PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038791

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038791

Automotive Surround View System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

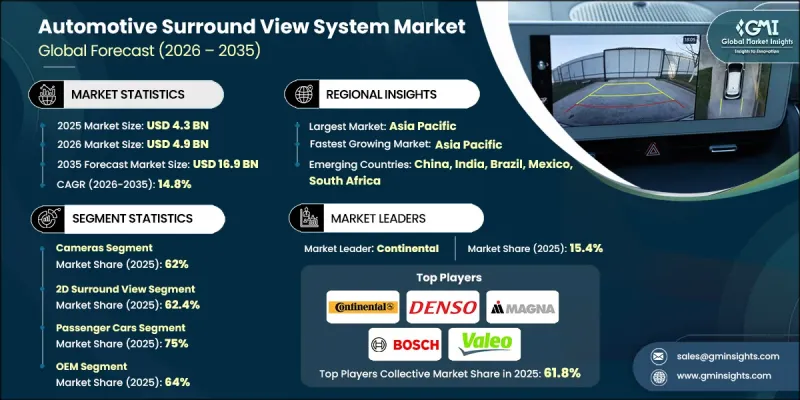

The Global Automotive Surround View System Market was valued at USD 4.3 billion in 2025 and is estimated to grow at a CAGR of 14.8% to reach USD 16.9 billion by 2035.

Increasing integration of advanced driver assistance systems is playing a central role in driving demand, as automakers aim to improve safety standards, enhance driving comfort, and meet evolving regulatory requirements. Rising concerns around road safety and traffic congestion are encouraging the adoption of technologies that improve visibility and minimize blind spots. Surround view systems are becoming essential in delivering a comprehensive view of the vehicle's surroundings, supporting safer maneuvering and parking. Growing consumer preference for larger vehicles and premium models is further accelerating adoption, as these vehicles require enhanced visibility solutions. In addition, regulatory bodies and safety organizations are promoting the use of advanced safety features, contributing to higher penetration across both mature and emerging automotive markets. Continuous technological advancements and increasing OEM participation are reinforcing the role of surround view systems as a critical component in modern vehicle design.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.3 Billion |

| Forecast Value | $16.9 Billion |

| CAGR | 14.8% |

The camera segment accounted for 62% share in 2025 and is expected to grow at a CAGR of 13.8% from 2026 to 2035. Ongoing improvements in sensor quality, image clarity, and performance in low-light conditions are enhancing system capabilities. Multi-camera configurations are becoming more widely adopted, supported by advancements that are making these solutions more cost-effective and accessible across a broader range of vehicle categories.

The 2D surround view segment held a 62.4% share in 2025 and is projected to grow at a CAGR of 14.3% through 2035. This segment is gaining traction due to its cost efficiency and simplified system architecture, enabling wider adoption across various vehicle segments. Integration with existing driver assistance functionalities enhances overall system value, allowing manufacturers to offer comprehensive safety solutions without significantly increasing costs.

United States Automotive Surround View System Market reached USD 1.05 billion in 2025. Market growth is supported by strong technological development and an increasing focus on vehicle safety standards. Manufacturers are advancing integrated systems that combine surround view capabilities with broader driver assistance features to meet regulatory expectations and improve overall performance. The expanding use of camera-based systems is also contributing to improved safety outcomes and greater adoption across a wider range of vehicles. Additionally, the integration of these systems into advanced vehicle platforms is supporting ongoing market expansion.

Key companies operating in the Global Automotive Surround View System Market include Continental, Denso, Robert Bosch, Magna International, Valeo, Aptiv, Hyundai Mobis, Panasonic, Mobileye (Intel), and Clarion/Faurecia. Companies in the Automotive Surround View System Market are strengthening their position through continuous innovation and strategic collaborations. They are investing in advanced imaging technologies, artificial intelligence, and sensor integration to enhance system accuracy and performance. Partnerships with automotive manufacturers are enabling deeper integration of surround view systems into next-generation vehicles. Many firms are focusing on cost optimization to expand adoption across mid-range vehicle segments. In addition, companies are expanding their global footprint by increasing production capabilities and entering emerging markets. Mergers and acquisitions are also being used to enhance technological expertise and diversify product offerings, while ongoing investment in research and development supports long-term growth.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Technology

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.2.6 Sales channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Component suppliers

- 3.1.2 System integrators

- 3.1.3 OEMs

- 3.1.4 Aftermarket distributors & installers

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of ADAS features

- 3.2.1.2 Rising demand for vehicle safety systems

- 3.2.1.3 Growth in premium and SUV vehicle sales

- 3.2.1.4 Stringent safety regulations and mandates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system cost in low-end vehicles

- 3.2.2.2 Integration complexity with vehicle electronics

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging automotive markets

- 3.2.3.2 Integration with autonomous driving systems

- 3.2.3.3 Advancements in AI-based image processing

- 3.2.3.4 Increasing EV adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Transport Canada Motor Vehicle Safety Standards (CMVSS)

- 3.4.2 Europe

- 3.4.2.1 European Whole Vehicle Type Approval (WVTA)

- 3.4.2.2 ECE Regulation 124 (R124)

- 3.4.3 Asia Pacific

- 3.4.3.1 Japan Automotive Standards Organization (JASO)

- 3.4.3.2 AIS (Automotive Industry Standards) - India

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Traffic Council (CONTRAN) - Resolution 242

- 3.4.4.2 Mexican NOM Standards (Normas Oficiales Mexicanas)

- 3.4.5 Middle East & Africa

- 3.4.5.1 Emirates Authority for Standardization and Metrology (ESMA)

- 3.4.5.2 South African Bureau of Standards (SABS)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing Analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by Primary Research)

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Trade data analysis (Driven by paid database)

- 3.12.1 Import/export volume & value trends

- 3.12.2 Key trade corridors & tariff impact

- 3.13 Impact of AI & Generative AI on the Market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Infrastructure & deployment landscape

- 3.14.1 Deployment penetration by region & buyer segment

- 3.14.2 Scalability constraints & infrastructure investment trends

- 3.15 Forecast assumptions & scenario analysis (driven by primary research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Cameras

- 5.3 Electronic control unit

- 5.4 Display unit

- 5.5 Software

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 2D surround view

- 6.3 3D surround view

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Parking assistance

- 8.3 Collision avoidance

- 8.4 Autonomous driving support

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Sales channel, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.4.8 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 Aptiv

- 11.1.2 Continental

- 11.1.3 Denso

- 11.1.4 Hyundai Mobis

- 11.1.5 Magna

- 11.1.6 Robert Bosch

- 11.1.7 Valeo

- 11.1.8 ZF Friedrichshafen

- 11.2 Regional players

- 11.2.1 Ficosa

- 11.2.2 Gentex

- 11.2.3 Kyung Chang Industrial

- 11.2.4 Marelli

- 11.2.5 Mitsubishi Electric

- 11.2.6 Panasonic Automotive Systems

- 11.2.7 Stoneridge

- 11.2.8 Tokai Rika

- 11.3 Emerging players

- 11.3.1 Clarion

- 11.3.2 STONKAM

- 11.3.3 Streamax Technology

- 11.3.4 Xiamen Xoceco Electronics