3.4 Peanuts

- 8.3.5 Lentils & Chickpeas

- 8.4 Vegetables

- 8.4.1 Tomato

- 8.4.2 Lettuce & Leafy Greens

- 8.4.3 Carrot & Root Vegetables

- 8.4.4 Onion & Alliums

- 8.4.5 Brassicas (Cabbage, Broccoli)

- 8.4.6 Others

- 8.5 Fruits

- 8.5.1 Berries

- 8.5.2 Melons

- 8.5.3 Others

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By End-user, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Commercial Seed Companies

- 9.3 Farmer/Grower Direct

- 9.4 Agricultural Cooperatives

- 9.5 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 BASF SE

- 11.2 Bayer AG

- 11.3 Brett Young Seeds Ltd

- 11.4 Clariant AG

- 11.5 Croda International Plc

- 11.6 Germain Seed Technology Inc.

- 11.7 Michelman, Inc

- 11.8 Precision Laboratories

- 11.9 Sensient Technologies

- 11.10 Smith Seed Service.